Abstract

An exact dating of the onset of financial crises is important to learn which factors have caused or contributed to the financial turmoil. While most economists agree that the recent worldwide financial crises evolved as a consequence of a bursting bubble on the US housing market, the related literature yet failed to deliver a consensus on the question when exactly the bubble started developing. The estimates in the literature range in between 1997 and 2002, while applications of market-based procedures deliver even later dates. In this paper, we employ the methods of statistical process control to date the likely beginning of the bubble. The results support the view that the bubble on the US housing market already emerged as early as 1996/1997.

Similar content being viewed by others

Notes

The empirical analysis was conducted with R in combination with the mFilter package (Balcilar 2007).

In Zeileis et al. (2005) either all data or a moving window with fixed size are used. Note that the CUSUM process of the structural change literature differs from the one in statistical process control. Both designs are also known in the SPC literature (repeated significance tests and moving average charts, respectively). However, since the CUSUM test in the structural change literature is dominated by the described CUSUM chart and the EWMA chart, it is rarely used in the SPC literature.

The unit-root tests were conducted using the R package “fUnitRoots” (Wuertz et al. 2017).

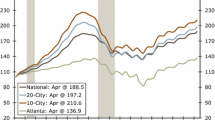

For the corresponding EWMA series with \(\lambda =0.05\) and \(\lambda =0.20\), see Figures 10 and 11 in online appendix.

The detailed CUSUM series can be found in Figures 12 and 13 in online appendix.

References

Adalid R, Detken C (2007) Liquidity shocks and asset price boom/bust cycles. ECB Working Paper 732, European Central Bank

Alessi L, Detken C (2009) “Real time” early warning indicators for costly asset price boom/bust cycles: a role for global liquidity. Working Paper Series 1039, European Central Bank

Baker D (2008) The housing bubble and the financial crisis. Real-world economics review 46. http://paecon.net/PAEReview/issue46/Baker46.pdf

Balcilar M (2007) mFilter: Miscellaneous time series filters. R package version 0.1-3. https://CRAN.R-project.org/package=mFilter/

Belke A, Orth W, Setzer R (2008) Sowing the seeds of the subprime crisis—does global liquidity matter for housing and other asset prices. Int Econ Econ Policy 5:403–24

Bernanke B (2002) Asset-price “Bubbles” and monetary policy. Speech given before the New York Chapter of the National Association for Business Economics, New York, October 15

Blondell D, Hoang P, Powell JG, Shi J (2002) Detection of financial time series turning points: a new CUSUM approach applied to IPO cycles. Rev Quant Finance Acc 18:293–315

Campbell J, Shiller RJ (1987) Cointegration and tests of present value models. J Polit Econ 95:1062–88

Case KE, Shiller RJ (2003) Is there a bubble in the housing market? Brook Pap Econ Act Econ Stud Prog Brook Inst 34(2):299–362

Demyanyk Y, van Hemert O (2011) Understanding the subprime mortgage crisis. Rev Financ Stud 24(6):1848–80

Dreger C, Kholodilin KA (2011) An early warning system to predict the house price bubbles. Discussion Papers of DIW Berlin 1142, DIW Berlin, German Institute for Economic Research

Dreger C, Wolters J (2009) Geldpolitik und Vermgensmärkte. Vierteljahreshefte zur Wirtschaftsforschung 78(1):56–65

Ferreira F, Gyourko J (2011) Anatomy of the beginning of the housing boom: U.S. neighborhoods and metropolitan areas, 1993–2009. Samuel Zell and Robert Lurie Real Estate Center, Working Paper 714

Freese J (2015) The regional pattern of the U.S. house price bubble—an application of SPC to city level data. Rev Econ 66(2):185–224

Gallin J (2004) The long-run relationship between house prices and rents: evidence from local housing markets, finance and economics discussion series divisions of research and statistics and monetary affairs, federal reserve board, Washington, D.C. 2004-50

Goodhart C, Hofmann B (2008) House prices, money, credit and the macroeconomy. Oxf Rev Econ Policy 24:180–205

Gurkaynak RS (2008) Econometric tests of asset price bubbles: taking stock. J Econ Surv 22(1):166–86

Hagerty JR (2009) Who’s to blame for the housing bubble? Wall Street J. http://blogs.wsj.com/developments/2009/11/16/whos-to-blame-for-the-housing-bubble/

Hamilton JD (1994) Time series analysis. Princeton University Press, Princeton

Hawkins DM, Olwell DH (1998) Cumulative sum charts and charting for quality improvement. Springer, New York

Himmelberg C, Mayer C, Sinai T (2005) Assessing high house prices: bubbles, fundamentals and misperceptions. J Econ Perspect Am Econ Assoc 19(4):67–92

Homm U, Breitung J (2012) Testing for speculative bubbles in stock markets: a comparison of alternative methods. J Financ Econom 10(1):198–231

Kizys R, Pierdzioch C (2009) Changes in the international comovement of stock returns and asymmetric macroeconomic shocks. J Int Financ Mark Inst Money 19(2):289–305

Knoth S (2006) The art of evaluating monitoring schemes—how to measure the performance of control charts? In: Lenz H-J, Wilrich P-T (eds) Frontiers in statistical quality control 8. Physica Verlag, Heidelberg, pp 74–99

Knoth S (2018) spc: Statistical process control—calculation of ARL and other control chart performance measures. R package version 0.6.0. https://CRAN.R-project.org/package=spc/

Lucas JM, Saccucci MS (1990) Exponentially weighted moving average control schemes: properties and enhancements. Technometrics 32(1):1–29

Mikhed V, Zemcik P (2009) Do house prices reflect fundamentals? Aggregate and panel data evidence. J Hous Econ 18(2):140–49

Mishkin FS (2011) Over the cliff: from the subprime to the global financial crisis. J Econ Perpect 25(1):49–70

Montgomery DC (2013) Statistical quality control. An introduction. Wiley, Hoboken

Moustakides GV (1986) Optimal stopping times for detecting changes in distributions. Ann Stat 14:1379–87

Nishina K (1992) A comparison of control charts from the viewpoint of change-point estimation. Qual Reliab Eng Int 8:537–41

Pfaff B (2008a). VAR, SVAR and SVEC models: implementation within R Package vars. J Stat Softw 27(i04). https://doi.org/10.18637/jss.v027.i04

Pfaff B (2008b) Analysis of integrated and cointegrated time series with R, 2nd edn. Springer, New York (ISBN: 0-387-27960-1)

Phillips PCB, Yu J (2011) Dating the timeline of financial bubbles during the subprime crisis. Quant Econ 2:455–491

Phillips PCB, Wu Y, Yu J (2011) Explosive behavior in the 1990s Nasdaq: when did exuberance escalate asset values? Int Econ Rev 52(1):201–226

Pinto E (2009) Acorn and the housing bubble. Wall Street J. https://www.wsj.com/articles/SB10001424052748703298004574459763052141456. Accessed 16 Dec 2015

Ravn MO, Uhlig H (2002) On adjusting the Hodrick-Prescott filter for the frequency of observations. Rev Econ Stat 84(2):371–80

Roberts SW (1959) Control-charts-tests based on geometric moving averages. Technometrics 1:239–50

Schaller H, van Norden S (2002) Fads or bubbles? Empir Econ 27:335–62

Shewhart WA (1926) Quality control charts. Bell Syst Tech J 5:593–603

Shiller RJ (2007) Understanding recent trends in house prices and home ownership. Working Papers 28, Yale University, Department of Economics

Sims CA, Stock JH, Watson MW (1990) Inference in linear time series models with some unit roots. Econometrica 58(1):161–82

Srivastava MS, Wu Y (1997) Evaluation of optimum weights and average run lengths in EWMA control schemes. Commun Stat Theory Methods 26(5):1253–67

Standard and Poor’s (2012) http://www.standardandpoors.com/home/en/us

Taylor M, Peel D (1998) Periodically collapsing stock price bubbles: a robust test. Econ Lett 61:221–28

Theodossiou PT (1993) Predicting shifts in the mean of a multivariate time series process: an application in predicting business failures. J Am Stat Assoc 88:441–49

Watson MW (1994) Vector autoregressions and cointegration. In: Engle RF, McFadden DL (eds) Handbook of econometrics, volume IV, chapter 47. Elsevier Science B.V, Amsterdam

White LJ (2010) Preventing bubbles: what role for financial regulation?. Stern School of Business, New York University, New York

Wuertz D, Setz, T Chalabi Y (2017). fUnitRoots—modeling trends and unit roots. R package version 3010.78. http://www.rmetrics.org

Yashchin E, Philips TK, Stein DM (1997) Monitoring active portfolios using statistical process control. In: Amman H et al (eds) Computational approaches to economic problems. Selected papers from the 1st conference of the Society for Computational Economics. Kluwer Academic Publishers, Dordrecht, pp 193–205

Zeileis A, Leisch F, Kleiber C, Hornik K (2005) Monitoring structural change in dynamic econometric models. J Appl Econom 20:99–121

Zeileis A, Grothendieck G (2005) zoo: S3 infrastructure for regular and irregular time series. J Stat Softw 14(6):1–27

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Berlemann, M., Freese, J. & Knoth, S. Dating the start of the US house price bubble: an application of statistical process control. Empir Econ 58, 2287–2307 (2020). https://doi.org/10.1007/s00181-019-01648-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-019-01648-x