Abstract

Households’ stock market participation has significant effects on savings and on an economy’s financial development and performance. Yet participation into capital markets is limited and quite heterogonous both among and within several countries. This phenomenon represents an empirical puzzle whose understanding is rather incomplete. In this work, we exploited a combination of datasets for nine European countries and used different econometric specifications that allow to control for endogeneity of financial literacy and human capital, to assess the role of several variables in affecting the probability to participate in the stock market in year 2010. Besides socio-demographic variables, we found that financial literacy has a positive and significant effect on stock market participation, together with the level of human capital and social interaction. Country level differences are explained by such institutional factors as the effectiveness of the education system and by the attractiveness of the stock markets.

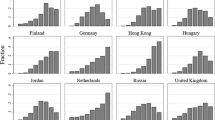

Source: Authors’ calculation using SHARE database. Data are provided for 5-year cohort groups (apart from 1966 to 1975, due to low number of observations)

Source: Authors’ calculation using SHARE database. For details on financial literacy groups see Appendix 2

Source: Authors’ calculation using SHARE database

Source: Authors’ calculation using SHARE database. Income quintiles are country-specific

Source: Authors’ calculation using SHARE database. Wealth quintiles are country-specific

Source: Authors’ calculation using International Historical Statistics. X axis: 5-year average student–teacher ratio for 5-year cohort groups at age 6–15 (some older cohorts were merged with others in case of low number of observations or lack of data). Y axis: fraction of individuals participating in the stock market for each cohort group and country

Source: Authors’ calculation using Global Financial Database. X axis: 5-year averages of Sharpe-ratios for each 5-year cohort-groups and countries. Y axis: fractions of individuals participating in the stock market for each cohort group and country

Similar content being viewed by others

Notes

Also the significant increase of employee financial plans, either directly through employee share ownership (ESO) or indirectly through intermediaries like Employee stock ownership plans (ESOP) or profit sharing (PS) have provided a relevant support to individuals’ demand for risky assets. These financial plans, also linked to defined contribution schemes, have empirically proven to favor higher productivity, strengthen corporate governance and competitiveness of firms (Kaarsemaker et al. 2010; Soppe and Houweling 2014). Most importantly, these financial plans have also improved the financial outlook of workers, equipping them with more sophisticated financial techniques and thus resulting in better financial decisions in terms of savings, risky asset participation and retirement planning.

This paper uses data from SHARE wave 4 release 1.1.1, as of March 28th 2013 (https://doi.org/10.6103/SHARE.w4.111), and SHARELIFE release 1, as of November 24th 2010 (https://doi.org/10.6103/SHARE.w3.100). The SHARE data collection has been primarily funded by the European Commission through the 5th Framework Programme (Project QLK6-CT-2001-00360 in the thematic programme Quality of Life), through the 6th Framework Programme (Projects SHARE-I3, RII-CT-2006-062193, COMPARE, CIT5- CT-2005-028857, and SHARELIFE, CIT4-CT-2006-028812) and through the 7th Framework Programme (SHARE-PREP, N° 211,909, SHARE-LEAP, N° 227,822 and SHARE M4, N° 261,982). Additional funding from the US National Institute on Aging (U01 AG09740-13S2, P01 AG005842, P01 AG08291, P30 AG12815, R21 AG025169, Y1-AG-4553-01, IAG BSR06-11 and OGHA 04-064) and the German Ministry of Education and Research as well as from various national sources is gratefully acknowledged (see http://www.share-project.org for a full list of funding institutions).”

Among few theoretical exceptions, see the model developed by Spataro and Corsini (2017).

In the recent years there has been burgeoning research on the measurement of financial literacy and its effects on household behaviour especially on retirement planning (Lusardi and Mitchell 2011; Van Rooij et al. 2012 among others) on savings and portfolio decisions (Jappelli and Padula 2013; Lusardi et al. 2017). For a review see Jappelli (2010).

Such differences among countries in stockholding could also arise from differences in cultural norms which are likely to be associated with apparent differences in risk tolerance levels or perception of the risk of the financial options. Additionally, changes in participation rates in risky asset markets could be influenced by the nature of society the worker belongs to. For example, in collectivistic societies, respondents are likely to receive financial assistance from their family and social networks; Pyles et al. (2016) showed that in these societies the perceived risk in financial decisions is lower than in individualistic societies (such as the Denmark, Sweden), where individuals are more likely to be left to fend for themselves. In the empirical analysis we take these issues into account by using control variables at both individual and cohort/country level.

We also tried to capture the difference in wages across different sectors; however, large number of missing values has forced us to drop the exercise.

The classification is based on direct stockholding percentages. Italy and Austria are low participating countries with less than 7% of the respondents holding stocks. The medium participation country group represents countries whose direct participation levels are between 8–20% and the high participating countries ranges from 21 to 40%. Broadly speaking stockholding increases form Southern to Northern Europe, with Switzerland as an exception.

Interactions of country dummies with Sharpe-ratios were also attempted, although they were not significant. In fact, Sharpe-ratios are country-specific and the latter, together with the country—group dummies and student–teacher ratios (cohort/country level) already capture the between-country variability in participation rates.

We recall that in SHARE database education years range from age zero to 25 (see Table 1).

The relative mathematical ability at age10 shows almost equal effect on financial literacy and school years, while relative score of language skills at age 10 is a better predictor of school years rather than financial literacy.

References

Alan, S. (2006). Entry costs and stock market participation over the life cycle. Review of Economic Dynamics, 9(4), 588–611. https://doi.org/10.1016/j.red.2006.06.003.

Amemiya, T. (1978). The estimation of a simultaneous equation generalized probit model. Econometrica 46(5), 1193–1205. https://doi.org/10.2307/1911443.

Arrondel, L., Calvo-Pardo, H., & Tas, D. (2012). Subjective return expectations, information and stock market participation: Evidence from France. Discussion Paper on Economics and Econometrics, University of Southampton. https://doi.org/10.2139/ssrn.2483909.

Arum, R. (1996). Do private schools force public schools to compete? American Sociological Review, 61(1), 29–46. https://doi.org/10.2307/2096405.

Bagliano, F., Fugazza, C., & Nicodano, G. (2014). Optimal Life-Cycle Portfolios for Heterogeneous Workers. Review of Finance, 18, 2283–2323. https://doi.org/10.1093/rof/rft046.

Behrman, J. R., Mitchell, O. S., Soo, C. K., & Bravo, D. (2012). How financial literacy affects household wealth accumulation. The American Economic Review, 102(3), 300–304. https://doi.org/10.1257/aer.102.3.300.

Bertaut, C., & Starr-McCluer, M. (2002). Household Portfolios in the US. In Household Portfolios, L. Guiso, M. Haliassos & T. Jappelli (Eds.), Cambridge: MIT Press.

Bertaut, C. C. (1998). Stockholding behavior of US households: Evidence from the 1983–1989 survey of consumer finances. Review of Economics and Statistics, 80(2), 263–275. https://doi.org/10.1162/003465398557500.

Bound, J., & Turner, S. (2007). Cohort Crowding: How Resource Affect College Attainment. Journal of Public Economics, 91(5), 877–899. https://doi.org/10.1016/j.jpubeco.2006.07.006.

Brav, A., Constantinides, G. M., & Geczy, C. C. (2002). Asset participation with heterogeneous consumers and limited participation: Empirical evidence. Journal of Political Economy, 110(4), 793–824. https://doi.org/10.1086/340776.

Brown, J. R., Ivković, Z., Smith, P. A., & Weisbenner, S. (2008). Neighbours matter: Causal community effects and stock market participation. The Journal of Finance, 63(3), 1509–1531. https://doi.org/10.1111/j.1540-6261.2008.01364.x.

Brown, S., & Taylor, K. (2007). Religion and education: Evidence from the National Child Development Study. Journal of Economic Behavior & Organization, 63(3), 439–460. https://doi.org/10.1016/j.jebo.2005.08.003.

Calvet, L. E., & Sodini, P. (2014). Twin picks: Disentangling the determinants of risk taking in household portfolios. Journal of Finance, 69(2), 867–906. https://doi.org/10.1111/jofi.12125.

Cameron, A. C., & Trivedi, P. K. (2010). Microeconometrics Using Stata. Texas: Stata Press, College Station.

Campbell, J. (2006). Household finance. The Journal of Finance, 61(4), 1553–1604. https://doi.org/10.1111/j.1540-6261.2006.00883.x.

Campbell, J. Y., & Cochrane, J. H. (2000). Explaining the poor performance of consumption-based asset pricing models. The Journal of Finance, 55(6), 2863–2878. https://doi.org/10.1111/0022-1082.00310.

Card, D., & Krueger, A. (1996). School resources and student outcomes: An overview of the literature and new evidence from North and South Carolina. Journal of Economic Perspectives, 10(4), 31–50. https://doi.org/10.1257/jep.10.4.31.

Christelis, D., Georgarakos, D., & Haliassos, M. (2013). Differences in portfolios across countries: Economic environment versus household characteristics. Review of Economics and Statistics, 95(1), 220–236. https://doi.org/10.1162/REST_a_00260.

Christelis, D., Jappelli, T., & Padula, M. (2010). Cognitive abilities and portfolio choice. European Economic Review, 54(1), 18–38. https://doi.org/10.1016/j.euroecorev.2009.04.001.

Cole, S., & Shastry, G. (2008). If you are so smart, why aren’t you rich? The effects of education, financial literacy and cognitive ability on financial market participation. Working Paper# 09–071. Harvard Business School, Wellesley College (unpublished), Cambridge MA.

Croson, R., & Gneezy, U. (2009). Gender differences in preferences. Journal of Economic Literature, 47(2), 1–27. https://doi.org/10.1257/jel.47.2.448.

Dimmock, S. G., & Kouwenberg, R. (2010). Loss-aversion and household portfolio choice. Journal of Empirical Finance, 17(3), 441–459. https://doi.org/10.1016/j.jempfin.2009.11.005.

Dimson, E., Marsh, P., & Staunton, M. (2002). Triumph of the optimists: 101 Years of global investment returns. New Jersey: Princeton University Press.

Fagereng, A., Gottlieb, C., & Guiso, L. (2017). Asset market participation and portfolio choice over the life-cycle. The Journal of Finance, 72(2), 705–750. https://doi.org/10.1111/jofi.12484.

Fonseca, R., Mullen, K. J., Zamarro, G., & Zissimopoulos, J. (2012). What explains the gender gap in financial literacy? The role of household decision making. Journal of Consumer Affairs, 46(1), 90–106. https://doi.org/10.1111/j.1745-6606.2011.01221.x.

Georgarakos, D., & Pasini, G. (2011). Trust, sociability, and stock market participation. Review of Finance, 15(4), 693–725. https://doi.org/10.1093/rof/rfr028.

Grohmann, A., Kouwenberg, R., & Menkhoff, L. (2015). Childhood roots of financial literacy. Journal of Economic Psychology, 51, 114–133. https://doi.org/10.1016/j.joep.2015.09.002.

Guiso, L., Haliassos, M., & Jappelli, T. (2003). Stockholding in Europe: where do we stand, and where do we go? Economic Policy 36, 123–170. https://doi.org/10.1111/1468-0327.00104.

Guiso, L., & Jappelli, T. (2005). Awareness and stock market participation. Review of Finance, 9(4), 537–567. https://doi.org/10.1007/s10679-005-5000-8.

Guiso, L., Sapienza, P., & Zingales, L. (2004). The role of social capital in financial development. The American Economic Review, 94(3), 526–556. https://doi.org/10.1257/0002828041464498.

Guiso, L., Sapienza, P., & Zingales, L. (2008). Trusting the stock market. The Journal of Finance, 63(6), 2557–2600. https://doi.org/10.1111/j.1540-6261.2008.01408.x.

Haliassos, M., & Bertaut, C. (1995). Why do so few hold stocks? The Economic Journal, 105(432), 1110–1129. https://doi.org/10.2307/2235407.

Hong, H., Kubik, J., & Stein, J. (2004). Social interaction and stock-market participation. The Journal of Finance, 59(1), 137–163. https://doi.org/10.1111/j.1540-6261.2004.00629.x.

Hurd, M., Van Rooij, M., & Winter, J. (2011). Stock market expectations of Dutch households. Journal of Applied Econometrics, 26(3), 416–436. https://doi.org/10.1002/jae.1242.

Jappelli, T. (2010). Economic Literacy: An International Comparison. The Economic Journal, 120(548), F429-F451. https://doi.org/10.1111/j.1468-0297.2010.02397.x.

Jappelli, T., & Padula, M. (2013). Investment in financial literacy and saving decisions. Journal of Banking and Finance, 37(8), 2779–2792. https://doi.org/10.1016/j.jbankfin.2013.03.019.

Kaarsemaker, E., Pendleton, A., & Poutsma, E. (2010). Employee share ownership. In A. Wilkinson, P. Gollan, M. Marchington, & D. Lewin (Eds.), The oxford handbook of participation in organizations (pp. 315–337). Oxford: Oxford University Press.

Kaustia, M., & Knüpfer, S. (2008). Do investors overweight personal experience? Evidence from IPO subscriptions. The Journal of Finance, 63, 2679–2702. https://doi.org/10.1111/j.1540-6261.2008.01411.x.

Kern, M. L., & Friedman, H. S. (2009). Early educational milestones as predictors of lifelong academic achievement, midlife adjustment, and longevity. Journal of Applied Developmental Psychology, 30(4), 419–430. https://doi.org/10.1016/j.appdev.2008.12.025.

Lam, D., & Schoeni, R. F. (1993). Effects of family background on earnings and returns to schooling. Journal of Political Economy, 101(4), 710–740. https://doi.org/10.1086/261894.

Liu, Y. J., Meng, J., You, W., & Zhao, L. (2014). Word-of-mouth communication, observational learning, and stock market participation. https://doi.org/10.2139/ssrn.2251570.

Lusardi, A., Michaud, P., & Mitchell, O. S. (2017). Optimal financial knowledge and wealth inequality. Journal of Political Economy, 125(2), 431–477. https://doi.org/10.1086/690950.

Lusardi, A., & Mitchell, O. S. (2011). Financial literacy and planning: Implications for retirement wellbeing in. In A. Lusardi & O. Mitchel (Eds.), Financial literacy: Implications for retirement security and the financial marketplace (pp. 17–39). New York: Oxford University Press.

Lusardi, A., & Scheresberg, C. D. B. (2013). Financial literacy and high-cost borrowing in the United States (No. w18969). National Bureau of Economic Research. https://doi.org/10.3386/w18969.

Malmendier, U., & Nagel, S. (2011). Depression babies: Do macroeconomic experiences affect risk-taking? The Quarterly Journal of Economics, 126(1), 373–416. https://doi.org/10.1093/qje/qjq004.

Männamaa, M., & Kikas, E. (2010). Cognitive profiles and their stability in different academic performance groups for math and language. In A. Toomela (Ed.), Systemic person-oriented study of child development in early primary school (pp. 95–131). Frankfurt: Peter Lang.

Marton, K. (2008). Visuo-spatial processing and executive functions in children with specific language impairment. International Journal of Language and Communication Disorders, 43, 181–200. https://doi.org/10.1080/16066350701340719.

Ostroff, C., & Schmitt, C. (1993). Configurations of organizational effectiveness and efficiency. Academy of Management Journal, 36(6), 1345–1361. https://doi.org/10.2307/256814.

Pyles, M. K., Li, Y., Wu, S., & Dolvin, S. D. (2016). Cultural influences on risk tolerance and portfolio creation. Journal of Behavioral and Experimental Finance, 9, 43–55. https://doi.org/10.1016/j.jbef.2016.01.001.

Soppe, A., & Houweling, R. (2014). Sharing in Modern companies: Employee financial participation in Netherlands (Delen in modern ondernemen: Financiële werknemersparticipatie in Nederland). Rotterdam: Erasmus Universiteit Rotterdam.

Spataro, L., & Corsini, L. (2017). Endogenous Financial Literacy, Saving, and Stock Market Participation. FinanzArchiv: Public Finance Analysis, 73(2), 135–162. https://doi.org/10.1628/001522117X14877521353555.

Staiger, D., & Stock, J. H. (1997). Instrumental variables regression with weak instruments. Econometrica, 65, 557–586. https://doi.org/10.2307/2171753.

Thomas, A., & Spataro, L. (2016). The effects of pension funds on markets performance: A review. Journal of Economic Surveys, 30(1), 1–33. https://doi.org/10.1111/joes.12085.

Thomas, A., Spataro, L., & Mathew, N. (2014). Pension funds and stock market volatility: An empirical analysis of OECD countries. Journal of Financial Stability, 11, 92–103. https://doi.org/10.1016/j.jfs.2014.01.001.

Van der Sluis, S., de Jong, P., & Van der Leij, A. (2004). Inhibition and shifting in children with learning deficits in arithmetic and reading. Journal of Experimental Child Psychology, 87, 239–266. https://doi.org/10.1016/j.jecp.2003.12.002.

Van Rooij, M., Lusardi, A., & Alessie, R. (2011). Financial literacy and stock market participation. Journal of Financial Economics, 101(2), 449–472. https://doi.org/10.1016/j.jfineco.2011.03.006.

Van Rooij, M., Lusardi, A., & Alessie, R. (2012). Financial literacy, retirement planning and household wealth. The Economic Journal, 122(560), 449–478. https://doi.org/10.1111/j.1468-0297.2012.02501.x.

Vestman, R. (2010). Limited stock market participation among renters: Explanations and welfare consequences. Stockholm: The Institute for Financial Research (SIFR).

Wooldridge, J. M. (2002). Econometric analysis of cross section and panel data. Cambridge: The MIT Press.

Yoong, J. (2011). Financial illiteracy and stock market participation: Evidence from the RAND American Life Panel. In O. S. Mitchell & A. Lusardi (Eds.), Financial literacy: Implications for retirement security and the financial marketplace (pp. 76–97). New York: Oxford University Press.

Acknowledgements

We are grateful to the participants at the Seminar at Department of Economics and Management, University of Pisa, at the «13th Workshop on Pension, Saving and Insurance, Paris», at the «Institutional and Individual Investors: Saving for old age» Conference, University of Bath, at GRASS IX Workshop, IMT Lucca, at XXIV MBF Rome Conference, at 52nd TIES conference, IIM Kozhikode, Michael Haliassos, Maurizio Fiaschetti, Angela Parenti, Davide Fiaschi, Thomas Renström and Valeria De Bonis, Alessandro Belmonte, Nebojsa Dimic for helpful insights and suggestions on a previous version of this paper. The usual disclaimer applies.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Ethical Approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Appendix

Appendix

Appendix 1

See Table 5.

Appendix 2: Financial Literacy in SHARE

The questions used to construct the financial literacy indicator are set out below. Possible answers are shown on cards displayed by the interviewer who is instructed not to read them out to respondents:

-

1.

If the chance of getting a disease is 10%, how many people out of 1000 can be expected to get the disease? The possible answers are 100, 10, 90, 900 and another answer.

-

2.

2. In a sale, a shop is selling all items at half price. Before the sale a sofa costs 300 euro. How much will it cost in the sale? The possible answers are 150, 600 and another answer.

-

3.

3. A second hand car dealer is selling a car for 6000 euro. This is two-thirds of what it costs new. How much did the car cost new? The possible answers are 9000, 4000, 8000, 12,000, 18,000 and another answer.

-

4.

4. Let’s say you have 2000 euro in a savings account. The account earns 10 per cent interest each year. How much would you have in the account at the end of the second year? The possible answers are 2420, 2020, 2040, 2100, 2200, 2400.

If a person answers (1) correctly she is then asked (3) and if she answers correctly again she is asked (4). Answering (1) correctly results in a score of 3, answering (3) correctly but not (4) results in a score of 4 while answering (4) correctly results in a score of 5. On the other hand, if she answers (1) incorrectly she is directed to (2). If she answers (2) correctly she gets a score of 2 while if she answers (2) incorrectly she gets a score of 1.

The questions were asked in national languages like German, Italian, Swedish, Danish and Dutch. As for the Austria, the language used was German. The respondents from Belgium questions were provided in French or Flemish and for the Switzerland, the questionnaires were provided in Italian, German or French.

The actual range of responses were as follows: For question 1, the range of response is five, question 2 has three alternative answers, question 3 have six responses and finally question 4 has seven responses.

Appendix 3

See Table 6.

The detailed methodology of calculating the Sharpe-ratios is the following. The data on the return index is computed from Global Financial Database. The returns on risky assets and safe asset returns are calculated separately from the return index by applying the formula

where Y1 is the current return index value and Y0 is the base return index. Then we calculate the average returns by subtracting the return of the risky asset (Rf) from the return from safe asset\(\left( {{R_0}} \right):\frac{{{R_f} - {R_o}}}{{stdev({R_f})}}.\)

Finally, the average returns are divided by the standard deviation of risky assets that is annualised by multiplying by \(\sqrt 2\)of the respective years.

Appendix 4

See Table 7.

Appendix 5

See Table 8.

Rights and permissions

About this article

Cite this article

Thomas, A., Spataro, L. Financial Literacy, Human Capital and Stock Market Participation in Europe. J Fam Econ Iss 39, 532–550 (2018). https://doi.org/10.1007/s10834-018-9576-5

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10834-018-9576-5