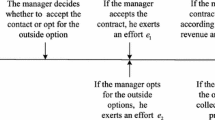

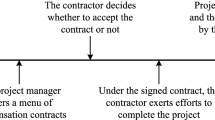

Abstract

The R&D project manager tends to misreport risk aversion magnitude and shirk under uncertain environment for acquiring information rent and risk premium, which brings a significant challenge for the firm when designing compensation contracts. We consider an agency problem where a firm employs a manager who has private information about his risk aversion magnitude and unobservable efforts to implement a R&D project through a menu of incentive contracts. Both the subjective assessments about the risk aversion degree and the project variability are characterized as uncertain variables. Within the framework of uncertainty theory and principal-agent theory, we investigate the impacts of information asymmetry on the optimal compensation contracts and the firm’s profits under four information structures. We demonstrate that, counterintuitive as it sounds, the manager’s optimal contract under full information is the same as that under pure adverse selection. Nevertheless, compared to the case under full information, the firm should distort the commission rate upwards under pure moral hazard and dual asymmetric information. We also show that when the manager’s efforts are observable, hidden information about the risk aversion magnitude has no effect on the firm’s profit. However, when unobservable, private risk aversion degree always brings about information rent and induces a loss for the firm’s profit. Finally, our study provides managerial recommendations on mitigating the adverse impacts caused by asymmetric information.

Similar content being viewed by others

References

Armstrong CS, Larcker DF, Su CL (2010) Endogenous selection and moral hazard in compensation contracts. Oper Res 58(4):1090–1106

Bergmann R, Friedl G (2008) Controlling innovative projects with moral hazard and asymmetric information. Res Policy 37(9):1504–1514

Bhattacharya S, Gaba V, Hasija S (2014) A comparison of milestone-based and buyout options contracts for coordinating R&D partnerships. Manag Sci 61(5):963–978

Brown DC, Davies SW (2017) Moral hazard in active asset management. J Financ Econ 125(2):311–325

Bubshait AA (2003) Incentive/disincentive contracts and its effects on industrial projects. Int J Proj Manag 21(1):63–70

Chao RO, Lichtendahl KC, Grushka-Cockayne Y (2014) Incentives in a stage-gate process. Prod Oper Manag 23(8):1286–1298

Chen YJ (2013) Risk-incentives trade-off and outside options. OR Spectrum 35(4):937–956

Chen Z, Lan Y, Zhao R (2016) Impacts of risk attitude and outside option on compensation contracts under different information structures. Fuzzy Optim Decis Mak. https://doi.org/10.1007/s10700-016-9263-7

Crama P, De Reyck B, Degraeve Z (2013) Step by step. The benefits of stage-based R&D licensing contracts. Eur J Oper Res 224(3):572–582

Crama P, De Reyck B, Taneri N (2016) Licensing contracts: control rights, options, and timing. Manag Sci 63(4):1131–1149

Dai Y, Chao X (2013) Salesforce contract design and inventory planning with asymmetric risk-averse sales agents. Oper Res Lett 41(1):86–91

Dutta S (2003) Capital budgeting and managerial compensation: incentive and retention effects. Account Rev 78(1):71–93

He Z, Li S, Wei B, Yu J (2013) Uncertainty, risk, and incentives: theory and evidence. Manag Sci 60(1):206–226

Holmstrom B (1979) Moral hazard and observability. ACA Trans 10(1):74–91

Holmstrom B (1982) Moral hazard in teams. ACA Trans 13(2):324–340

Huang H, Shen X, Xu H (2016) Procurement contracts in the presence of endogenous disruption risk. Decis Sci 47(3):437–472

Li X, Qin Z (2014) Interval portfolio selection models within the framework of uncertainty theory. Econ Model 41:338–344

Liu B (2007) Uncertainty theory. Springer, Berlin

Liu B (2013) Extreme value theorems of uncertain process with application to insurance risk model. Soft Comput 17(4):549–556

Liu Y, Chen X, Ralescu DA (2015) Uncertain currency model and currency option pricing. Int J Intell Syst 30(1):40–51

Manso G (2011) Motivating innovation. J Financ 66(5):1823–1860

Mihm J (2010) Incentives in new product development projects and the role of target costing. Manag Sci 56(8):1324–1344

Mu R, Lan Y, Tang W (2013) An uncertain contract model for rural migrant worker’s employment problems. Fuzzy Optim Decis Mak 12(1):29–39

Rahmani M, Roels G, Karmarkar US (2017) Collaborative work dynamics in projects with co-production. Prod Oper Manag 26(4):686–703

Taneri N, De Meyer A (2017) Contract theory: impact on biopharmaceutical alliance structure and performance. Manuf Serv Oper Manag 19(3):453–471

Wu X, Zhao R, Tang W (2014a) Uncertain agency models with multi-dimensional incomplete information based on confidence level. Fuzzy Optim Decis Mak 13(2):231–258

Wu Y, Ramachandran K, Krishnan V (2014b) Managing cost salience and procrastination in projects: compensation and team composition. Prod Oper Manag 23(8):1299–1311

Xiao W, Xu Y (2012) The impact of royalty contract revision in a multistage strategic R&D alliance. Manag Sci 58(12):2251–2271

Yang K, Zhao R, Lan Y (2014) The impact of risk attitude in new product development under dual information asymmetry. Comput Ind Eng 76(10):122–137

Yang K, Zhao R, Lan Y (2016) Impacts of uncertain project duration and asymmetric risk sensitivity information in project management. Int Trans Oper Res 23(4):749–774

Yang K, Lan Y, Zhao R (2017) Monitoring mechanisms in new product development with risk-averse project manager. J Intell Manuf 28(3):667–681

Yao K, Li X (2012) Uncertain alternating renewal process and its application. IEEE Trans Fuzzy Syst 20(6):1154–1160

Acknowledgements

This work was supported by the National Natural Science Foundation of China (Grant Nos. 71771166 and 71771165).

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Additional information

Communicated by X. Li.

Appendix

Appendix

Proof of Proposition 1

Noting that because the project manager’s expected profit is decreasing in the fixed payment, the individual rationality constraint for the manager must bind at optimality. Thus, we can substitute it into the objective function of Model (8) and obtain the firm’s expected profit:

which is decreasing in \(w_1\) and concave in \(e_{1}\) and \(e_{2}\). Thus, the firm would set both \(w_1\) to zero for getting a maximum profit. Besides, we can yield the manager’s optimal effort levels \(e_1=r_1v\) and \(e_2=r_2d_1\) by using the first-order condition. Following the determinate individual rationality constraint which is binding, the corresponding optimal fixed payment \(w_0\) can be derived immediately. The proof of the proposition is complete. \(\square \)

Proof of Proposition 2

Based on the incentive compatibility constraint for moral hazard, the manager will choose his optimal efforts in the research and development stages to maximize his own utility:

which is concave in \(e_1\) and \(e_2\). We can derive the optimal effort level \(e_{1}^*=r_1v w_1\) and \(e_{2}^*=r_2d_1 w_1\) by the first-order condition. Furthermore, as the individual rationality constraint should be binding at optimality, by substituting \(e_{1}^*\) and \(e_{2}^*\) into the individual rationality constraint and then substituting the fixed wage (\(w_0\)) and the effort levels (\(e_{1}^*\) and \(e_{2}^*\)) into the objective function, the firm’s expected profit can be rewritten as

By the first-order condition regarding to \(w_1\), we can obtain \(w_1(x)=\frac{(r_1v)^2+(r_2d_1)^2}{(r_1v)^2+(r_2d_1)^2+x\sigma ^2}\). Based on the binding individual rationality constraint, the optimal fixed payment \(w_0\) can be obtained immediately. The proof of the proposition is complete.\(\square \)

Proof of Lemma 1

The incentive compatibility constraint for adverse selection can be written as

which means that \(\mathrm{CE}(x,y)\) obtains its maximal value at \(\mathrm{CE}(x,x)\), i.e., the manager can obtain his maximal profit \(\mathrm{CE}(x,y)\) if and only if \(x=y\). Thus, \(\mathrm{CE}(x,y)\) satisfies the first-order condition (i.e., local incentive compatibility constraint) \(\frac{\partial \mathrm{CE}(x,y)}{\partial y}\bigm |_{y=x}=0\) and the second-order condition \(\frac{\partial ^{2} \mathrm{CE}(x,y)}{\partial y^{2}}\bigm |_{y=x}\leqslant 0\). It follows from the first-order condition that

Differentiating the first-order condition (11) with respect to x yields

It follows from the second-order condition that

On the basis of (12) and (13), we gain the monotonicity condition

Suppose, next, that both the local incentive compatibility and monotonicity conditions hold. Then it must be the case that all the manager’s incentive compatibility conditions hold. To see this result, without loss of generality, suppose that \(x>y\). By integrating the local incentive compatibility condition (11) and using the monotonicity condition (14), we can obtain

That is to say

On the other hand, if \(x<y\), we can also obtain

That is to say

This result establishes the equivalence between the monotonicity condition together with the local incentive compatibility condition and the full set of the manager’s incentive constraints.

Differentiating \(\mathrm{CE}(x,x)\) with respect to x yields

The individual rationality constraint is equivalent to

The constraint is binding under the optimal mechanism because the firm will reap the redundant profit, so that \(\mathrm{CE}(1,1)=0\).\(\square \)

Proof of Lemma 2

Because

we can derive

Combining the definition of CE(x, x) in equation (2) yields

By substituting the fixed wage into the objective function, we can derive the firm’s expected profit

\(\square \)

Proof of Proposition 3

We can use the first-order condition \(\frac{\partial E[Q-W]}{\partial e_{1}}=0\) and \(\frac{\partial E[Q-W]}{\partial e_{2}}=0\) to yield the first-best effort levels: \(e_{1}^{A}=r_1v\) and \(e_{2}^{A}=r_2d_1\). Substituting it into the objective function and ignore the monotonicity constraint in Lemma 1, the firm’s problem can be rewritten as unconstrained optimization problem:

which is decreasing in \(w_1(x)\). Consequently, the firm’s optimization problem can be obtained as \(w_1(x)=0\). The corresponding optimal fixed payment \(w_0(x)\) for the manager can be obtained immediately. The proof of the proposition is complete.\(\square \)

Proof of Lemma 3

By using the first-order condition \( \frac{\partial \mathrm{CE}(x,x)}{\partial e_{1}}=0\) and \(\frac{\partial \mathrm{CE}(x,x)}{\partial e_{2}}=0\), the manager selects his optimal effort levels: \(e_{1}=r_1vw_1(x)\) and \(e_{2}=r_2d_1w_1(x)\). When the manager selects the contract \((w_0(x), w_1(x))\), his expected utility

Similarly, if the manager selects the contract \((w_0(y),w_1(y))\), his expected utility

The rest of the proof is similar to the Proof of Lemma 1. Therefore, the proof of the lemma is complete.\(\square \)

Proof of Lemma 4

Similar to the Proof of Lemma 2.\(\square \)

Proof of Proposition 4

Through the similar method used in the Proof of Proposition 3, the firm’s problem can be rewritten as

The first-order variation and the second-order variation of the firm’s expected profit are derived as

and

Following the determinate optimal incentive commission rate \(w_1(x)\), the corresponding optimal fixed payment \(w_0(x)\), the optimal effort levels \(\mathrm{e}^{\mathrm{D}}_1\) and \(\mathrm{e}^{\mathrm{D}}_2\) can be obtained immediately. The proof of the proposition is complete.\(\square \)

Proof of Proposition 5

The result is derived directly by comparing the project manager’s profits which are shown in Propositions 1–4.\(\square \)

Proof of Proposition 6

The result is derived directly by comparing the project manager’s profits which are shown in Corollaries 1–4.\(\square \)

Proof of Proposition 7

Similar to the Proof of Proposition 6.\(\square \)

Proof of Proposition 8

Similar to the Proof of Proposition 6.\(\square \)

Rights and permissions

About this article

Cite this article

Fu, Y., Chen, Z. & Lan, Y. The impacts of private risk aversion magnitude and moral hazard in R&D project under uncertain environment. Soft Comput 22, 5231–5246 (2018). https://doi.org/10.1007/s00500-017-2960-5

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00500-017-2960-5