Abstract

Failure of critical national infrastructures can cause disruptions with widespread economic impacts. To analyze these economic impacts, we present an integrated modeling framework that combines: (1) geospatial information on infrastructure assets/networks and the natural hazards to which they are exposed; (2) geospatial modeling of the reliance of businesses upon infrastructure services, in order to quantify disruption to businesses locations and economic activities in the event of infrastructure failures; and (3) multiregional supply-use economic modeling to analyze wider economic impacts of disruptions to businesses. The methodology is exemplified through a case study for the United Kingdom. The study uses geospatial information on the location of electricity infrastructure assets and local industrial areas, and employs a multiregional supply-use model of the UK economy that traces the impacts of floods of different return intervals across 37 subnational regions of the UK. The results show up to a 300% increase in total economic losses when power outages are included in the risk assessment, compared to analysis that just includes the economic impacts of business interruption due to flooded business premises. This increase indicates that risk studies that do not include failure of critical infrastructures may be underestimating the total losses.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Critical infrastructure systems, such as energy, transportation, water, waste, and digital communications, are the backbone of modern economies and societies (Hall et al. 2017). Failures of these systems can result in large-scale economic losses and social disruptions. Prominent examples of such catastrophic failures include, among others, communications failures and electricity blackouts during hurricanes Sandy (2012) and Irma (2015) in the United States (Kwasinski 2013), and multiple infrastructure failures in the United Kingdom during floods in 2007 and 2015 (Pitt 2008; Kemp 2016). Such incidents are becoming increasingly common, as evidenced by the increased frequency and severity of large electricity blackouts over the last decades (Hines et al. 2009; Bompard et al. 2013). Given the increasing economic costs of big disaster events, with billion dollar events becoming more frequent (AON 2016), there is a growing interest in improving the quantification of infrastructure failure impacts. Such interest ranges from the policymaker’s concern to prioritize asset protection in order to maintain socioeconomic order, to the operator’s interests in resilience planning to maintain continuous supply to avoid fines and reputational risks, to the insurers’ interests in reducing their risk exposure and liabilities.

The economic disruption and losses due to infrastructure failure is a complex phenomenon to analyze. Businesses depend upon infrastructure (such as electricity, gas, and tele-communications) for a wide variety of purposes. Information on the location and performance of the physical networks that supply these services is difficult to obtain. Moreover, infrastructure networks are dependent (and sometimes interdependent) on each other, meaning that failure can propagate between networks, with cascading effects. Observations of failure events are rare and incomplete. The complex circumstances surrounding any particular event are very unlikely to be replicated in the future. Comprehensive damage assessments have therefore tended to rely upon system simulation modeling, which provides the capacity to explore a very wide range of possible failure events and economic circumstances.

Simulating and understanding the propagating impacts of infrastructure failure on businesses and the economy requires a framework that addresses: (1) the processes and consequences of physical infrastructure failures in terms of physical capital losses and service flow disruptions; and (2) the resulting business disruptions and economic flow losses across the wider macroeconomic sectors. Additionally, due to the spatial and temporal nature of both infrastructure failure itself and the economy it affects, it is necessary to include the wider multi-regional losses and the possible gains under substitution effects. This article aims to create an integrated methodological framework in which the aforementioned phenomena are represented.

Infrastructure failure analyses generally come under the topics of infrastructure vulnerability, risk, and resilience analysis, which are extensively researched topics. For detailed reviews of these topics and studies see Zio (2009), Aven (2011), Yusta et al. (2011), and Ouyang (2014). The key focus of these studies has been on representing infrastructure interdependencies (Rinaldi et al. 2001), and measuring failures of one or more interconnected infrastructures in terms of physical network connectivity failure, service flow disruptions, and customer impacts (Hu et al. 2016; Pant et al. 2016, 2017; Poljanšek et al. 2017; Thacker et al. 2017a, b, c). Even though the focus of most of these studies has been on modeling failures due to natural hazard-induced disasters, relatively few of these studies distinguish between impacts within and outside the hazard areas (Pant et al. 2017).

In the disaster impact literature, the cost of infrastructure failure is often estimated in terms of monetary values of physical stocks that are damaged or have failed due to direct exposure to a natural hazard (Scawthorn et al. 2006; Meyer et al. 2013). More specifically, the focus is often on the physical impacts to the directly affected area only (Gerl et al. 2016). Neglecting the impacts outside the directly affected hazard area may result, however, in suboptimal investment decisions due to the implicit underestimation of risk. To address this limitation, we focus on the two main causes of cascading effects outside the hazard area: (1) the impacts through critical infrastructure system failures, which can propagate disruptions outside the hazard area due to a reduction in infrastructure services and network effects; and (2) the impacts that spread through industrial supply chains, and cause losses through forward and backward linkages in the economy.

Estimating the wider economic impacts of natural hazard-induced disasters is now a well-studied topic in which input–output (IO) and computable general equilibrium (CGE) models are extensively applied (Okuyama and Santos 2014). IO and CGE models can be interpreted as analytical techniques to represent an economic system and can be used to model the effects of changes to this system. Recently, many studies in this field have focused on improving the models’ capability to handle interregional impacts and supply-side disruptions. Examples are studies on both national (Schulte in den Bäumen et al. 2015; Oosterhaven and Tobben 2017) and international scales (Koks and Thissen 2016), varying from IO-based models (Okuyama 2015) and hybrid models (Hallegatte 2008; Oosterhaven and Bouwmeester 2016), which combine elements of both IO and CGE models, to full-fledged CGE models (Rose et al. 2016). These models represent the (monetary value of) the flow of resources between economic sectors, with CGE models also simulating price adjustments due to changes in supply and demand. They usually include infrastructure as economic sectors (for example, energy, transport) in an equivalent way to other economic sectors, while not representing the critical role of infrastructure. A weakness of these studies is that they do not integrate the geospatial representation of an infrastructure with its equivalent economic sector.

Studies that assess the economic impacts of critical infrastructure failure mainly use the framework of the inoperability input–output model (IIM) (Haimes and Jiang 2001; Anderson et al. 2007; Jonkeren and Giannopoulos 2014). The IIM and its variants are derived from the Leontief IO models (Haimes et al. 2005). These studies, however, either do not include: (1) a spatially explicit representation of critical infrastructure; or (2) they do not represent the full economic system, but rather are focused only on the infrastructure sectors. Recent IIM studies of port disruptions have combined infrastructure failures with multi-commodity import and export flow disruptions across multiple regions (Pant et al. 2011, 2015; MacKenzie et al. 2012). Despite multiple advances in this field over the past years, an approach that fully integrates the physical processes of critical infrastructure failure with economic analysis of business and supply-chain disruptions has not yet been achieved.

In this study, we develop a framework to estimate the impacts of natural hazard-induced disasters on business activity, industrial production capacities, and critical infrastructure failure. We begin by combining detailed spatial information on economic activity, infrastructure service areas, and the spatial intensity of natural hazards to obtain the disruption in economic activity due to failure of the most vulnerable assets. Then this combined disruption of economic activity and infrastructure failure is translated into a disruption to the wider economy due to economic dependence on infrastructure. Finally, the total macroeconomic impacts, as a result of disruption to supply chains, are estimated through a macroeconomic model—the Multi-Regional Impact Assessment (MRIA) model (Koks and Thissen 2016). The MRIA model is a multiregional supply-use model that estimates a new economic equilibrium in the short-term disaster aftermath. We demonstrate the proposed methodological framework through an application to electricity substations and business areas exposed to flooding in the United Kingdom (UK).

The remainder of this article is structured as follows. Section 2 outlines the definition of losses that are considered within this study. Section 3 provides an overview of the methodological framework required to estimate the economic impacts due to a combined disruption of infrastructure failure and businesses. Section 4 describes an application of the methodology to the UK. Section 5 presents results from the analysis and Sect. 6 offers discussion of these results and their broader implications for policy and practice. Finally, Sect. 7 provides the study’s conclusions and outlines directions for future research.

2 Categories of Economic Loss

We follow two different causal pathways to estimate economic losses due to a natural hazard event. The comparison of the two branches allows us to investigate how infrastructure failure may alter the economic system. We only focus on the impacts to businesses, therefore households are only considered in the analysis insofar as they are indirectly effected as consumers of the outputs of businesses. Therefore, when referring to economic activities, we specifically refer to industrial and/or business activities. A comprehensive analysis of the economic impacts of natural hazards would also include direct damage to households and the wider (economic) effects of the disruption to, and recovery of, households. We exclude from this study these phenomena, which have been quite widely studied elsewhere by Bubeck et al. (2012) and Haer et al. (2016), for example, to assist clarity of exposition and interpretation of the results.

In the first branch of our framework, the economic losses are estimated by looking at the direct business disruption due to a hazard event. This is referred to as “hazard only disruption.” In the second branch, the economic losses are estimated by looking at both the direct business disruption due to the hazard as well as the business disruption due to infrastructure failure (that is, lost provision of infrastructure services). The second branch is referred to as “systemic disruption.”

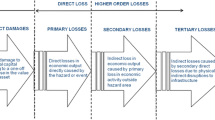

Figure 1 illustrates the direct spatial impacts of the two branches, exemplified with a flood hazard. Panel A shows the spatial impacts when only considering the flood and panel B shows the spatial impacts in the case of a systemic disruption. When only considering direct business disruption (panel A), we have two types of economic output losses, following the standard definitions in the disaster impact literature: direct output losses in the flooded area and indirect output losses outside the flooded area. The direct output losses can be described as the impacts that occur to businesses directly affected by a natural hazard (dark blue colored, indicated by the number “1”). These businesses have supply chain interactions with businesses inside and outside the flooded area. The indirect output losses (red colored, indicated by the number “4”) can be described as the system-wide economic effects to firms and industries via backward and/or forward supply chain linkages (Okuyama and Santos 2014).

Hypothetical cartogram depicting flood hazard impact areas and business disruption. The figure illustrates the two loss estimation branches and the difference in affected business activities. Panel A shows the economic activities affected due to the flood only. Panel B shows the affected business activities due to a systemic disruption

In the case of a systemic disruption, as well as considering the damage and disruption in panel A, we also consider the impacts of infrastructure damage in the flooded zone. These infrastructure assets are depicted as purple dots in Fig. 1 and they supply all of the businesses within a service area, depicted by a grey polygon in Fig. 1. Note that the service area may extend beyond the flooded area. The direct output losses can now be split up: (1) direct output losses due to the natural hazards only (dark blue colored, indicated by the number “1”); (2) direct output losses due to infrastructure failure only (purple colored, indicated by the number “2”); and (3) direct output losses due to both a natural hazard and infrastructure failure (maroon colored, indicated by the number “3”). As becomes apparent from Fig. 1, the direct output losses due to infrastructure failure can substantially increase the total direct output losses. Even though in both cases the resulting cascading effects will result in supply chain disruptions, there will be a significant difference in the way businesses are directly affected. In the case of business disruption due to infrastructure failure, the business itself will (in most cases) not be damaged. As soon as the infrastructure asset is repaired, production can continue again. For flooded businesses, however, there will be additional asset losses that result in additional cost for repair and recovery; and potentially prolonged periods of business inactivity while all repairs take place. All these direct output losses result in indirect output losses, following the same aforementioned definition.

3 Methodology

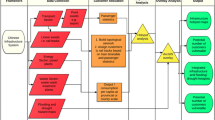

Figure 2 provides an overview of the methodology developed to assess the impacts of disruption on business activity and industrial production capacities due to natural hazard-induced disasters and the failure of critical infrastructure. The process of mapping business dependency on infrastructure, which is described below, applies to a single type of infrastructure with fixed spatial service coverages. Our two loss estimation approaches are displayed in Fig. 2. The first approach estimates only the impacts of business activity disruption in the area affected by the natural hazard (the left orange-red color schemed pillar in Fig. 2). The second approach, systemic disruption, estimates the impacts of business activity disruption, both due to the natural hazard and as a consequence of the natural hazards leading to infrastructure failure and loss of supply of essential services to businesses (the right purple color schemed pillar in Fig. 2).

Generalized framework of our approach. The model assesses the economic impacts of disruptions from natural hazards for two loss estimation approaches: (1) considering business disruptions in the area affected by the natural hazard only (left pillar—orange–red color scheme); and (2) considering systemic impacts of business disruptions and infrastructure failures, both within and external to the natural hazard area (right pillar—purple color scheme)

The first step, as illustrated in panel 1, Fig. 2, is to identify the dependencies between the business activities and the infrastructural assets and to connect them in a single (geospatial) set. The next step (panel 2, Fig. 2) is to overlay natural hazard information with the business activities and infrastructure assets to determine which parts of the system are exposed to natural hazards. The third step (panel 3, Fig. 2) is where we use the exposed asset set to create an exhaustive set of potential failure combinations (of these assets) to estimate the system-wide consequences of failure. This set of combinations is created to account for the fact that there is uncertainty around which infrastructure assets may fail at the same time. Floods in different areas often do not occur at the same time. As such, these combinations are critical to understand the wider impact of a combined failure in different areas. Finally, the set of failure combinations, representing scenarios of the consequences of natural hazard events, is used to estimate the wider economic impacts (panel 4, Fig. 2). The MRIA model (Koks and Thissen 2016) is applied to estimate these macroeconomic impacts for both approaches. Figure 2 shows the flow through the methodology, starting from the steps within panel 1 and proceeding downward towards the steps in panel 4 to create a coherent analytical framework. The subsections of Sect. 3 provide a mathematical description of each element within Fig. 2.

3.1 Mapping Business Dependency on Infrastructures

Generally, infrastructures with fixed spatial service coverages are called utility services such as electricity, gas, water, and digital communications. Governed by the direction of flow of resources, the assets of utility services have been classified by Pant et al. (2017) and Thacker et al. (2017c) as: (1) sources—which generate resources; (2) intermediates—which transmit the resources; and (3) sinks—which connect to the final users to provide the resources for their services. Here we look at the specific dependency of the businesses on the infrastructure sinks. The infrastructure under consideration is represented as a collection of all its point sink assets that are denoted as \(I = \left\{ {\alpha_{1} , \ldots ,\alpha_{n} } \right\}\). Similarly, the collection of economic activities (or businesses) under consideration are denoted by the set \(B = \left\{ {\beta_{1} , \ldots ,\beta_{z} } \right\}\). Each infrastructure asset \(i\) is associated with a service area, given by \(a\left( {\alpha_{i} } \right)\), and similarly each economic activity \(j\) occurs in an area \(a\left( {\beta_{j} } \right)\). The collection of areas served by the infrastructure and the economic activities are respectively given by the sets \(A\left( I \right) = \left\{ {a\left( {\alpha_{1} } \right), \ldots , a\left( {\alpha_{n} } \right)} \right\}\) and \(A\left( B \right) = \left\{ {a\left( {\beta_{1} } \right), \ldots , a\left( {\beta_{n} } \right)} \right\}\). We assume that each infrastructure asset serves a unique area with respect to other assets, which means \(a\left( {\alpha_{i} } \right) \cap a\left( {\alpha_{p} } \right) = \emptyset ,\quad \forall \alpha_{i} ,\alpha_{p} \in I,i \ne p\). The economic measure per unit area (for example, employment numbers per unit area) associated with economic activity \(j\) is denoted as a number \(\left| {\varphi \left( {\beta_{j} } \right)} \right|\), from which we can estimate the total economic measure over the area \(a\left( {\beta_{j} } \right)\) as \(\left| {s\left( {\beta_{j} } \right)} \right| = \left| {\varphi \left( {\beta_{j} } \right)} \right|\left| {a\left( {\beta_{j} } \right)} \right|\). The set \(S\left( B \right) = \left\{ {\left| {s\left( {\beta_{1} } \right)} \right|, \ldots ,\left| {s\left( {\beta_{z} } \right)} \right|} \right\}\) then denotes all economic measures corresponding to their economic activities.

We calculate the total measurable economic activity associated with each infrastructure asset by summing the measures of the economic activities located within its service area. This is achieved by computing the spatial intersection of the infrastructure assets and economic activity areas. If \(a\left( {\alpha_{i} \cap \beta_{j} } \right)\) denotes the intersecting area between infrastructure asset i and economic activity j, then the economic measure associated with the infrastructure asset service is estimated as \(\left| {\varphi \left( {\beta_{j} } \right)} \right|\left| {a\left( {\alpha_{i} \cap \beta_{j} } \right) } \right|\). The total economic measure associated with the infrastructure asset i is estimated by summing all economic activities that it intersects, given as \(\left| {s\left( {\alpha_{i} } \right)} \right| = \sum\nolimits_{j} {\left| {\varphi \left( {\beta_{j} } \right)} \right|\left| {a\left( {\alpha_{i} \cap \beta_{j} } \right) } \right|}\). We note that \(\left| {a\left( {\alpha_{i} \cap \beta_{j} } \right) } \right| = 0\) if there is no spatial intersection between an infrastructure asset and economic activity. The set \(S\left( I \right) = \left\{ {\left| {s\left( {\alpha_{i} } \right)} \right|, \ldots ,\left| {s\left( {\alpha_{n} } \right)} \right|} \right\}\) denoting all economic measures associated with infrastructure assets can be assembled by following the above process. Elements of \(S\left( I \right)\) denote the dependency of businesses on the infrastructure service.

3.2 Determine Infrastructure System Exposure and Vulnerability to Natural Hazards

The next step is to estimate the exposure of infrastructures and economic activities to the natural hazard. Although we have a hazard map derived as a continuous field, it can be denoted as a set of discrete hazard elements \(H = \left\{ {h_{1} , \ldots h_{m} } \right\}\) over space. Here \(h_{k}\) denotes the hazard over an area \(a\left( {h_{k} } \right)\) with a magnitude (for example, flood depth, earthquake intensity) \(y\left( {h_{k} } \right)\), giving the sets \(A\left( H \right) = \left\{ {a\left( {h_{1} } \right), \ldots a\left( {h_{m} } \right) } \right\}\) and \(Y\left( H \right) = \left\{ {y\left( {h_{1} } \right), \ldots y\left( {h_{m} } \right) } \right\}\) of hazard outlines and magnitudes respectively. The infrastructure assets and economic activities are intersected with the hazard extent to first infer exposure to the natural hazard. We assume that the hazard causes failure of an infrastructure asset only when it exceeds a threshold value, given by \(y_{\text{tr}}\). This assumption provides a simplified understanding of failure criteria, instead of a more nuanced understanding of probabilistic failures in terms of asset fragilities based on probabilistic hazards (Winkler et al. 2010; Ouyang et al. 2012). As will be demonstrated later in our case-study on flooding of electricity substations, such fragility curves are not available for flood hazard assessment and in the UK the industry guidelines also prescribe assessing substation equipment failures based on the height of critical equipment above flood levels (Energy Networks Association 2018). Hence, the state of functionality of an infrastructure asset is assumed binary (0 = failed and 1 = no failure) given as:

The economic activities disrupted due to infrastructure disruptions are measured by assembling the sets of all economic measures associated with the failed/disrupted assets, given as

Similarly, the economic activities are also assumed to be disrupted if they are exposed to the natural hazard above a threshold \(y_{\text{tr}}\) (this threshold may be different to the infrastructure failure threshold). The failure state of the economic activity can be denoted by:

The amount of economic activity disrupted is measured by multiplying the per unit area measure by the area over which this economic activity is disrupted. Hence if economic activity \(\beta_{j}\) is exposed to the natural hazard \(h_{k}\) (above the chosen threshold) over area \(a\left( {\beta_{j} \cap h_{k} } \right)\) then its disruption is \(\left| {\varphi \left( {\beta_{j} } \right)} \right|\left| {a\left( {\beta_{j} \cap h_{k} } \right) } \right|\). The total disruption of the economic activity \(\beta_{j}\) due to the hazard exposure is estimated across all its exposure to the natural hazard, which is \(\left| {\bar{s}\left( {\beta_{j} } \right)} \right| = \sum\nolimits_{k} {\left( {1 - r\left( {\beta_{j} \cap h_{k} } \right)} \right)\left| {\varphi \left( {\beta_{j} } \right)} \right|\left| {a\left( {\beta_{j} \cap h_{k} } \right) } \right|}\). All economic activity disruptions due to the natural hazard can be assembled into a set \(\bar{S}\left( B \right) = \left\{ {\left| {\bar{s}\left( {\beta_{j} } \right)} \right|,\forall_{j} } \right\}\). How the businesses activities are effectively being impacted is illustrated in panel A and panel B in Fig. 1, for respectively set \(\bar{S}\left( B \right)\) and \(\bar{S}\left( I \right)\).

3.3 Create Set of Failure Combinations

The sets \(\bar{S}\left( I \right)\) and \(\bar{S}\left( B \right)\) show the economic activities disrupted by the natural hazard and through systemic disruptions. We are interested in comparing these two types of impacts with each other, and further, to look at multiple failure combinations of several infrastructure assets failing at the same time. A natural hazard could knock out more than one infrastructure asset at the same time and different natural hazards in different areas may occur at the same time. First, economic activities corresponding to each infrastructure asset are combined. From set \(\bar{S}\left( B \right)\) the set \(\overline{\overline{S}} \left( B \right) = \left\{ {\sum\nolimits_{j} {1_{ij} \left| {\bar{s}\left( {\beta_{j} } \right)} \right|} } \right\}\) is created, where \(1_{ij}\) is an indicator function whose value is one when economic activity \(\beta_{j}\) is within the service area of infrastructure asset \(\alpha_{i}\) and 0 otherwise. Each element of \(\overline{\overline{S}} \left( B \right)\) shows the total disruption to economic activities, given their independent flooding within an infrastructure service area. In the end, the set \(\overline{\overline{S}} \left( B \right)\) has the same numbers of elements as \(\bar{S}\left( I \right)\).

To understand multiple failure combinations, we simulate the exhaustive set of all possible failure combinations of infrastructure assets. If \(\left| {\bar{S}\left( I \right)} \right|\) denotes the number of elements of \(\bar{S}\left( I \right)\) then \(2^{{\left| {\bar{S}\left( I \right)} \right|}} - 1\) failure combinations are considered, denoted by the \(F\left( I \right) = { \mathcal{P}}\left( {\bar{S}\left( I \right)} \right)\backslash \emptyset\) where \({\mathcal{P}}\left( {\bar{S}\left( I \right)} \right)\) is the power set of \(\bar{S}\left( I \right)\) and the \(\backslash \emptyset\) operation means the empty set is removed from \({\mathcal{P}}\left( {\bar{S}\left( I \right)} \right)\). The disruptions to economic activity corresponding to each infrastructure failure combination are similarly assembled in the set \(F\left( B \right) = { \mathcal{P}}\left( {\overline{\overline{S}} \left( B \right)} \right)\backslash \emptyset\), with the same ordering as \(F\left( I \right)\). As will be seen later in the case study, our set of individual infrastructure failure cases is small, hence exhaustive sampling is possible. If the individual failure cases are several in number, then Monte Carlo sampling techniques could also be used to sample failure combinations (Nedic et al. 2006; Pant et al. 2016).

3.4 Estimate Macroeconomic Impacts

The next step is to integrate the outcomes of the vulnerability assessment and the set of failure combinations to provide an input for the macroeconomic model. As shown in the fourth panel of Fig. 2, for each set of failure combinations (both for \(F\left( I \right)\) and \(F\left( B \right)\)), the economic disruption (\(\delta\)) is estimated for all affected businesses (\(\beta_{j}\)) within each sector (\(k\)) for each region affected (r). We can denote a collection of economic activities (or businesses) that belong to a specific macroeconomic sector as the set \({\rm K}\left( B \right) = \left\{ {\kappa \left( {\beta_{1} } \right), \ldots ,\kappa \left( {\beta_{n} } \right)} \right\}\). This results in the vector \({\varvec{\updelta}}^{\varvec{r}}\), with a ratio of the business interruption for each sector in the macroeconomic model. To obtain the post-disaster production output, total production \(x_{k}^{r}\) of each affected sector in each affected region is multiplied with (1 − \(\delta_{k}^{r}\)). To estimate the disruption of each failure combination, we redefine the maximum production capacity as stated in Eq. 3. When no businesses of a specific sector in a region are affected by the flood, the related sector will have a maximum production capacity that equals its pre-disaster production capacity. As soon as at least one business associated with a sector is affected, the post-disaster production capacity will be equal to the sector’s production capacity multiplied with the disruption.

Using the post-disaster maximum production capacity, we can estimate the daily economic output losses with the use of the MRIA macroeconomic modeling framework. The MRIA calculates how trade flows both within a region and from and to other regions may change because of the disruption, either positively or negatively. This trade flow change is the main driver of indirect economic effects in the affected and surrounding regions (Koks and Thissen 2016). Wider-scale economic impacts may occur when the production capacity of a region is insufficient to take over all production from an affected region. Following a standard input–output modeling approach, the MRIA model assumes a demand-determined economy. In other words, the demand must be satisfied by the total supply.

The core model of the MRIA can be described as follows. The objective function of the model minimizes total production \({\mathbf{x}}\) over all regions (Eq. 4), subject to production meeting demand (Eq. 5). Industries aim to minimize their costs given the demand for products and the available technologies to produce them. These technologies describe how industries can make a variety of products from a specific set of inputs—the Leontief production function (Leontief 1951). Technologies are “owned” by the different industries in the different regions and are therefore only available to them. The MRIA model is based on the region-specific technologies of industries used to make different products derived from regional technical coefficient matrices. The technologies are inputs required to produce an output of different products. Products are produced at the lowest costs, and together with the demand for products in every region, these costs determine which technologies are used as well as the extent of their use. The range of inputs that each industry requires to make its variety of products represents its production technology and is described by the use table \({\mathbf{U}}\) (this table describes how many products an industry uses to make its products). The range of products that each industry can make using this technology is described by the supply table \({\mathbf{S}}\). The MRIA model is described by Eqs. 4–7, with \(p = 1, \ldots , P\), with \(P\) = number of products, with \(k\) and \(l = 1, \ldots , K\), with \(K\) = number of sectors,\(r = 1, \ldots , N\), with \(s = 1, \ldots , N\), and with \(N\) = number of regions. Matrices are denoted by bold capitals, vectors by bold small types, and scalars by italics; \({\hat{\mathbf{x}}}\) a diagonal matrix of \({\mathbf{x}}\), \({\mathbf{i}}\) a summation column with ones, and \({\mathbf{I}} = {\hat{\mathbf{i}}}\) the identity matrix.

The supply of products of all regions (\({\mathbf{S}}^{r} {\mathbf{i}}\)) should be equal to or larger than the demand (intermediate use \({\mathbf{U}}^{r} {\mathbf{i}}\) and final demand \({\mathbf{f}}^{r}\)) for these products from all regions (Eq. 5). The possibility of total demand to be lower than the total production capacity is an essential element in the model that allows for modeling inefficiencies in the economy due to limits in the production capacity in the disaster area. Production in all regions will take place at the lowest possible costs (industries minimize costs) given (intermediate and final) demand, the available technologies, and the maximum capacity of industries. The vector \({\varvec{\upeta}}\) defines the total import (\({\mathbf{m}}\)) share for product p demanded from region r (Eq. 6 and vector \(\varpi\) defines how much additional imports are required in the affected regions to satisfy intermediate and final demand for products that cannot be satisfied due to lost production capacity in their own region. For a complete description of the model, please refer to Koks and Thissen (2016).

To obtain the direct output losses for a specific failure combination, we simply sum the loss in production capacity of all sectors affected by the flood. These values are obtained before running the MRIA model. To obtain the total economic impacts (including both direct and indirect impacts) \(D\) of each failure combination, we take the sum of the difference of the new production capacities \(\overline{{ {\mathbf{x}}}}^{\varvec{r}}\), obtained as the solution of the MRIA model, with the pre-disaster production capacities \({\mathbf{x}}^{{\mathbf{r}}}\) within each region.

4 Application to Flooding in the United Kingdom

Figure 3 presents how the methodological framework described in Sect. 2 is put into the practice for the United Kingdom. Whereas the macroeconomic impacts are estimated for the whole of the UK, the actual direct flood impacts and infrastructure failure (and, consequently, the estimation of the business disruption) are focused on the southeast of England. The first part of this section explains the data that are used to estimate the direct business disruption and critical infrastructure failure for the southeast of England, whereas the second part will focus on the datasets used to estimate the macroeconomic impacts for the UK. Table 1 presents an overview of the different datasets that are being used in this study.

Presentation of the application of the Middle Layer Super Output Area (MSOA) general framework to the United Kingdom

The practical implementation of Sect. 3.1 is exemplified in panel 1 in Fig. 3. When estimating the impacts of a natural hazard, it is important to ensure that one uses the highest level of (spatial) detail possible for the exposed elements. Within this study, we make use of several openly available datasets to define the location of the exposed economic activities. To populate set \(B\), we use the Middle Layer Super Output Area (MSOA) spatial dataset (Office for National Statistics 2016) to have detailed information on local employment levels for eight different (aggregated) sector groups (Table 2). The MSOA dataset is used for the southeast of England and consists of approximately 2200 MSOAs, with an average size of 13.6 km2. Population is approximately maintained within the definition of an MSOA, resulting in larger sized MSOAs in rural areas, relative to urban areas. The MSOA data are then combined with Corine Land Cover (CLC) dataset (European Environmental Agency 2017) to define the location of industrial activity within each MSOA. The CLC dataset distinguishes 45 different land-use classes, varying from high-density residential areas to several different agricultural land-use classes. The CLC dataset is used to define the spatial location of economic activity, resulting in set \(A\left( B \right)\). Combining these spatial datasets results in a set of economic activities \(S\left( B \right).\)

Given the central role of electrical power in supporting multiple infrastructure types and economic activities (Thacker et al. 2017a), we populate \(I\) as the set of 132 kV electricity distribution substation assets supplying the southeast of the UK. The location of these assets was derived using schematic plans for the area (see Kelly et al. (2016) for more details on the assets). The nonoverlapping set of service areas \(A\left( I \right)\) corresponding to each asset was derived using the Voronoi decomposition technique (Poljanšek et al. 2010; Thacker et al. 2017a). The service area for any asset (given by a Voronoi cell) is derived using the assumption that each asset provides service to the area closest to it in space. This is a valid assumption, as in reality infrastructure assets connected to their nearest demand centers result in (often) spending the least energy (or effort) for delivering goods and services (Pant et al. 2017). We finalize step 1 in the methodology by calculating \(S\left( I \right)\), through the intersection of the previously defined business activity areas \(S\left( B \right)\) and the asset service areas \(A\left( I \right)\).

We calculate system-wide impacts that arise due to the failure of individual assets. For this study, we are specifically interested in the parts of the system that are exposed to flood hazards (Fig. 3, panel 2). As such, we create the sets \(\bar{S}\left( B \right)\) and \(\bar{S}\left( I \right)\), when the datasets of \(S\left( B \right)\) and \(S\left( I \right)\) are spatially overlaid with hazard maps for five different annual return periods (1/20, 1/75, 1/100, 1/200, 1/1000), with flood depth \(y\left( {h_{k} } \right)\) for each element \(\left( {h_{k} } \right)\) within a geographic area (\(a\left( {h_{k} } \right)\)). These hazard maps, generated for the whole of the UK, are produced from a multi-scale two-dimensional dynamic river flood flow model called JFlow (Bradbrook 2006). To infer flooding, we estimate the peak flows along the watercourses that are generated using digital terrain information and catchment descriptors, such as rainfall, soil type, urban coverage, and reservoir influence. Flow points are modeled at regular intervals along the 120,000 km of river network of the UK (spaced at 200 m apart in areas where digital terrain elevation information is considered accurate and 400 m apart elsewhere). Only watercourses with a catchment area greater than 3 km2 in cities and 10 km2 elsewhere are modeled. The flow is then distributed along the watercourse using flow hydrographs. The hydrographs are routed through JFlow, which converts peak flow data into peak flood depth data and estimates the extent of flooding. Finally, banded flood depths (\(y\left( {h_{k} } \right)\)) in meters are produced.

To estimate the economic impacts, we create a set of failure combinations, based on a failure threshold that defines the vulnerability of each infrastructure asset. The critical assets in most electricity substations are elevated above the ground. Many electricity substations in England now have flood protection systems with an elevation of about 1 m. Therefore, we assume that an electricity substation only fails when it is inundated by at least 1 m, that is, \(y\left( {h_{k} } \right)\) > 1.0 m. This assumption results in five impacted electricity substations in our study area for a flood with a return period of 1/1000. Using these five substations, we can derive 31 unique failure combinations, exemplified through the sets \(F\left( B \right)\) and \(F\left( I \right)\). In practical terms, these failure combinations range from failure of one substation up to the failure of all five substations at once. The map in panel 3 of Fig. 3 illustrates the location of these substations and the spatial extent of the affected service areas. Table 3 shows the list of all failure combinations.

These 31 unique failure combinations result in a set of 186 model runs for estimating the macroeconomic impacts. We run one set of combinations for each of the five flood return periods to estimate the impact due to flooding of businesses \(\overline{\overline{S}} \left( B \right)\) within the service areas of these affected substations and a second set of combinations to estimate the impact of substation failure, which results in business interruption for the whole affected service area \(\bar{S}\left( I \right)\). We assume that businesses only disrupt when it is inundated by at least 30 cm, that is, \(y\left( {h_{k} } \right)\) > 0.3 m. In this study, we use temporary reduced employment as the proxy for business disruption. We note that using asset losses is a more commonly used approach to estimate the economic disruption and capacity loss rates (Hallegatte 2008). As described in Sect. 2, however, infrastructure failure will most likely not result in direct damages to buildings and assets of businesses. As such, to consistently compare the impacts to businesses that are just flooded and that are affected by power outages only, we use the loss in labor productivity as the main cause of business disruption. The total output losses can be interpreted as the reduction in value added for each industry in each of the 37 NUTS2 (Nomenclature of Territorial Units for Statistics, level 2)Footnote 1 areas within the UK. To estimate this reduction, we make use of multiregional supply-use tables for the UK for 2013. They are a subset of the regionalized WIOD (World Input–Output Database) for Europe as a whole (Thissen et al. 2017).

5 Results

The following subsections present the results from the application of the methodological framework to the case of flooding within the UK. For the previously introduced 31 failure combinations: Sect. 5.1 presents the direct business disruption and reduced available employment due to flooding and systemic disruption in the southeast of England, and Sect. 5.2 presents the macroeconomic impacts for the whole of the UK.

5.1 Business Disruption

The total flooded area per sector (left panel) and per substation (right panel) appears in Fig. 4. For the two most likely floods (1/20 and 1/75 year frequency), only two substations are flooded (North Watford and Bury St. Edmunds) and within the service area of these substations, almost all flooding occurs in the agricultural areas, close to the river. When the flooding becomes more severe (< 1/100 year frequency), we see a sharp increase in flooded areas that include commercial and noncommercial activities. This can be attributed to the addition of the floods in Canary Wharf and Kingston Upon Thames, both home to many services activities. The substation in Bedford is only included in the 1/1000 year flood, and causes a clear increase in flooded agricultural area due to the relatively more rural nature of this area.

Total flooded area by business sector and substation location in the southeast of England. The left panel presents the total flooded area by sector. The right panel exhibits the total flooded area by location

Figure 5 displays the spatial extent of business disruption in the southeast of England for the five locations identified in Fig. 3, panel 3. The left panel shows the spatial distribution of impacts when the MSOAs are affected by a flood with a 1/1000 return period only, whereas the right panel shows the spatial distribution of a systemic disruption as a result of the same flood. As becomes apparent from the figure, in all the affected MSOAs, the percentage of disrupted businesses increases substantially when electricity fails as well. Because in all five cases, the substation is located in the center of the MSOA clusters, there is a clear pattern in which the most impacted are in the center where the entire MSOA is affected by the power outage/flood. Disruption gradually diminishes to only limited impacts to the MSOAs further away from the substation as a result of a reduced dependency of those MSOAs on the specific substation.

Presentation of the service areas of the five substations in the southeast of England considered in the failure combinations in Table 3. The left panel shows the percentage reduction of total employment for each MSOA due to flooding only by an event with a 1/1000 return period. The right panel shows the percentage reduction of total employment due to a systemic disruption by the same flood event with a 1/1000 return period

To gain a clearer understanding of the impacts, Fig. 6 shows the reduction in employment for scenario 31 (Table 3), the most extreme scenario in which the five substations are all affected. Commercial and public services are seen to be the most affected, in both the flooding only and systemic disruption cases. There is a sharp increase in the total amount of commercial services affected between a 1/75 and a 1/100 flood. As shown in Fig. 4, this is mainly the result of an increase in flood extent around Kingston Upon Thames (location 4) and Canary Wharf (location 5). Both the agricultural and manufacturing sectors are in relative and absolute terms the least affected in terms of temporary reduced employment. This has two main reasons: (1) in all cases, the failed substation is in a relative urbanized area, where we often find less agricultural and manufacturing economic activity; and (2) the agriculture and manufacturing sectors are more capital intensive, as opposed to the more labor intensive commercial and public services.

Projected reduction in employment due to extreme flooding in the southeast of England. Disrupted employment per sector for a flood appears only in absolute terms (upper left panel) and in relative terms (lower left panel) and for a systemic disruption is displayed in absolute terms (upper right panel) and in relative terms (lower right panel)

When comparing the numbers for reduced employment between a flood only (left panel) and a systemic disruption (right panel), Fig. 6 presents a number of interesting insights. First, we see that a systemic disruption can increase losses substantially, especially in the higher return periods. More specifically, the increase in affected employment ranges from a factor 185 for the 1/20 return period, up to a factor 23 for the 1/1000 return period. This smaller difference between a systemic disruption and flood only in the lower return periods can be attributed to the increased flooded area (as also shown in Fig. 4). Second, in the case of a systemic disruption, there is a relatively larger share of the manufacturing sector impacted (especially in the higher return periods), whereas in the case of a flood only, a relatively larger share of the agricultural sector is impacted. Third, the actual overall share of sectors is relatively similar for both a systemic disruption and a flood only scenario. In all cases, the sectors with the largest shares of disrupted employment are the financial and professional activities, public administration, as well as distribution, hotels, and restaurants.

5.2 Macroeconomic Impacts for the UK

Figure 7 shows the ranked daily total output losses for all failure combinations from the smallest (most left bar) to the largest (most right bar) losses. The left panel (1/1000 flood only) and the right panel (systemic disruption) show a similar ranking, but with up to a factor 3 difference in the size of the daily total output losses. The similar ranking indicates that even though the spatial extent of impacted businesses clearly increases due to substation failure, the relative composition of affected sectors remains similar. When focusing on the daily direct output losses (the dotted part of the bars) the difference between a systemic disruption and a flood can be seen to go up to a factor 33 difference, which is similar to the difference in the disrupted employment between a systemic disruption and flood only (Fig. 5).

Total daily output losses for the United Kingdom for 31 failure combinations. The left panel shows the impacts due to a flood with a return period of 1/1000. The right panel shows the impacts due to a flood with a return period of 1/1000 and a failure of the electricity substation at the same time. Please refer to the list in Fig. 6 for a definition of the sectors

This large difference between direct and total output losses highlights the observation that a relatively small disruption in the local economy can result in relatively large macroeconomic impacts. The average share of the direct output losses in the total output losses is 17% in the case of a flood only (an average disaster multiplier (that is, the division of the direct output losses by the indirect output losses) of 6.3) and 60% in the case of a systemic disruption (an average disaster multiplier of 1.6). This indicates that a large share of businesses directly disrupted due to a systemic disruption are already disrupted indirectly in the case of a flood event only.

Two single failure scenarios s2 and s3, respectively Kingston upon Thames and Canary Wharf, result in substantially higher output losses compared to the other three single failure scenarios. The impacts in these areas are mainly driven by a large temporary reduced employment capacity in the service sectors (as also shown by the large increase in disrupted employment for these sectors in Fig. 5 when these locations are included). For both of these scenarios and in both loss estimation approaches, the daily impacts for the financial and professional activities (sector F) are relatively higher compared to the other single failure scenarios.

Interestingly, the results show that in most scenarios the public services (sector G) result in the highest daily total output losses. This is in contrast to Fig. 5, which shows similar disrupted employment numbers for distribution, hotels, and restaurants (sector D) and an even higher disrupted employment for professional activities (sector F). This indicates that substitution of services in the affected areas is more difficult in the public sector relative to the commercial sector. Distribution activities even show gains as a result of a disruption. The larger the disruption, the more gains we see for this sector. This is a direct result of the increase in trade of services and goods due to substitution of supply and demand from and towards other regions.

Figure 8 shows the daily total output losses for the whole of the UK. The larger the disruption, the less likely it is for other regions to be able to offset the negative effects of the disruption. In the two left panels, which illustrates the (small) economic impacts of scenario 4 (disruption in Bury St. Edmunds), we see that most regions either do not really endure any impacts at all when the disruption is small (upper left panel), or are able to offset some of the negative effects because of this disruption (lower left panel). These small positive effects are mainly driven by substitution effects in commercial activities. The two right panels, showing the effects of the most extreme scenario, still show relative localized daily total output losses. This indicates that for the five substations considered in this study, most of the UK is able to find a substitution for the lost services.

Daily impacts for four scenarios in each NUTS2 (Nomenclature of Territorial Units for Statistics, level 2) region of the United Kingdom. The upper left and upper right panels show the impacts due to a 1/1000 flood for scenarios 4 and 31, respectively. The lower left and lower right panels show the total impact due to infrastructure failure and a 1/1000 flood for scenarios 4 and 31, respectively

6 Discussion

This is one of the first studies that quantifies how disaster impacts may change when incorporating critical infrastructure failures in the disaster loss modeling framework. The results highlight how up to a factor 3 increase in daily total output losses can be observed when critical infrastructure failure is considered. In terms of business disruption at a local level, it can even result in up to a factor 185 increase in reduced employment. This considerable increase in economic impacts shows the importance of including critical infrastructure failure in a more quantitative manner into disaster risk modeling frameworks and, consequently, into disaster risk management. A more holistic loss modeling approach is the first step towards improving the determination of the cost-effectiveness of risk reduction measures, as called for in the United Kingdom Climate Change Risk Assessment (Dawson et al. 2017) and the most recent international agreements: the Sendai Framework for Disaster Risk Reduction 2015–2030 (UNISDR 2015) and the Warsaw International Mechanism for Loss and Damage Associated with Climate Change Impacts (UNFCCC 2013).

While there are no data to validate our estimates with real-world numbers for flooding in the southeast of England, documented evidence of a flood event in the Lancaster District of the Lancashire County in 2015 (Kemp 2016) provides a good understanding of electricity impacts. During a 1/100 year flood event, a 132 kV substation failure affected 61,000 properties whose power was progressively restored over 2 days, an outage that impacted over 100,000 people (Kemp 2016). The reported number of properties directly flooded was 332 (Lancashire County Council 2016), which shows that due to the electricity outage over the 2 days approximately 183 times more properties were affected. The total reported number of properties directly flooded during the period of flooding in 2015 over an extended Lancashire area was 2567 (2029 residential and 538 business), showing that the electricity outage magnified the impacts by about 24 times. The UK Environment Agency calculates that, for every person who suffers flooding, about 16 more are affected by loss of services such as power, transport, and telecommunications (Environment Agency 2019).

If properties affected could be considered as a proxy for affected labor, then these estimates from reported statistics of the magnification of impacts due to electricity failure are close to our modeled estimates. The estimated economic costs of disruption for this substation failure included damages from loss of power estimated at £10 million for 2 days, based on £70 per day compensations to customers (Environment Agency 2018). These costs based on compensations to customers are of the same order as our estimated economic losses. The customer damage costs reported in the Environment Agency report, applied to the 350,000–800,000 disrupted employment estimated by us (Fig. 6) for the largest set of five substations failures is approximately £24.5–56 million per day (Environment Agency 2018). From our analysis, the total economic loss for the five substation failure is estimated to be around £27 million per day, falling within the range of these estimates and probably on the lower end. Not including household customers in estimating direct impacts may lead to high indirect impacts. To estimate the factor of increase in losses due to indirect impacts of infrastructure disruptions, the UK Environment Agency has traditionally used an uplift factor of around 2 in its Long Term Investment Scenarios (Environment Agency 2014) while some studies in the Thames Catchment have used a factor of 1.89 (Raynor 2014). This means that the total losses are considered to be 1.89–2 times greater than direct losses, when accounting for infrastructure disruptions. Our estimate of 3 in this study is higher because most of the existing estimates do not account for the macroeconomic impacts, and are generally underestimating indirect impacts.

An inherent problem within such macroeconomic modeling approaches is the assumptions modelers are required to make and the resulting uncertainty contained within these assumptions. Koks and Thissen (2016) tested the two core assumptions that drive the MRIA model results: (1) the maximum use of regional capacity, which influences when and by how much products will be imported from other regions; and (2) the recovery duration. The results show that setting a relatively low maximum local production will cause substantially larger imports from other regions, whereas allowing for a high maximum local production creates a large (unwanted) overproduction. Because these goods may not get sold due to a reduction in demand, the result is additional (unwanted) costs. Doubling recovery time may result in almost three times higher losses (Koks and Thissen 2016). As recovery time is often unknown and is proven to be a major driver of the total losses, we have chosen to present the results in this study in terms of daily output losses.

This study interfaces both economic disaster impact and critical infrastructure risk research and aims to bring together elements from both fields. In relation to the infrastructure literature, the outcomes of this study show that disrupted employment, as a result of lost services, may provide an alternative measure of impacts compared to the traditionally used output losses. In relation to the economic literature, we have presented a methodology that more explicitly incorporates supply-side disruptions, when compared to the majority of current input–output approaches. As outlined by Dietzenbacher and Miller (2015) and Oosterhaven (2017), the traditional input–output model and, consequently, the inoperability input–output model (IIM) are only able to deal with demand-side disruptions. Disaster and critical infrastructure failure, however, will result in supply-side disruptions as well (that is, firms not able to produce), calling for more flexible approaches such as the one presented in this study. In the case of a systemic disruption, the disaster multipliers observed in this study (averaging 1.6) are similar to studies using a similar macroeconomic modeling approach (Oosterhaven and Tobben 2017) but are slightly lower in comparison to studies using the IIM approach. Anderson et al. (2007), for instance, presented a disaster multiplier of approximately 2.2 for the 2003 blackout in the northwest of the United States. In the case of a flood event only, however, the average observed disaster multiplier of 6.3 seems to be much higher compared to previous studies. This may indicate that the relatively small flood events considered in this study do affect relatively important economic activities.

In the determination of the effectiveness of risk reduction measures, there is an increasing trend of including nonmonetary aspects [for example, social vulnerability (Koks et al. 2015)]. The monetary aspects (that is, the cost-benefit analysis) still play a leading role, however, in deciding whether a risk reduction measure is or is not employed. Including critical infrastructure failure in the loss modeling framework may not only result in making a dike (more) cost-effective (the benefits of avoided losses may increase), but may also increase the awareness of policymakers and network operators to improve resilience and redundancy of critical infrastructure networks. This knowledge gain makes management and infrastructure better able to cope with disasters. Evaluation of losses from systemic failures may result in changes to the overall prioritization of risk reduction measures—leading to a more optimal sequencing of adaptation option deployment.

The limited availability of data on the structure and function of infrastructure systems and the businesses that they support, in normal conditions and at various stages of a disaster event, introduces uncertainties into the analysis and inherently into the conclusions that are drawn from available data. For example, lack of data on the operational characteristics of the electricity grid has resulted in modeling assumptions that include: that businesses have no electricity back-up supplies on premises, and that the failure of a substation will result in full restriction of downstream power to the businesses it usually supplies. Such assumptions, though justified through empirical observations, may not be observed entirely in reality and hence the results emerging from this study could be considered as a “worst case” scenario.

Given these considerations, this study reflects an indicative analysis that provides a first step towards identifying and screening large scale systemic vulnerabilities. More detailed, site-specific analyses of assets should be undertaken to estimate their exposure and vulnerabilities to flooding or other natural hazards. Despite this, the work presented within this study forms an important justification for, and methods towards, a systemic approach to evaluating the potential economic losses associated with natural hazard events. This achievement will form an important means by which to generate evidence to support ongoing policy efforts to optimally reduce risks to natural hazards (Environment Agency 2014), including the prioritized adaptation of critical infrastructures (Energy Networks Association 2018) for electricity substation adaptation to flooding in the UK. In addition to progress in these more traditional policy areas, insights into social-economic related impacts, including impacts to employment and regional economic effects, will provide policymakers with greater information on which to base investment decisions and to offer a more progressive and holistic approach to disaster management and planning.

7 Conclusions

In this article, we presented a spatially explicit integration of critical infrastructure asset failure modeling and business activity disruption in order to comprehensively estimate the total economic losses of flooding at a multiregional level. This study presents two key novelties in the methodological development of disaster impact modeling: (1) the spatial integration of critical infrastructure assets and business activity, resulting in a more detailed estimation of business disruption due to natural hazards; and (2) the explicit coupling of critical infrastructure failure with a state-of-the-art multiregional macroeconomic modeling framework, able to capture supply-side, as well as demand-side, disruptions.

By presenting both the economic impacts due to flooding and due to flooding and critical infrastructure failure concurrently, we have demonstrated the necessity of incorporating critical infrastructure failure in disaster impact modeling. In terms of business disruption at a local level, the results show up to a factor 23 for the 1/1000 return period of reduced employment when incorporating critical infrastructure failure in the loss assessment. When looking at the macroeconomic impacts at a national level, the results show that daily direct output losses could increase up to a factor 33 and total output losses up to a factor 3, when including critical infrastructure failure in the loss assessment.

Through the proposed study we have demonstrated the large benefits that exist in adopting a systemic approach to disaster impact modeling. Given the complex and interconnected nature of both economic and infrastructure systems, these benefits exist for multiple users and organizations, beyond areas immediately impacted by the disaster event. To exploit these benefits, a coordinated and cooperative approach will be required by researchers and other stakeholders from government and industry. Such partnerships can lead to not only the further development and refinement of disaster-impact models, but also result in the parametrization of those models with the best available data, ensuring that they are fit-for-purpose use by decision makers. Such an approach will ensure that risk reduction and resilience building activities are underpinned by the most appropriate evidence and are given the best possible opportunities for success.

Notes

The NUTS classification is a hierarchical system for dividing up the economic territory of the European Union for the purpose of the collection and development of European-wide statistics. NUTS2 regions are generally used for applications and analysis for regional policy making. Examples of NUTS2 regions are the inner-city of London and the city of Brussels.

References

Anderson, C.W., J.R. Santos, and Y.Y. Haimes. 2007. A risk-based input–output methodology for measuring the effects of the August 2003 northeast blackout. Economic Systems Research 19(2): 183–204.

AON (Application-Oriented Networking). 2016. 2014 Annual global climate and catastrophe report. London: AON Benfield.

Aven, T. 2011. On some recent definitions and analysis frameworks for risk, vulnerability, and resilience. Risk Analysis 31(4): 515–522.

Bompard, E., T. Huang, Y. Wu, and M. Cremenescu. 2013. Classification and trend analysis of threats origins to the security of power systems. International Journal of Electrical Power & Energy Systems 50(1): 50–64.

Bradbrook, K. 2006. JFLOW: A multiscale two-dimensional dynamic flood model. Water and Environment Journal 20(2): 79–86.

Bubeck, P., W.J.W. Botzen, and J.C.J.H. Aerts. 2012. A review of risk perceptions and other factors that influence flood mitigation behavior. Risk Analysis 32(9): 1481–1495.

Dawson, R.J., D. Thompson, D. Johns, et al. 2017. UK climate change risk assessment evidence report. London: The Committee on Climate Change. https://www.theccc.org.uk/tackling-climate-change/preparing-for-climate-change/uk-climate-change-risk-assessment-2017/. Accessed 12 Sept 2019.

Dietzenbacher, E., and R.E. Miller. 2015. Reflections on the inoperability input–output model. Journal of Economic Systems Research 27(4): 478–486.

Energy Networks Association. 2018. ETR [Engineering Technology Report] 138: Resilience to flooding of grid and primary substations. London: Energy Networks Association.

Environment Agency. 2014. Flood and coastal erosion risk management: Long-Term Investment Scenarios (LTIS) 2014. Bristol, UK: Environment Agency.

Environment Agency. 2018. Estimating the economic costs of the 2015 to 2016 winter floods. Bristol, UK: Environment Agency.

Environment Agency. 2019. Flood and coastal erosion risk management: Long-term investment scenarios (LTIS) 2019. https://www.gov.uk/government/publications/flood-and-coastal-risk-management-in-england-long-term-investment/long-term-investment-scenarios-ltis-2019. Accessed 12 Sept 2019.

European Environmental Agency. 2017. CLC Corine land cover data 2012 version 18. https://land.copernicus.eu/pan-european/corine-landcover/clc-2012/view. Accessed 12 Sept 2019.

Gerl, T., H. Kreibich, G. Franco, D. Marechal, and K. Schröter. 2016. A review of flood loss models as basis for harmonization and benchmarking. PLoS One 11(7): Article e0159791.

Haer, T., W.J. Botzen, H. de Moel, and J.C.J.H. Aerts. 2016. Integrating household risk mitigation behavior in flood risk analysis: An agent-based model approach. Risk Analysis 37(10): 1977–1992.

Haimes, Y.Y., B.M. Horowitz, J.H. Lambert, J.R. Santos, C.Y. Lian, and K.G. Crowther. 2005. Inoperability input-output model for interdependent infrastructure sectors. I: Theory and methodology. Journal of Infrastructure Systems 11(2): 67–79.

Haimes, Y.Y., and P. Jiang. 2001. Leontief-based model of risk in complex interconnected infrastructures. Journal of Infrastructure Systems 7(1): 1–12.

Hall, J.W., S. Thacker, M.C. Ives, Y. Cao, M. Chaudry, S.P. Blainey, and E.J. Oughton. 2017. Strategic analysis of the future of national infrastructure. Proceedings of the Institution of Civil Engineers—Civil Engineering 170(1): 39–47.

Hallegatte, S. 2008. An adaptive regional input-output model and its application to the assessment of the economic cost of Katrina. Risk Analysis 28(3): 779–799.

Hines, P., J. Apt, and S. Talukdar. 2009. Large blackouts in North America: Historical trends and policy implications. Energy Policy 37(12): 5249–5259.

Hu, X., J.W. Hall, P. Shi, and W.H. Lim. 2016. The spatial exposure of the Chinese infrastructure system to flooding and drought hazards. Natural Hazards 80(2): 1083–1118.

Jonkeren, O., and G. Giannopoulos. 2014. Analysing critical infrastructure failure with a resilience inoperability input–output model. Journal of Economic System Research 26(1): 39–59.

Kelly, S., P. Tyler, and D. Crawford-Brown. 2016. Exploring vulnerability and interdependency of UK infrastructure using key-linkages analysis. Networks and Spatial Economics 16(3): 865–892.

Kemp, R. 2016. Living without electricity: One city’s experience of coping with loss of power. London: Royal Academy of Engineering. https://www.raeng.org.uk/publications/reports/living-without-electricity. Accessed 30 Aug 2019.

Koks, E.E., B. Jongman, T.G. Husby, and W.J.W. Botzen. 2015. Combining hazard, exposure and social vulnerability to provide lessons for flood risk management. Environmental Science & Policy 47: 42–52.

Koks, E.E., and M. Thissen. 2016. A multiregional impact assessment model for disaster analysis. Journal of Economic System Research 28(4): 429–449.

Kwasinski, A. 2013. Lessons from field damage assessments about communication networks power supply and infrastructure performance during natural disasters with a focus on Hurricane Sandy. In Proceedings of FCC Workshop on Network Resiliency 2013, 5 February 2013, New York, USA.

Lancashire County Council. 2016. December 2015 floods in Lancashire flood & water management Act 2010 Section 19 investigation—Appendix A. https://www.lancashire.gov.uk/media/900010/section-19-flood-investigation-report-december-2015-floods.pdf. Accessed 12 Sept 2019.

Leontief, W.W. 1951. Input–output economics. Scientific American 185(4): 15–21.

MacKenzie, C.A., K. Barker, and F.H. Grant. 2012. Evaluating the consequences of an inland waterway port closure with a dynamic multiregional interdependence model. IEEE Transactions on Systems Man and Cybernetics Part A—Systems and Humans 42(2): 359–370.

Meyer, V., N. Becker, V. Markantonis, R. Schwarze1, J.C.J.M. van den Bergh, L.M. Bouwer, P. Bubeck, P. Ciavola, et al. 2013. Assessing the costs of natural hazards—State of the art and knowledge gaps. Natural Hazards and Earth System Sciences 13: 1351–1373.

Nedic, D.P., I. Dobson, D.S. Kirschen, B.A.Carrerasc, and V.E. Lynchc. 2006. Criticality in a cascading failure blackout model. International Journal of Electrical Power & Energy Systems 28(9): 627–633.

Office for National Statistics. 2016. Middle layer super output areas (December 2011) full clipped boundaries in England and Wales. UK: Office for National Statistics.

Okuyama, Y. 2015. How shaky was the regional economy after the 1995 Kobe earthquake? A multiplicative decomposition analysis of disaster impact. The Annals of Regional Science 55(2): 289–312.

Okuyama, Y., and J.R. Santos. 2014. Disaster impact and input–output analysis. Journal of Economic Systems Research 26(1): 1–12.

Oosterhaven, J. 2017. On the limited usability of the inoperability IO model. Journal of Economic Systems Research 29(3): 452–461.

Oosterhaven, J., and M.C. Bouwmeester. 2016. A new approach to modeling the impact of disruptive events. Journal of Regional Science 56(4): 583–595.

Oosterhaven, J., and J. Tobben. 2017. Wider economic impacts of heavy flooding in Germany: A non-linear programming approach. Spatial Economic Analysis 12(4): 404–428.

Ouyang, M. 2014. Review on modeling and simulation of interdependent critical infrastructure systems. Reliability Engineering & System Safety 121: 43–60.

Ouyang, M., L. Dueñas-Osorio, and X. Min. 2012. A three-stage resilience analysis framework for urban infrastructure systems. Structural Safety 36–37: 23–31.

Pant, R., K. Barker, F.H. Grant, and T.L. Landers. 2011. Interdependent impacts of inoperability at multi-modal transportation container terminals. Transporation Research Part E-Logistics and Transportation Review 47(5): 722–737.

Pant, R., K. Barker, and T.L. Landers. 2015. Dynamic impacts of commodity flow disruptions in inland waterway networks. Computers & Industrial Engineering 89: 137–149.

Pant, R., J.W. Hall, and S.P. Blainey. 2016. Vulnerability assessment framework for interdependent critical infrastructures: Case-study for Great Britain’s rail network. European Journal of Transport and Infrastructure Research 16(1): 174–194.

Pant, R., S. Thacker, J.W. Hall, D. Alderson, and S. Barr. 2017. Critical infrastructure impact assessment due to flood exposure. Journal of Flood Risk Management 11(1): 22–33.

Pitt, M. 2008. The Pitt review: Learning lessons from the 2007 floods. London: Pitt Review. http://www.cabinetoffice.gov.uk/thepittreview/final_report.aspx. Accessed 29 Aug 2019.

Poljanšek, K., F. Bono, and E. Gutiérrez. 2010. GIS-based method to assess seismic vulnerability of interconnected infrastructure: A case of EU gas and electricity networks. Luxembourg: Publications Office of the European Union.

Poljanšek, K., M. Marin Ferrer, T. De Groeve, and I. Clark. 2017. Science for disaster risk management 2017: Knowing better and losing less. Luxembourg: Publications Office of the European Union.

Raynor, P. 2014. The Humber estuary flood risk management strategy: Summary strategy and business case. 2014. https://www.eastriding.gov.uk/EasySiteWeb/GatewayLink.aspx?alId=592095. Accessed 12 Sept 2019.

Rinaldi, S.M., J.P. Peerenboom, and T.K. Kelly. 2001. Identifying, understanding, and analyzing critical infrastructure interdependencies. IEEE Control Systems Magazine 21(6): 11–25.

Rose, A., I. Sue Wing, D. Wei, and A. Wein. 2016. Economic impacts of a California Tsunami. Natural Hazards Review 17(2): Article 4016002.

Scawthorn, C., P. Flores, N. Blais, H. Seligson, E. Tate, S. Chang, E. Mifflin, W. Thomas, et al. 2006. HAZUS-MH flood loss estimation methodology. II. Damage and loss assessment. Natural Hazards Review 7(2): 72–81.

Schulte in den Bäumen, H., J. Többen, and M. Lenzen. 2015. Labour forced impacts and production losses due to the 2013 flood in Germany. Journal of Hydrology 527: 142–150.

Thacker, S., S. Barr, R. Pant, J.W. Hall, and D. Alderson. 2017a. Geographic hotspots of critical national infrastructure. Risk Analysis 37(12): 2490–2505.

Thacker, S., S. Kelly, R. Pant, and J.W. Hall. 2017b. Evaluating the Benefits of Adaptation of Critical Infrastructures to Hydrometeorological Risks. Risk Analysis 38(1): 134–150.

Thacker, S., R. Pant, and J.W. Hall. 2017c. System-of-systems formulation and disruption analysis for multi-scale critical national infrastructures. Reliability Engineering & System Safety 167: 30–41.

Thissen, M., B. Los, and M. Lankhuizen. 2017. Construction of a time series of fine-grained detailed Nuts2 regional input-output tables for the EU embedded in a global system of country tables. Hague, Netherlands: PBL Netherlands Environment Assessment Agency.

UNFCCC (United Nations Framework Convention on Climate Change). 2013. Warsaw international mechanism for loss and damage associated with climage change impacts. Bonn: UNFCCC.

UNISDR (United Nations International Strategy for Disaster Reduction). 2015. Sendai framework for disaster risk reduction 2015–2030. Geneva: UNISDR.

Winkler, J., L. Duenas-Osorio, R. Stein, and D. Subramanian. 2010. Performance assessment of topologically diverse power systems subjected to hurricane events. Reliability Engineering & System Safety 95(4): 323–336.

Yusta, J.M., G.J. Correa, and R. Lacal-Arántegui. 2011. Methodologies and applications for critical infrastructure protection: State-of-the-art. Energy Policy 39(10): 6100–6119.

Zio, E. 2009. Reliability engineering: Old problems and new challenges. Reliability Engineering & System Safety 94(2): 125–141.

Acknowledgements

We would like to thank the PBL Netherlands Environmental Assessment Agency, and in particular Dr. Mark Thissen, for providing the multiregional supply-use tables. The research reported in this article was part of the U.K. Infrastructure Transitions Research Consortium (ITRC) funded by the Engineering and Physical Sciences Research Council under Programme Grants EP/I01344X/1and EP/N017064/1.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

Koks, E., Pant, R., Thacker, S. et al. Understanding Business Disruption and Economic Losses Due to Electricity Failures and Flooding. Int J Disaster Risk Sci 10, 421–438 (2019). https://doi.org/10.1007/s13753-019-00236-y

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13753-019-00236-y