Abstract

This paper compares alternative methods of controlling for the spatial dependence of house prices in a mass appraisal context. Explicit modeling of the error structure is characterized as a relatively fluid approach to defining housing submarkets. This approach allows the relevant submarket to vary from house to house and for transactions involving other dwellings in each submarket to have varying impacts depending on distance. We conclude that—for our Auckland, New Zealand, data—the gains in accuracy from including submarket variables in an ordinary least squares specification are greater than any benefits from using geostatistical or lattice methods. This conclusion is of practical importance, as a hedonic model with submarket dummy variables is substantially easier to implement than spatial statistical methods.

Similar content being viewed by others

Notes

An alternative approach would be to incorporate variables measuring neighborhood characteristics (as in Dubin 1988, for example). Such data would typically be available for small areas defined for census purposes. However, census areas are less likely to correspond to housing submarkets than are the valuer-defined areas used here.

Bourassa et al. (2003) show that the latter method, although quite simple, results in significant improvements in the accuracy of predictions based on a market-wide hedonic equation; thus we test for its impact here.

This code is available at http://www.spatial-statistics.com. Other general results on sparse matrices exist; see, for example, Bai and Golub (1997) and Reusken (2002).

A sale was removed from the sample if it fell into one of the following categories: (a) the property had a land area larger than 0.25 ha (this excluded properties that may have been sold primarily for redevelopment purposes); (b) the property had a floor area either less than 30 square meters (probably due to an error in data entry); (c) the transaction was flagged as not being “arm’s length”; or (d) the property was located on an island.

The OLS predictions are calculated as \(\exp {\left( {\widehat{{{\text{In}}Y}}} \right)}\), although the correct transformation would be \(\exp {\left( {\widehat{{{\text{In}}Y}} + 0.5\widehat{\sigma }^{2} } \right)}\). Because we are unable to implement equivalent transformations for predictions based on the other methods, we do not add \( 0.5\widehat{\sigma }^{2} \) before taking the antilogs of the OLS predictions. Given the large sample size, this has only a trivial impact on the results.

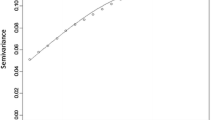

The body of each boxplot is constructed from the first to the third quartiles, while the whiskers are set at ±1.5 times the inter-quartile range from the median. However, if no observation exists at that distance, the whisker is set at the closest observation towards the body of the boxplot. If there are observations outside of the whiskers, each of these is depicted by a line. Within the body of each boxplot, the median over the 100 splits appears as a bar, while the 95% confidence interval is depicted by the indented and unshaded area in the center of the plot.

For comparison purposes, Fik et al. (2003) note that Freddie Mac prefers to have at least 50% of predictions within 10% of the actual values.

The adjustment using average residuals in submarkets is ineffective when submarket dummy variables are included in the model because the average of residuals for each submarket equals zero.

In the list of variables in Table 2, we deleted variables from “Walls in good condition” to “Average quality of the principal structure” and from “Water view” to “Very good neighborhood.”

References

Bai, Z., & Golub, G. H. (1997). Bounds for the trace of the inverse and the determinant of symmetric positive definite matrices. Annals of Numerical Mathematics, 4, 29–38.

Basu, A., & Thibodeau, T. G. (1998). Analysis of spatial autocorrelation in house prices. Journal of Real Estate Finance and Economics, 17(1), 61–85.

Bourassa, S. C., Hamelink, F., Hoesli, M., & MacGregor, B. D. (1999). Defining housing submarkets. Journal of Housing Economics, 8(2), 160–183.

Bourassa, S. C., Hoesli, M., & Peng, V. C. (2003). Do housing submarkets really matter? Journal of Housing Economics, 12(1), 12–28.

Can, A. (1992). Specification and estimation of hedonic housing price models. Regional Science and Urban Economics, 22(3), 453–474.

Can, A., & Megbolugbe, I. (1997). Spatial dependence and house price index construction. Journal of Real Estate Finance and Economics, 14(1/2), 203–222.

Case, B., Clapp, J., Dubin, R., & Rodriguez, M. (2004). Modeling spatial and temporal house price patterns: A comparison of four models. Journal of Real Estate Finance and Economics, 29(2), 167–191.

Clapp, J. M. (2003). A semiparametric method for valuing residential locations: Application to automated valuation. Journal of Real Estate Finance and Economics, 27(3), 303–320.

Colwell, P. F. (1998). A primer on piecewise parabolic multiple regression analysis via estimations of Chicago CBD land prices. Journal of Real Estate Finance and Economics, 17(1), 87–97.

Cressie, N. (1993). Statistics for spatial data. Wiley: New York.

Cressie, N., & Hawkins, D. M. (1980). Robust estimation of the variogram, I. Journal of the International Association for Mathematical Geology, 12(2), 115–125.

Dubin, R. A. (1988). Estimation of regression coefficients in the presence of spatially autocorrelated error terms. Review of Economics and Statistics, 70(3), 466–474.

Dubin, R. A. (1998). Predicting house prices using multiple listings data. Journal of Real Estate Finance and Economics, 17(1), 35–59.

Dubin, R., Pace, R. K., & Thibodeau, T. G. (1999). Spatial autoregression techniques for real estate data. Journal of Real Estate Literature, 7(1), 79–95.

Fik, T. J., Ling, D. C., & Mulligan, G. F. (2003). Modeling spatial variation in housing prices: A variable interaction approach. Real Estate Economics, 31(4), 623–646.

Getis, A., & Aldstadt, J. (2004). Constructing the spatial weights matrix using a local statistic. Geographical Analysis, 36(2), 90–104.

Haining, R. (1990). Spatial data analysis for the social and environmental sciences. Cambridge: Cambridge University Press.

LeSage, J. P., & Pace, R. K. (2004). Introduction. In J. P. LeSage & R. K. Pace (Eds.), Spatial and spatiotemporal econometrics. Advances in econometrics, Vol. 18 (pp. 1–32). Oxford: Elsevier.

Matheron, G. (1962). Traité de Géostatistique Appliquée, Tome I. Mémoires du Bureau de Recherches Géologiques et Minières, No. 14. Paris: Editions Technip.

Militino, A. F., Ugarte, M. D., & García-Reinaldos, L. (2004). Alternative models for describing spatial dependence among dwelling selling prices. Journal of Real Estate Finance and Economics, 29(2), 193–209.

Pace, R. K., & Barry, R. (1997a). Quick computation of regressions with a spatially autoregressive dependent variable. Geographical Analysis, 29(3), 232–247.

Pace, R. K., & Barry, R. (1997b). Sparse spatial autoregressions. Statistics and probability letters, 33(2), 291–297.

Pace, R. K., Barry, R., Clapp, J. M., & Rodriguez, M. (1998). Spatiotemporal autoregressive models of neighborhood effects. Journal of Real Estate Finance and Economics, 17(1), 15–33.

Pace, R. K., Barry, R., & Sirmans, C. F. (1998). Spatial statistics and real estate. Journal of Real Estate Finance and Economics, 17(1), 5–13.

Pace, R. K., & Gilley, O. W. (1997). Using the spatial configuration of the data to improve estimation. Journal of Real Estate Finance and Economics, 14(3), 333–340.

Pace, R. K., & Gilley, O. W. (1998). Generalizing the OLS and grid estimators. Real Estate Economics, 26(2), 331–347.

Palm, R. (1978). Spatial segmentation of the urban housing market. Economic Geography, 54(3), 210–221.

Reusken, A. (2002). Approximation of the determinant of large sparse symmetric positive definite matrices. SIAM Journal on Matrix Analysis and Applications, 23(3), 799–812.

Ripley, B. (1981). Spatial statistics. New York: Wiley.

Ugarte, M. D., Goicoa, T., & Militino, A. F. (2004). “Searching for housing submarkets using mixtures of linear models”. In J. P. LeSage, & R. K. Pace (Eds.), Spatial and spatiotemporal econometrics. Advances in econometrics, Vol. 18 (pp. 259–276). Oxford: Elsevier.

Acknowledgments

We thank John Clapp, Xavier de Luna, and two anonymous referees for useful comments.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Bourassa, S.C., Cantoni, E. & Hoesli, M. Spatial Dependence, Housing Submarkets, and House Price Prediction. J Real Estate Finan Econ 35, 143–160 (2007). https://doi.org/10.1007/s11146-007-9036-8

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-007-9036-8