Abstract

We empirically compare the contributions of venture capital (VC) and private equity backed firms, including those backed by government subsidized innovation investment funds (IIFs), in the Australian economy by analyzing employment, R&D, patents, time to IPO, and market capitalization from market inception to August 2012. Overall, the data highlight a central role for VC and IIF investment in facilitating R&D, innovation, and economic growth. Our IIF findings highlight the success of government sponsorship of VC under the Australian program design, which is sharply in contrast with the lack of success of government venture programs in other countries.

Similar content being viewed by others

Notes

The AVCAL sample comprises over 100 % more transactions recorded than that available in Thomson SDC’s database, and corrects for a large proportion of incorrect entries in SDC. AVCAL includes investments and failed firms, but of course they cannot be certain if they have captured 100 % of failures.

In 2002 Australia introduced legislation allowing venture capital limited partnerships to facilitate VC fundraising. Prior to that time funds were structured as trusts but essentially functionally equivalent to limited partnerships (Cumming and Johan 2013).

Source: http://www.nvca.org.

The word technology was included for the first two rounds of the IIF program (1997 and 2001) but removed for round 3 (2006)—see Section 1.2 in http://www.ausindustry.gov.au/programs/venture-capital/iif/Documents/IIF-GuideForApplicants2012.pdf.

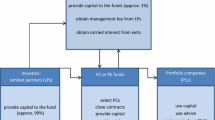

The government allocates capital to the IIF program. The government identifies appropriate fund managers through a competitive process and licenses them on the proviso that they can raise matching capital from private investors—it is then their job to go out and raise that capital.

AVCAL acknowledges that they may not have captured 100 % of failures, but have captured all known ones by the funds in the industry.

With 40 % of the population randomly selected in our data sample, our sampling error for non-VC/PE/IIF-backed firms is less than 0.5 %; see, e.g., Gravetter and Wallnau (2011).

We noted discrepancies in over 50 % of cases in the Thomson SDC sample relative to the AVCAL sample. Inferences from the data herein are significantly different with the AVCAL sample. The AVCAL sample is much larger (about twice as many transactions than that which is available from Thompson SDC) and a complete representation of all VC, PE and IIF transactions in Australia.

Source: http://www.nvca.org.

As indicated in Table 2, for these non-VC/PE/IIF figures we winsorized at the 99 % level, effectively not biasing results from Australian subsidiaries of large multinationals with very large numbers of patents.

For these figures we winsorized at the 99 % level, effectively not biasing results from Australian subsidiaries of large multinationals with very large numbers of patents. The numbers are calculated from Table 2 based on having sampled 40 % of comparable firms; see supra, footnote 13 and accompanying text.

References

Alperovych, Y., Hubner G., & Lobet, F. (2013). Venture capital-backing and public investor: Belgian evidence, Working Paper, EMLyon.

Amit, R., Brander, J., & Zott, C. (1998). Why do venture capital firms exist? Theory and Canadian evidence. Journal of Business Venturing, 13, 441–466.

Audretsch, D. B. (2003). Standing on the shoulders of midgets: The U.S. small business innovation research program (SBIR). Small Business Economics, 20, 129–135.

Audretsch, D. (2007). The entrepreneurial society. Oxford: Oxford University Press.

Audretsch, D. B., & Link, A. N. (2012). Entrepreneurship and innovation: Public policy frameworks. Journal of Technology Transfer, 37, 1–17.

Audretsch, D. B., Link, A. N., & Scott, J. T. (2002). Public/private technology partnerships: Evaluating SBIR supported research. Research Policy, 31, 145–158.

Bertoni, F., Ferrer, M. A. & Martí, J. (2012). The different role played by venture capital and private equity investors on the investment activity of their portfolio firms, Small Business Economics (forthcoming).

Bertoni, F., Meoli, M. & Vismara, S. (2013). Board independence, ownership structure, and the valuation of IPOs in continental Europe, Working Paper, University of Bergamo.

Bonardo, D., Paleari, S., & Vismara, S. (2011). Valuing university-based firms: The effects of academic affiliation on IPO performance. Entrepreneurship Theory and Practice, 35, 755–776.

Bonini, S., Alkan, S., & Salvi, A. (2012). The effects of venture capitalists on the governance of firms. Corporate Governance: An International Review, 20, 21–45.

Caselli, S., Gatti, S., & Perrini, F. (2009). Are venture capitalists a catalyst for innovation or do they simply exploit it? European Financial Management, 15, 92–101.

Cressy, R., Munari, F., & Malipiero, A. (2007). Playing to their strengths? Evidence that specialization in the private equity industry confers competitive advantage. Journal of Corporate Finance, 13, 647–669.

Croce, A., Grilli, L. & Murtinu, S. (2014). Venture capital enters academia: An analysis of university-managed funds, Journal of Technology Transfer, 39, 688–715.

Cumming, D. J. (2007). Government policy towards entrepreneurial finance: Innovation investment funds. Journal of Business Venturing, 22, 193–235.

Cumming, D. J. (2014). Public economics gone wild: Lessons from venture capital, International Review of Financial Analysis, 36, 251–260.

Cumming, D. J., & Johan, S. A. (2013). Venture capital and private equity contracting (2nd ed.). Amsterdam: Elsevier Science Academic Press.

Cumming, D. J., & Li, D. (2013). Public policy, entrepreneurship, and venture capital in the United States, Journal of Corporate Finance, 23, 345–367.

Cumming, D. J., & MacIntosh, J. G. (2006). Crowding out private equity: Canadian evidence. Journal of Business Venturing, 21, 569–609.

De Bettignies, J. (2008). Financing the entrepreneurial venture. Management Science, 54, 151–166.

Engel, D., & Keilbach, M. (2007). Firm-level implications of early stage venture capital investment—An empirical investigation. Journal of Empirical Finance, 14, 150–167.

Gans, J., Hayes, R., 2010. Assessing Australia’s Innovative Capacity: 2009 Update. IPRIA.

Gilson, R. J. (2003). Engineering a venture capital market: Lessons from the American experience. Stanford Law Review, 55, 1067–1103.

Giot, P., & Schwienbacher, A. (2007). IPOs, trade sales and liquidations: Modelling venture capital exits using survival analysis. Journal of Banking & Finance, 31, 679–702.

Gompers, P. A., & Lerner, J. (2004). The venture capital cycle (2nd ed.). Cambridge: MIT Press.

Gravetter, F. J., & Wallnau, L. B. (2011). Essentials of statistics for the behavioral sciences (7th ed.). Belmont, CA: Wadsworth.

Groh, A. P., & Andrieu, G. (2012). Entrepreneurs’ financing choice between independent and bank-affiliated venture capital firms. Journal of Corporate Finance, 18, 1143–1167.

Groh, A. P., & von Liechtenstein, H. (2011). The first step of the capital flow from institutions to entrepreneurs: The criteria for sorting venture capital funds. European Financial Management, 17(3), 532–559.

Groh, A. P., von Liechtenstein, H., & Lieser, K. (2010). The European venture capital and private equity country attractiveness indices. Journal of Corporate Finance, 16, 205–224.

Hirukawa, M., & Ueda, M. (2008). Venture capital and industrial ‘Innovation’, CEPR Discussion Paper No. DP7089.

Hirukawa, M., & Ueda, M. (2011). Venture capital and innovation: Which is First? Pacific Economic Review, 16(4), 421–465.

Kanniainen, V., & Keuschnigg, C. (2003). The optimal portfolio of start-up firms in venture capital finance. Journal of Corporate Finance, 9, 521–534.

Kanniainen, V., & Keuschnigg, C. (2004). Start-up investment with scarce venture capital support. Journal of Banking & Finance, 28, 1935–1959.

Keuschnigg, C., & Nielsen, S. B. (2001). Public policy for venture capital. International Tax and Public Finance, 8, 557–572.

Keuschnigg, C., & Nielsen, S. B. (2003a). Tax policy, venture capital and entrepreneurship. Journal of Public Economics, 87, 175–203.

Keuschnigg, C., & Nielsen, S. B. (2003b). Taxes and venture capital support. Review of Finance, 7, 515–539.

Keuschnigg, C., & Nielsen, S. B. (2004a). Progressive taxation, moral hazard, and entrepreneurship. Journal of Public Economic Theory, 6, 471–490.

Keuschnigg, C., & Nielsen, S. B. (2004b). Start-ups, venture capitalists and the capital gains tax. Journal of Public Economics, 88, 1011–1042.

Leleux, B., & Surlemont, B. (2003). Public versus private venture capital: Seeding or crowding out? A pan-European analysis. Journal of Business Venturing, 18, 81–104.

Lerner, J. (2009). Boulevard of broken dreams: Why public efforts to boost entrepreneurship and venture capital have failed—and what to do about it. Princeton: Princeton University Press.

Nahata, R. (2008). Venture capital reputation and investment performance. Journal of Financial Economics, 90, 127–151.

Nahata, R., Hazaruka, S. & Tandon, K. (2009). Success in global venture capital investing: Do institutional and cultural differences matter? Journal of Financial and Quantitative Analysis (forthcoming).

Schwienbacher, A. (2008). Innovation and venture capital exits. Economic Journal, 118, 1888–1916.

Toole, A. A., & Turvey, C. (2009). How does initial public financing influence private incentives for follow-on investment in early-stage technologies? Journal of Technology Transfer, 34, 43–58.

Vismara, S., Paleari, S., & Ritter, J. R. (2012). Europe’s second markets for small companies. European Financial Management, 18, 352–388.

Wang, S., & Wang, S. (2010). Cross-border venture capital performance: Evidence from China. Pacific-Basin Finance Journal, 19, 71–97.

Wang, L., & Wang, S. (2012a). Endogenous networks in investment syndication. Journal of Corporate Finance, 18, 640–663.

Wang, L., & Wang, S. (2012b). Economic freedom and cross-border venture capital performance, Journal of Empirical Finance, 19, 26–50.

Wang, S., & Zhou, H. (2004). Staged financing in venture capital: Moral hazard and risks. Journal of Corporate Finance, 10, 131–155.

Wonglimpiyarat, J. (2010). Commercialization strategies of technology: Lessons from Silicon Valley. Journal of Technology Transfer, 35, 225–236.

Wright, M., Vohora, A., & Lockett, A. (2004). The formation of high-technology university spinouts: The role of joint ventures and venture capital investors. Journal of Technology Transfer, 29, 287–310.

Yung, C. (2009). Entrepreneurial financing and costly due diligence. The Financial Review, 44, 137–149.

Zhang, J. (2009). The performance of university spin-offs: An exploratory analysis using venture capital data. Journal of Technology Transfer, 34, 255–285.

Acknowledgment

We are indebted to the Social Sciences and Humanities Research Council of Canada, the Australian Private Equity and Venture Capital Association (AVCAL), and the Department of Industry, Innovation, Science, Research and Tertiary Education (DIISRTE) for financial support. We owe thanks to Asish Naik, Vikrum Vijayarajan, and Warner Wu for research assistance. Also, we owe thanks to the seminar participants at the AVCAL Workshops in Sydney and Melbourne in September 2012, the French Finance Association Conference Participants in May 2013, the Financial Management Association Conference Participants in October 2013, the Technology Transfer Society Conference Participants in November 2013, as well as Tricia Berman, David Brown, Jeremy Chrisp, Joshua Funder, Shanon Glenn, Tom Honeyman, Derek Kerr, Kathy Nielsen, Roger Price, Kar Mei Tang, Brigitte Smith, Stephen Thompson, Malcolm Thornton, Silvio Vismara, Sam Waring, and Katherine Woodthorpe for helpful comments and suggestions. This paper was awarded the best paper prize by AVCAL in 2013.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Cumming, D., Johan, S. Venture’s economic impact in Australia. J Technol Transf 41, 25–59 (2016). https://doi.org/10.1007/s10961-014-9378-3

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10961-014-9378-3