Abstract

The aim of the paper is to assess the informational content of a survey-based measure of the Brazilian manufacturing capacity utilization rate produced by the Brazilian Institute of Economics from Getulio Vargas Foundation. From a theoretical point of view, the survey-based capacity measure should provide meaningful information with respect to the Brazilian business cycle. In this work, we choose to use the output gap as the most comprehensive and convincing proxy of the cyclical situation (Graff and Sturm in CESifo Econ Stud 58(1):220–251, 2012). More specifically, we will refer to a real-time version of the output gap, using an existing real-time GDP data set produced by the Central Bank of Brazil (Cusinato et al. in Empir Econ, 2012). The information efficiency of the real-time output gap estimates is tested checking whether survey data can help producing real-time estimates that are significantly closer to the latest releases. In this sense, the paper provides a significant contribution to the existing literature, extending analysis already available for OECD countries to the Brazilian economy. Our main result is that survey data can indeed help to produce more efficient estimates of the output gap in real time.

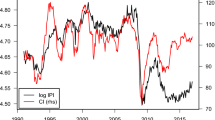

Source: FGV/IBRE and IBGE

Similar content being viewed by others

Notes

According to Stark (2002), real-time data consists in data as they existed prior to subsequent revisions. In this context, the term “vintage” is used to designate the last available information set for a variable on a specific date, i.e., the most recent revision up to that corresponding moment [see Croushore and Stark (2000, 2001)]; the collection of these vintages is generally referred to as a “real-time data set”.

The database has been updated using the publications of the Brazilian Institute of Geography and Statistics (IBGE) as the source.

Considering that we are working with quarterly data, the specifications adopted for the various filters are the following: for the HP filter, we used a value of the smoothing parameter λ equal to 1600; the Christiano–Fitzgerald filter filters out stochastic cycles for periods smaller than 1.5 years (six quarters) and larger than 8 years (32 quarters); the Butterworth filter filters out stochastic cycles at periods larger than 32 (8 years), the chosen order of this filter is 2; finally, the trend specified for the unobserved components model is a random walk with drift.

Economic Cycle Dating Committee (Comitê de Datação de Ciclos Econômicos, CODACE, in Portuguese). The CODACE chronology is the result of a consensus opinion among a panel of seven renowned economic experts. It was created in 2008 by FGV/IBRE with the task of maintaining a reference chronology of economic cycles in Brazil following the tradition established by the NBER in the USA and the CEPR in Europe.

These factors are determined by the relative weight of the branch in relation to the total manufacturing industry, according to IBGE.

More information about the FGV seasonal adjustment methodology can be found at http://portalibre.fgv.br.

Alternatively, revisions might happen because the underlying true value was initially measured with noise—which means the revision would be uncorrelated to the true value.

$$ g_{{R1_{t} }} - g_{{RN_{t} }} = \mu_{t}, \quad \hbox{where}\, cov (g_{{RN_{t} }} ,\mu_{t} ) = 0.$$Alternatively, we have also estimated Eq. (5) using LCU (−1) and both LCU and LCU (−1); the results were similar to those presented in Table 3. All the exercises were performed using both raw data and the real-time version of the seasonally adjusted LCU. The results are available with the authors upon request.

The equation above was estimated using Newey–West standard errors correcting for autocorrelation up to lag (N − 2).

Complete results for all revision horizons up to the twelfth revision are available with the authors upon request.

Knowing that, in the real world, by the end of a given quarter we only have the information for the previous quarter GDP, while survey data on capacity utilization are available by the end of the reference quarter.

The procedure we have used can be divided in three steps: first, we choose the ARMA model that best fits the first difference of each one of the 76 vintages of (seasonally adjusted) GDP; the resulting models were chosen on the basis of the Bayesian information criteria. The selected ARMA model for each vintage can be obtained under request. Secondly, we produce one-step ahead forecasts for each of the 76 GDP seasonally adjusted vintages. Finally, we calculate the output gap for each vintage including the additional forecasted data point calculated before. Results of the exercise are available with the authors upon request.

In most cases, we pick the contemporary LCU as a regressor. The only exception is when we use the UC method to estimate the gap: in this case, on the basis of preliminary testing, the lagged LCU is to be preferred.

The α 1, β 1 and β 2 values for each ECM estimate are available upon request.

References

Baxter, M., & King, R. G. (1999). Measuring business cycles: Approximate band-pass filters for economic time series. The Review of Economics and Statistics, 81(4), 575–593.

Bry, G., & Boschan, C. (1971). Cyclical analysis of economic time series: Selected procedures and computer programs. National Bureau of Economic Research, Inc., Technical Working Paper, No. 20.

Christiano, L. J., & Fitzgerald, T. J. (2003). The band pass filter. International Economic Review, 44(2), 435–465.

Clark, P. K. (1987). The cyclical component of U.S. economic activity. The Quartely Journal of Economics, 102(4), 797–814.

Cogley, T., & Nason, J. M. (1995). Effects of the Hodrick–Prescott filter on trend and difference stationary time series. Implications for business cycle research. Journal of Economic Dynamics and Control, 19, 253–278.

Croushore, D., & Stark, T. (2000). A real-time data set for macroeconomists: Does data vintage matter for forecasting? Working Papers 00-6, Federal Reserve Bank of Philadelphia.

Croushore, D., & Stark, T. (2001). Forecasting with a real-time data set for macroeconomists. Working Papers 01-10, Federal Reserve Bank of Philadelphia.

Cusinato, R. T., Minella, A., & Júnior, S. S. P. (2010). Output gap and GDP in Brazil: A real-time data analysis. Working Papers Series 203, Central Bank of Brazil, Research Department.

Cusinato, R. T., Minella, A., & Júnior, S. S. P. (2012). Output gap and GDP in Brazil: A real-time data analysis. Empirical Economics, 44(3), 1113–1127.

Graff, M., & Sturm, J.-E. (2012). The informational content of capacity utilization rates for output gap estimates. CESifo Economic Studies, 58(1), 220–251.

Harvey, A. C. (1985). Trends and cycles in macroeconomic time series. Journal of Business and Economic Statistics, 3, 216–227.

Harvey, A. C. (1989). Forecasting, structural time series models and the Kalman filter. Cambridge: Cambridge University Press.

Hodrick, R. J., & Prescott, E. C. (1981). Post-war business cycles: An empirical investigation. Center for Mathematical Studies in Economics and Management Science, Discussion Papers 451, Northwestern University.

Hodrick, R. J., & Prescott, E. C. (1997). Post-war business cycles: An empirical investigation. Journal of Money, Credit and Banking, 29, 1–16.

Malgarini, M., & Paradiso, A. (2012). Measuring capacity utilization in the Italian manufacturing sector: A comparison between time series and survey estimates. OECD Journal: Journal of Business Cycle Measurement and Analysis, 2012(2), 5–19.

Orphanides, A., & van Norden, S. (2002). The unreliability of output-gap estimates in real time. The Review of Economics and Statistics, 84(4), 569–583.

Orphanides, A., & van Norden, S. (2003). The reliability of inflation forecasts based on output gap estimates in real time. CIRANO Working Papers 2003s-01, CIRANO.

Palis, R. R., & Ramos, R. L. O., & Robitaille, P. (2004). News or noise? An analysis of Brazilian GDP announcements. International Finance Discussion Papers, No. 776, Federal Reserve Board.

Pollock, D. S. G. (2000). Trend estimation and de-trending via rational square-wave filters. Journal of Econometrics, 99, 317–334.

Stark, T. (2002). A summary of the conference on real-time data analysis. Federal Reserve Bank of Philadelphia Business Review, Q1, 5–11.

Author information

Authors and Affiliations

Corresponding author

Additional information

The opinions expressed in the paper are the sole responsibility of the author and do not involve ANVUR.

Rights and permissions

About this article

Cite this article

Lima, S., Malgarini, M. Does a Survey Based Capacity Utilization Measure Help Predicting Brazilian Output Gap in Real-Time?. J Bus Cycle Res 12, 119–139 (2016). https://doi.org/10.1007/s41549-016-0004-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41549-016-0004-3