Abstract

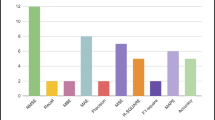

This paper provides evidence that forecasts based on global stock returns transmission yield better returns in day trading, for both developed and emerging stock markets. The study investigates the performance of global stock market price transmission information in forecasting stock prices using support vector regression for six global markets—USA (Dow Jones, S&P500), UK (FTSE-100), India (NSE), Singapore (SGX), Hong Kong (Hang Seng) and China (Shanghai Stock Exchange) over the period 1999–2011. The empirical analysis shows that models with other global market price information outperform forecast models based merely on auto-regressive past lags and technical indicators. Shanghai stock index movement was predicted best by Hang Seng Index opening price (57.69), Hang Seng Index by previous day’s S&P500 closing price (54.34), FTSE by previous day’s S&P500 closing price (57.94), Straits Times Index by previous day’s Dow Jones closing price (54.44), Nifty by HSI opening price (60), S&P500 by STI closing price (55.31) and DJIA by HSI opening price (55.22), and Nifty was found to be the most predictable stock index. Trading using global cues-based forecast model generates greater returns than other models in all the markets. The study provides evidence that stock markets across the globe are integrated and the information on price transmission across markets, including emerging markets, can induce better returns in day trading.

Similar content being viewed by others

References

Alberquerque R, Vega C (1997) Economic news and international stock market co-movement. Rev Finance 13(3):401–465

Anderson TG, Bollersev T, Diebold FX, Vega C (2007) Real-time price discovery in global stock, bond and foreign exchange markets. J Int Econ 73(2):251–277

Awokuse TO, Chopra A, Bessler DA (2009) Structural change and international stock market interdependence: evidence from Asian emerging markets. Econ Model 26:549–559

Balios D, Xanthakis M (2003) International interdependence and dynamic linkages between developed stock markets. South East Eur J Econ 1:105–130

Bekaert G, Harvey CR, Angela N (2005) Market integration and contagion. J Bus 78(1):39–70

Boser BE, Guyon IM and Vapnik VN (1992) A training algorithm for optimal margin classifiers. In: 5th annual ACM workshop on COLT, Pittsburgh, PA, pp 144–152

Brock W, Lakonishok J, Lebaron B (1992) Simple technical trading rules and the stochastic properties of stock returns. J Finance 47(5):1731–1764

Cao L (2003) Support vector machines experts for time series forecasting. Neurocomputing 51:321–339

Cao L, Francis EHT (2003) Support vector machine with adaptive parameters in financial time series forecasting. IEEE Trans Neural Netw 14(6):1506–1518

Chapelle O, Vapnik V, Bousquet O, Mukherjee S (2002) Choosing multiple parameters for support vector machines. Mach Learn 46:131–159

Cheng LH, Cheng YT (2009) A hybrid SOFM-SVR with a filter-based feature selection for stock market forecasting. Expert Syst Appl 36(2):1529–1539

Cheng W, Wanger L, Lin CH (1996) Forecasting the 30-year US treasury bond with a system of neural networks. J Comput Intell Finance 4:10–16

Chinag TC, Jeon BN, Li H (2007) Dynamic correlation analysis of financial contagion: evidence from Asia markets. J Int Money Finance 26(7):1206–1228

Chuang I, Lu JR, Tswei K (2007) Interdependence of international equity variances: evidence from East Asian markets. Emerg Mark Rev 8(4):311–327

Cortes C, Vapnik V (1995) Support-vector networks. Mach Learn 20:273–297

Cuadro-Saez L, Fratzscher M, Thimann C (2009) The transmission of emerging market shocks to global equity markets. J Empir Finance 16(1):2–17

De Santis G, Imrohoroglu S (1997) Stock returns and volatility in emerging financial markets. J Int Money Finance 16(4):561–579

Ehrmann M, Fratzcher M (2009) Global financial transmission of monetary policy shocks. Oxf Bull Econ Stat 71(6):739–759

Gerard B, Thanyalakpark K, Batten J (2003) Are the East Asian markets integrated? Evidence from the ICAPM. J Econ Bus 55(5):585–607

Hakin S (1999) Neural networks: a comprehensive foundation. Prentice Hall, Englewood Cliffs NJ. ISBN 0-13-273350-1

Hausman J, Wongswan J (2011) Global asset prices and FOMC announcements. J Int Money Finance 30(3):547–571

Iwatsubo K, Ingaki K (2007) Measuring financial market contagion using the dually traded stocks of Asian firms. J Asian Econ 18(1):217–236

Kim KJ (2003) Financial time series forecasting using support vector machines. Neurocomputing 55(1–2):307–319

Kim KJ (2006) Artificial neural networks with evolutionary instance selection for financial forecasting. Expert Syst Appl 30:519–526

Kim KJ, Han I (2000) Genetic algorithms approach to feature discretization in artificial neural networks for the prediction of stock price index. Expert Syst Appl 19(2):125–132

King MA, Wadhwani S (1990) Transmission of volatility between stock markets. Rev Financ Stud 3(1):5–33

Kodogiannis V, Lolis A (2002) Forecasting financial time series using neural network and fuzzy system-based techniques. Neural Comput Appl 11:90–102

Kumar M and Thenmozhi M (2005). Forecasting index future returns using neural network and ARIMA models. www.actapress.com—Paper No. 437-031, ISBN(CD) 0-88986-417-9

Kumar M and Thenmozhi M (2007) A comparison of different hybrid ARIMA—neural network models for stock index return forecasting and trading strategy. In: Proceedings of 20th Australasian banking and finance conference, Sydney, Australia

Kumar M, Thenmozhi M (2009) Forecasting stock index movement: a comparison of support vector machines and random forest. IIMB Manag Rev 21(1):41–55

Kumar M, Thenmozhi M (2012) Causal effect of volume on stock returns and conditional volatility in developed and emerging market. Am J Finance Account 2(4):346–362

Leung MT, Daouk H, Chen AS (2000) Forecasting stock indices: a comparison of classification and level estimation models. Int J Forecast 16:173–190

Li S, Chen S (2009) the transmission of pricing information of dually-listed between Hong Kong and New York stock exchange. J Serv Sci Manag 2:348–352

Lin WL, Engle RF, Ito T (1994) Do bulls and bears move across borders? International transmission of stock returns and volatility. Rev Financ Stud 7(3):507–538

Liu YA, Pan MS (1997) Mean and volatility spillover effects in the US and Pacific-Basin stock markets. Multinatl Finance J 1(1):47–62

Madaleno M, Pinho C (2012) International stock market indices co-movements: a new look. Int J Finance Econ 17(1):89–102

Masih R, Masih AMM (2001) Long and short term dynamic causal transmission amongst international stock markets. J Int Money Finance 20(4):563–587

Meric I, Kim JH, Linguo G, Meric G (2012) Co-movements of and linkages between Asian stock markets. Bus Econ Res J 3(1):1–15

Meyer D, Leisch F, Hornik K (2003) The support vector machine under test. Neurocomputing 55(1–2):169–186

Moustafa AAE (2011) Modeling and forecasting time varying stock return volatility in the Egyptian stock market. Int Res J Finance Econ 78, Euro Journals Publishing, Inc., ISSN 1450-2887. http://www.internationalresearchjournaloffinanceandeconomics.com

Neely CJ, Paul WA (2001) Technical analysis and central bank intervention. J Int Money Finance 20(7):949–970

Osler K (2000) Support for resistance: technical analysis and intraday exchange rates. FRBNY Econ Policy Rev 6(2):53–68

Ou P, Wang H (2009) Prediction of stock market index movement by ten data mining techniques. Mod Appl Sci 3(12):1852–1913

Pai PF, Lin CS (2005) A hybrid ARIMA and support vector machines model in stock price forecasting. Omega 33(6):497–505

Phylaktis K, Ravazzolo F (2004) Currency risk in emerging equity markets. Emerg Mark Rev 5:317–339

Schulmeister S (2009) Profitability of technical stock trading: has it moved from daily to intraday data? Rev Financ Econ 18(4):190–201

Sharda R, Patil RB (1994) A connectionist approach to time series prediction: an empirical test. In: Trippi RR, Turban E (eds) Neural networks in finance and investing. Probus Publishing Co, Chicago, pp 451–464

Sharkasi A, Ruskin HJ, Crane M (2005) Interrelationship among interrelationships among international stock market indices: Europe, Asia and the Americas. Int J Theor Appl Finance 8(05):603–622

Shin KS, Lee TS, Kim HJ (2005) An application of support vector machines in bankruptcy prediction model. Expert Syst Appl 28(1):127–135

Singh P, Kumar B and Pandey A (2010) Price and volatility spillovers across North American, European and Asian stock markets. Int Rev Financ Anal 19(1):55–64 Elsevier, ISSN 1057-5219, ZDB-ID 11336225

Soydemir G (2000) International transmission of stock market movements: evidence from emerging equity markets. J Forecast 19(3):149–176

Steven W, Narciso C (1999) Heuristic principles for the design of artificial neural networks. Inf Softw Technol 41(2):109–1197

Tay FEH, Cao LJ (2001) Application of support vector machines in financial time series forecasting. Omega 9(4):309–317

Taylor MP, Allen H (1992) The use of technical analysis in the foreign exchange market. J Int Money Finance 11(3):304–314

Vapnik VN (1999) An overview of statistical learning theory. IEEE Trans Neural Netw 10(5):988–999

Wongswan J (2006) Transmission of information across equity markets. Rev Financ Stud 19(4):1157–1189

Wongswan J (2009) The response of global equity indices to US monetary policy announcements. J Int Money Finance 28(2):344–365

Acknowledgments

We thank the anonymous referees and the discussant’s critical comments on an earlier version of this paper presented at the European Financial Management Association Annual Conference, Henley Business School, United Kingdom, June 26–29, 2013. We also acknowledge the suggestions given by the Conference participants, for improving the paper. We are also grateful to the referees of the journal for their valuable suggestions to improve this paper.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

The daily closing price plot and the corresponding daily closing return plots of SCI, Nifty, HSI, STI, FTSE, S&P500 and DJIA are shown below (Figs. 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15).

Plot of SCI closing prices

Plot of SCI closing returns

Plot of Nifty closing prices

Plot of Nifty closing returns

Plot of HSI closing prices

Plot of HSI closing returns

Plot of STI closing prices

Plot of STI closing returns

Plot of FTSE closing prices

Plot of FTSE closing returns

Plot of HSI closing prices

Plot of HSI closing returns

Plot of DJIA closing prices

Plot of DJIA closing returns

The closing price plots clearly reveal the impact of the global financial crisis during 2008–2009 in all the markets. Moreover, we also find a more cyclical trend in the index prices of the developed markets (UK, USA) compared to a linear increasing trend in the emerging markets (China, India). Thus, the data used covers periods of varying trends, and testing the models with rolling samples, prove that the forecast model developed is robust across different economic cycles.

Rights and permissions

About this article

Cite this article

Thenmozhi, M., Sarath Chand, G. Forecasting stock returns based on information transmission across global markets using support vector machines. Neural Comput & Applic 27, 805–824 (2016). https://doi.org/10.1007/s00521-015-1897-9

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00521-015-1897-9