Abstract

The paper examines the association between corporate leverage and their investment in R&D. Towards this end, it develops certain testable propositions. These propositions are tested using a dataset of manufacturing firms in India covering the period 1995–2010. Three main results are gleaned from the analysis. First, the optimal leverage ratio typically declines with R&D intensity. Second, the financial crisis has exerted a negative effect on leverage for firms. And finally, the dampening effect of R&D intensity on leverage is the highest for foreign private firms.

Similar content being viewed by others

Notes

The small- and medium-sized firms, as classified by the Indian Ministry of Micro, Small and Medium Enterprises, are those with investment in plant and machinery up to INR 100 million (approximately US $2.5 million).

The National Stock Exchange, the state-of-the-art exchange for listed companies, became operational from end 1994, which is why we focus on data from 1995 onwards.

R&D expenses often accounts for less than 1 % of turnover. Accordingly, companies often do not separately report such expenditures. This lack of a mandatory disclosure of R&D expenditures in accounts could be a source of bias because it is not evident whether the firm does not incur any expense on R&D or, alternately, whether it does but chooses not to report. Owing to this fact, even if a company reports zero R&D expenses, we retain it in the sample.

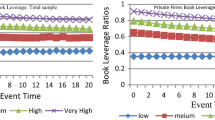

We also checked the impact of the financial crisis on leverage. The univariate tests indicate that the leverage, which was 0.340 in non-crisis years (SD = 0.191), declined to 0.327 (SD = 0.209) in the crisis years, and the differences were statistically significant.

The deep pocket policy suggests that the firm accumulates a significant quantum of funds in an earlier period to develop the project.

The rationale for using short-term leverage (in addition to leverage) rests on the fact that in a bank-dominated financial system as in India, it is typically big banks who lend debt and they may be concerned about recovery of their funds in the event of a bankruptcy of the firm. So while overall debt (comprising of bank plus non-bank debt) might be increasing owing to increasing recourse by corporates to non-bank debt (such as borrowings from development banks, debentures etc.), short-term debt (which is primarily bank debt) could be declining, since banks may discourage managers from investing in sunk costs. Therefore, a positive relationship between short-term leverage and R&D activity could signify risk aversion on the part of banks.

References

Acs ZJ (1988) Innovation in large and small firms: an empirical analysis. Am Econ Rev 78:678–690

Affleck-Graves J, Spiess D (1999) The long run performance of stock returns following debt offerings. Journal of Financial Economics 54:45–73

Aggarwal A (2000) Deregulation, technology imports and in-house R&D efforts: an analysis of the Indian experience. Res Policy 29:1081–1093

Aghion P, Klemm A, Bond S, Marinescu I (2004) Technology and financial structure: are innovative firms different? J Eur Econ Assoc 2:277–288

Audretsch DB, Acs ZJ (1991) Innovation and size at the firm level. South Econ J 57:739–744

Bah R, Dumontier P (2001) R&D intensity and corporate financial policy: some international evidence. Journal of Business Finance and Accounting 28:671–692

Bas M, Berthou A (2011) Financial reforms and foreign technology upgrading: evidence from India. Mimeo

Bitler MP, Moskowitz T, Jorgensen A (2004) Testing agency theory with entrepreneur effort and wealth. J Finance 60:539–576

Black B, Gilson RJ (1998) Venture capital and the structure of capital markets: banks versus capital markets. Journal of Financial Economics 47:243–277

Brown JR, Petersen BC (2009) Why has investment cash-flow sensitivity declined so sharply? Rising R&D and equity market developments. Journal of Banking and Finance 33:971–984

Brown JR, Fazzari SM, Petersen BC (2009) Financing innovation and growth: cash flow, external equity and the 1990s R&D boom. J Finance 64:151–185

Canepa A, Stoneman P (2008) Financial constraints to innovation in the UK: evidence from CIS2 and CIS3. Oxf Econ Pap 60:711–730

Chen H, Miao J, Wang N (2010) Entrepreneurial finance and non-diversifiable risk. Review of Financial Studies 23:4348–4388

Chibber PK, Majumdar SK (1999) Foreign ownership and profitability: property rights, control, and the performance of firms in Indian industry. J Law Econ 42:209–238

Cohen W (1995) Empirical studies of innovative activity. In: Stoneman P (ed) Handbook of economics and technological change. Blackwell, Oxford

Cohen W, Levin R (1989) Empirical studies of innovation and market structure. In: Schmalensee R, Willig R (eds) Handbook of industrial organization (vol. II), Ch. 18. Elsevier, Amsterdam

Cohen W, Klepper S (1994) Firm size and the nature of innovation within industries: the case of process and product R&D. Rev Econ Stat 78:232–243

Czarnitzki D, Kraft K (2009) Capital control, debt financing and innovative activity. Journal of Economic Behaviour and Organization 71:372–383

Dixon AJ, Seddighi HR (1996) An analysis of R&D activities in North East England manufacturing firms: the results of a sample survey. Reg Stud 30:287–294

Doukas J, Switzer L (1992) The stock market’s valuation of R&D spending and market concentration. Journal of Business Economics 44:95–114

Erikson R, Pakes A (1995) Markov-perfect industry dynamics: a framework for empirical work. Rev Econ Stud 62:53–82

Commission E (2011) Innovation Union competitiveness report 2011. European Commission, Brussels

Francis J, Smith A (1995) Agency costs and innovation: some empirical evidence. J Account Econ 19:383–409

Ghosh S (2006) Did financial liberalization ease financing constraints? Evidence from Indian firm-level data. Emerg Mark Rev 7:176–190

Ghosh S (2007) Bank monitoring, CEO ownership and firm valuation: empirical analysis for India. Manag Decis Econ 29:129–143

Goldar RN, Renganathan V (1988) Economic reforms and R&D expenditure in industrial firms in India. Indian Econ J 46:60–75

Goldberg P, Khandelwal A, Pavcnik N, Topalova P (2010a) Imported intermediate inputs and domestic product growth: evidence from India. Q J Econ 125:1727–1767

Goldberg P, Khandelwal A, Pavcnik N, Topalova P (2010b) Trade liberalization and new imported inputs. American Economic Review (Papers and Proceedings) 99:494–500

Government of India (2003) Research and development statistics. Department of Science and Technology, New Delhi

Gupta N (2005) Partial privatization and firm performance. J Finance 60:987–1015

Hall BH (1990) The impact of corporate restructuring on industrial research and development. Brookings Pap Econ Act 3:85–136

Hall B (2002) The financing of research and development. Oxford Rev Econ Policy 18:35–51

Hall BH (2010) The financing of innovative firms. Review of Economics and Institutions 1:1–30

Harris M, Raviv A (1991) The theory of the capital structure. J Finance 46:297–355

Himmelberg CP, Petersen BC (1994) R&D and internal finance: a panel study of small firms in high-tech industries. Rev Econ Stat 76:38–51

Kalemli-Ozcan S, Sorensen B, Yesiltas S (2011) Leverage across banks, firms and countries. NBER working paper 17354, Cambridge, MA

Kartak H (1985) Imported technology, enterprise size and R&D in a newly industrialising economy: the Indian experience. Oxf Bull Econ Stat 47:213–230

Kartak H (1989) Imported technology and R&D in a newly industrialising economy: the experience of Indian enterprises. J Dev Econ 31:123–139

Kartak H (1991) In house technological efforts, imports of technology and enterprise characteristics in a newly industrialising country: the Indian experience. J Int Dev 3:263–276

Kartak H (1997) Developing countries’ imports of technology, in house technological capabilities and efforts: an analysis of the Indian experience. J Dev Econ 53:67–83

Khandelwal A, Topalova P (2011) Trade liberalization and firm productivity: the case of India. Rev Econ Stat 93:995–1009

Khanna T, Palepu K (2000) Is group affiliation profitable in emerging markets: an analysis of diversified Indian business groups? J Finance 55:867–891

Klepper S (1996) Entry, exit, growth and innovation over the product life cycle. Am Econ Rev 86:562–583

Kumar N (1990) Multinational enterprises in India: industrial distribution, characteristics and performance. Routledge, London

Kumar N, Aggarwal A (2005) Liberalization, outward orientations and in-house R&D activity of multinational and local firms: a quantitative exploration for Indian manufacturing. Res Policy 34:441–449

Lall S (1987) Learning to industrialize: the acquisition of technological capability by India. McMillan, London

Love JH, Ashcroft B, Dunlop S (1996) Corporate structure, ownership and the likelihood of innovation. Appl Econ 28:737–746

Mani S (2008) Financing of industrial innovations in India: how effective are tax incentives for R&D? Centre for Development Studies working paper 405. CDS, Trivandrum

Myers SC, Majluf N (1984) Corporate financing and investment decisions when firms have information investors do not have. Journal of Financial Economics 13:187–221

Nelson R, Winter S (1982) The evolutionary theory of economic change. Harvard University Press, Cambridge

Patibandla M (2006) Equity pattern, corporate governance and performance: a study of India’s corporate sector. Journal of Economic behaviour and Organisation 59:29–44

Rajan RG, Zingales L (1998) Financial dependence and growth. Am Econ Rev 88:559–586

Zantout Z (1997) A test of the debt monitoring hypothesis: the case of corporate R&D expenditure. Financial Review 32:21–48

Acknowledgments

I would like to thank three anonymous referees and especially the Editor for their useful insights on an earlier draft which greatly improved the exposition and analysis. Needless to state, the views expressed and the approach pursued in the paper reflects the personal opinion of the author.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Ghosh, S. Does R&D intensity influence leverage? Evidence from Indian firm-level data. J Int Entrep 10, 158–175 (2012). https://doi.org/10.1007/s10843-012-0087-4

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10843-012-0087-4