Abstract

We tested the causality between FDI and its determinants in Bangladesh in the presence of structural break harnessing Vector Autoregression (VAR) model and Granger causality test. Regressors such as GDP growth rate, inflation, interest, corporate tax, exchange and wage rate, and trade openness (TO) have been used. VAR model finds that interest, tax, wage, and exchange rate do not affect inward FDI. However, the inflation rate and TO significantly impact the inward FDI in Bangladesh. The Granger causality test reveals a bidirectional causality in the FDI–inflation and FDI–TO nexus, whereas other explanatory variables do not cause the FDI granger. Variance decomposition (VDC) and impulse response function (IRF) assessment approve strong, moderate, and poor or no explanatory power of TO, inflation, and other explanatory variables, respectively. Regarding FDI–inflation bidirectional causality, we observed both natural (inflation truly causes FDI) and fake causality (FDI does not necessarily cause inflation). Therefore, when inflation causes FDI, then Bangladeshi Taka (BDT) becomes strong against USD, which increases import and reduces export (import > export). Due to the negative trade balance, this is true for Bangladesh. However, if FDI causes inflation, it will depreciate BDT; consequently, the export will surpass the total import, which is not the case in Bangladesh. Therefore, inflation causes FDI in Bangladesh, and this punch line ends the ongoing debate in the FDI–inflation–exchange rate nexus in Bangladesh. Finally, we recommend decreasing the lending interest rates to encourage further investment, adopting tax holidays, developing a skilled and semi-skilled workforce to harness the advantage of lower wage rates, and being more open to facilitating FDI-led development.

Similar content being viewed by others

Introduction

For many capital-poor nations, accumulating the desired amount of capital is not facile, and more often, these nations fall into long-term debt traps and predatory lending (Behuria 2018; Brautigam 2020). Moreover, apart from external funding (i.e., debt or foreign aid), a nation can also garner required capital from internal sources and portfolio investments. However, there is another type of capital, different from foreign debt or aid, known as foreign direct investment (FDI). FDI establishes a symbiotic relationship between the donor and the host countries where both benefit from capital transfer, Research and Development (R&D), technology and knowledge transfer, cheap labor, and institutional development (Arel-Bundock 2017; Hu et al. 2021; Liu et al. 2016; Ning and Wang 2018; Temiz and Gökmen 2014). While investing, the Multinational Companies (MNCs) primarily focus on the economic globalization, location determinants, infrastructural development, political environment, effective cross-border trade regulations, and institutional factors of the host economies (Alam et al. 2019; Contractor et al. 2020; Deseatnicov and Akiba 2016; Kleineick et al. 2020; Paul and Jadhav 2019). Apart from the said factors, some other country-specific determinants of FDI are deemed very influential. For instance, corruption, soundness of law and order, and democratic accountability have been identified as determinants of inward FDI for many developing nations (Osabutey and Okoro 2015). Other less assessed factors such as financial deepening (Liu et al. 2020) and soundness of the intellectual property rights in trade (Contractor et al. 2021; Zhang and Yang 2016) are also significant inward FDI parameters.

FDI’s inflow is also influenced by the social, political and institutional characteristics of a country. Studies within the socio-political and political-institutional genres have identified that political soundness, effective governing, proper regulations, voice and accountability, active start-up regulations, economic freedom, ease of doing business, government spending, improved one-stop services dedicated for international trade are the major determinants of FDI among world’s emerging economies (Alam et al. 2019; Contractor et al. 2021; Ibrahim et al. 2020; Kurtović et al. 2020; Mourao 2018; Paul and Jadhav 2019; Rashid et al. 2017). Numerous other studies have assessed determinants such as inflation, exchange, interest, and GDP growth rate, per capita GDP, export, import, gross national income and, external debt (Asiamah et al. 2019; Gupta 2018; Hossain 2021; Ibrahim and Abdel-Gadir 2015; Jaiblai and Shenai 2019; Kishor and Singh 2015; Sabir et al. 2019; Yimer 2017). In addition, some studies have analyzed the impact of foreign reserve on inward FDI, where Gupta (2018) found a positive connection between foreign reserves and FDI inflow in India, and Hossain (2021) found no impact of reserve on inward FDI in Bangladesh. Other determinants such as human resources, foreign and domestic agglomeration, industrial production index, stock market capital, stock exchange turnover ratio, currency value appreciation, globalization index, value of private consumption expenditure, current account balance, agricultural value addition have also been discussed in the FDI literature (Vi Dũng et al. 2018; Hossain 2021; Kishor and Singh 2015; Sabir et al. 2019; Sharma and Kautish 2020). Besides, resource-rich nations have particular appeal in resource-based FDI (Alfalih and Hadj 2020; Chanegriha et al. 2017; Rjoub et al. 2017; Yimer 2017).

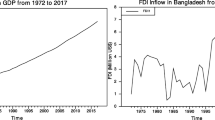

Bangladesh, a South Asian nation, has obtained jaw-dropping progress in infrastructural development and GDP growth. Consequently, the nation’s appetite for FDI has grown significantly in the recent years. According to Asian Development Bank (ADB), in the fiscal year of 2019, Bangladesh witnessed a record 8.2% growth, highest in South Asia (ADB 2021). Bangladesh’s GDP growth rate has been depicted in Fig. 1 (ADB 2020). Growth rate is an important determinant of FDI, and most studies have observed a positive association between GDP growth and FDI (Hossain 2021; Jaiblai and Shenai 2019; Kurtović et al. 2020; Saleem et al. 2020). However, given the surge of inward FDI in Bangladesh, the causality between GDP and FDI is yet to discover.

Annual GDP growth rate of Bangladesh from 2018 to 2021. Source: Compilation by the authors harnessing data from Asian Development Outlook (ADO) of ADB (2020)

Apart from growth rate, this paper considers variables such as inflation rate, interest rate, corporate tax, wage rate, and two other variables with international linkages, exchange rate, and trade openness. Inflation and interest rates are important determinants of inward FDI. However, the effects of these two variables have not been tested frequently on FDI. There are only a handful of studies on the effect of inflation on FDI, and all of them found negative connections (Agudze and Ibhagui 2021; Ibrahim and Abdel-Gadir 2015; Sabir et al. 2019). In Bangladesh, there is no concrete study on the causal effect of inflation on FDI. Hence, we have added inflation in our model to accommodate the causality between FDI and inflation, which will help design better macroeconomic policies for the country. Moreover, it has been proved that the corporate tax reduction and provision of tax holidays positively affect MNC’s investment decisions (Du et al. 2014). However, Bangladesh’s stand-in corporate taxation is quite the opposite of its Asian counterparts. According to a Bangladesh Investment Development Authority (BIDA 2022), the corporate tax rate for foreign investors in Bangladesh is 40–45%, whereas, in the case of Vietnam, Malaysia, and Indonesia, it is only 20, 24, and 25%, respectively. The high tax rate discourages potential investments; therefore, we have incorporated corporate tax in our model to assist with the modifications of government fiscal policies in Bangladesh.

Besides, currency devaluation brings more FDI to the host nation (Mostafa 2020; Xing 2006). Bangladeshi Taka (BDT) is strong against the USD, and it’s been a while since the government last devaluated the BDT. Therefore, we have explored the effect of the exchange rate on capital flow in Bangladesh. In addition, we have brought the empirical spotlight on the FDI–exchange rate–inflation nexus in Bangladesh to unveil the existing policy gap in Bangladesh’s capital market. Furthermore, MNCs invest to those nations that offer lower wages, which significantly reduces the firm-level production cost. Besides, it is already established that FDI can influence the wage level of the local skilled labors in the host nations (Hou et al. 2021; Tomohara and Takii 2011). Labor cost is comparatively very low in Bangladesh; however, the FDI–wage causal nexus is still unknown and it is judicious to trace the relation whether wage rate influences the FDI inflow or it is the other way around in Bangladesh. The wage rate depends on the skills of the labors (i.e., high-skilled labors are paid handsomely than other manual labors). Therefore, it is also important to assess the effects of the variation in skills on the FDI inflow in Bangladesh. Furthermore, Bangladesh has been advocating trade liberalization since the 1990s and has been successful in the improvement of global and bilateral trade relations across the Indian sub-continent, the European Union, and North America. This paper has given exclusive consideration for measuring the effect of trade openness on inward FDI in Bangladesh.

The FDI literature is teeming with numerous research outcomes; however, there still exists mixed and, to some extent, misleading and inconclusive outcomes that can downplay the importance of FDI. The inconclusive outcomes may be due to the adoption of different methodologies that may create issues with smaller datasets. Moreover, some studies put less importance on the time-series properties of the datasets, which may render spurious regression and can influence the ultimate outcomes (Oladipo 2013). Furthermore, the direction of causality between FDI and its regressors remains the most inconclusive in FDI literature. This paper is expected to explore the above-mentioned issues to contribute empirically to the FDI literature.

By addressing the above issues this paper is believed to make three significant contributions to the FDI literature of Bangladesh and alike nations. The first contribution will be methodological. In our paper, we have harnessed a large time-series dataset spanning from 1975 to 2015 and employed a wide array of econometric methodologies. We harnessed the VAR model followed by the Granger causality test (Granger 1969). We furthered our analysis by applying the impulse response function (IRF), variance decomposition (VDC), and vector error correction model (VECM) to comment on the long-run coefficients and shock level between FDI and its regressors. Second, this is one of the first studies that has considered the structural break while dealing with the determinants of FDI in Bangladesh. We have harnessed the Zivot and Andrews (2002) test to check the dataset's structural break.

Third, this paper introduces some rarely tested macroeconomic parameters (i.e., inflation, corporate tax, interest rate, and TO) of inward FDI in the context of Bangladesh. The inclusion of these regressors will help in formulating and adopting appropriate short and long-run regional and international policies to bait more FDI in the future. Regarding the parameters, we have asked three questions. (1) Does inward FDI cause inflation in Bangladesh or inflation cause FDI? This question is interesting because if FDI causes inflation in Bangladesh then ultimately the total volume of FDI will get dwindled in Bangladesh to control the economy’s inflationary pressure. Moreover, high inflation makes the business expensive for the MNCs, and they will look for other potential hosts. (2) What is happening in the FDI–exchange rate–inflation nexus in Bangladesh? Bangladesh has been pioneering the exchange rate appreciation policy, which makes import cheaper in Bangladesh. Moreover, Hossain (2021) observed that FDI and export are substitutionary in Bangladesh, and if this is the case, then exchange rate appreciation will undoubtedly help Bangladesh’s FDI-led development. (3) Do interest, corporate tax, and wage rate, and TO affect the FDI significantly in Bangladesh? If not, what policies can be adopted to fix the inactivity of these variables? What kind of causality is running between TO and inward FDI in Bangladesh?

The remaining paper is structured as follows: “Trends in inward FDI in Bangladesh” section discusses the history of FDI inflow in Bangladesh, “Theoretical and empirical literature review” section delineates the existing literature and their limitations, “Methodology” section features the statistical techniques that this paper has used, “Results and discussion” section elaborates the obtained outcomes with scientific logic, and “Conclusion and policy recommendation” section wraps this empirical endeavor with some suggestions for policy modifications.

Trends in inward FDI in Bangladesh

It is impossible for capital-poor nations like Bangladesh to implement mega projects that require billions of dollars only from internal funding. However, Bangladesh has created an example in daring to initiate one of the most expensive projects in its history, known as the “Padma Multipurpose Bridge” project. According to The Business Standard (2020), an estimated USD 3.6 billion will be required to accomplish this dream project. However, currently, several other mega projects (i.e., Matarbari Power Plant, Metro Rail Project, Rooppur Nuclear Power Plant, Karnaphuli Underwater Tunnel, Payra Deep Sea Port and so on) are ongoing in Bangladesh relying on external funding. The punch line here is that foreign investment is the key to Bangladesh’s ultimate development, and without it, the nation will perform poorly in the long run.

Bangladesh has achieved remarkable eye-catching improvements in various socio-economic indicators. Consequently, in the fiscal year of 2018–2019, Bangladesh received a record USD 3.88 billion FDI from foreign MNCs, whereas she gained USD 2.58 billion in 2017–2018 (Bangladesh Bank 2019, 2018). However, due to the Covid-19 pandemic, Bangladesh, including other nations, have witnessed a slump in the FDI inflow. According to United Nations Economic and Social Commission for the Asia and Pacific (ESCAP) (ESCAP 2020), the international flow of FDI has dropped by 49% (a fall from USD 1.5 trillion to USD 859 billion) in the first half of 2020. Following the trend, Bangladesh has also observed a downfall in the inflow of FDI, and according to a report of Dhaka Tribune (2020), Bangladesh has experienced a 32% fall in the inflow of FDI in the first half of 2020.

According to the Bangladesh Bank data, in the fiscal year of 2019–2020, the manufacturing sector received the highest FDI in Bangladesh, totalling an amount of USD 688.77 million (of which USD 271.17 million, USD 157.14 million and USD 142.48 million went to textiles and wearing, food products and other manufacturing industries, respectively), then the power sector received the second-highest amount of FDI totalling an amount of USD 632.15 million (of which power sector received USD 520.47 million and gas and petroleum received USD 111.68 million). The third, fourth, and fifth-highest positions were obtained by trade and commerce, transport, storage and communication and construction, totalling USD 447.40, USD 277.86 and USD 144.59 million, respectively (Bangladesh Bank 2020). The values are also graphically represented in Fig. 2.

Net FDI inflows by major sectors during the fiscal year of 2020. Source: Compilation by the authors exploiting Bangladesh Bank (2020) data

Moreover, before the Covid-19 pandemic, South Asia observed a surge in the inflow of FDI from developed nations. According to Bangladesh Bank (2020), the United Kingdom remains the topmost nation that has invested a total of USD 435.36 million as FDI in Bangladesh in the fiscal year of 2019–2020, and this amount is tantamount to almost 19% of the total FDI that Bangladesh received at that time. Besides, the USA, Norway, Singapore, UAE and the Netherlands remain the top investors in Bangladesh in the fiscal year of 2019–2020 (see Fig. 3).

Net FDI inflows by major countries during the fiscal year of 2020 in Bangladesh. Source: Compiled by the authors adopting Bangladesh Bank (2020) data

Furthermore, the total amount of direct investment at a given point of time, commonly known as FDI stock, has been increasing in Bangladesh since 2014 (Fig. 4). According to the Bangladesh Bank (2020) report, at the end of June 2020, the stock position of inward FDI in Bangladesh hit USD 18,721.69 million, which was at least 0.2% higher than what Bangladesh received in June 2019. The USA has been ranked as the top country in terms of FDI stock (USD 3905.90 million) provider in Bangladesh in the fiscal year of 2020.

Trends in inward FDI stock in Bangladesh in million dollars. Source: Compiled by the authors exploiting Bangladesh Bank (2020) data

Theoretical and empirical literature review

We conducted the literature review focusing mostly the causality domain of FDI. The causality outcomes in the literature between FDI and GDP growth can be segregated into three categories. Studies either have identified a unidirectional causality (Abdouli and Hammami 2017; Sothan 2017; Sunde 2017) or a bidirectional causality (Ahmad et al. 2018; Omri et al. 2014; Peng et al. 2016) or no causality at all (Asheghian 2016; Yalta 2013). Very few studies analyzed the FDI–GDP growth nexus in Bangladesh (Hossain 2021; Hussain and Haque 2016; Sarker and Khan 2020); however, none has adopted the causality analysis between FDI–GDP growth nexus. A study conducted long ago found no causality in the FDI–GDP growth nexus in Bangladesh (Shimul et al. 2009). Therefore, the literature gap is evident, and our thorough literature review demands a fresh causality analysis in the FDI–GDP growth nexus in Bangladesh.

Moreover, most studies focusing on FDI–exchange rate nexus have assessed the effect of exchange rate and exchange rate volatility on the capital flow into host nations. Regarding the exchange rate volatility, studies have considered the appreciation or depreciation of the local currencies. However, these studies have shown mixed outcomes about the relationship between FDI and exchange rate. Some studies concluded that the appreciation of local currency helps to attain more FDI (Ullah et al. 2012), some found that the fixed exchange rate regimes are more powerful in obtaining FDI than the floating exchange rates (Ambaw and Sim 2018; Cushman and Vita 2017). Contrarily, few studies found that currency devaluation brings more FDI to the host nations (Xing 2006). Furthermore, studies on the exchange rate volatility demonstrated mixed outcomes as well: some unveiled positive association between exchange rate volatility and FDI (Ullah et al. 2012; Mensah et al. 2017), some unearthed negative association (Latief and Lefen 2018), and some notified no effect at all (Polat and Payaslıoğlu 2016). Bangladesh pioneers the floating exchange rate policy, and there are not too many studies focusing Bangladesh that dealt with the FDI–exchange rate nexus. So far Qamruzzaman et al. (2019) and Mostafa (2020) found that appreciation of exchange rate decreases FDI inflow in Bangladesh where Qamruzzaman et al. (2019) further observed a bidirectional causality in FDI–exchange rate nexus.

The literature on the FDI–inflation rate nexus has observed mixed outcomes too. For example, some studies disclosed a negative relationship (Agudze and Ibhagui 2021; Boateng et al. 2015; Rashid et al. 2017; Sabir et al. 2019) and some revealed a positive relationship (Bano et al. 2019; Boateng et al. 2017) between FDI–inflation nexus. Few other studies noted the existence of a significant relationship between FDI and inflation rate; however, these studies did not confirm the nature of the associations (Cavusoglu and Alsabr 2017; Çeviş and Camurdan, 2007). Moreover, the direction of causality between FDI and inflation has not been tested in the above-mentioned studies, and no such work has been conducted in the context of Bangladesh. Furthermore, there is still controversy regarding the effect of interest rate on FDI. Studies observed either a positive impact of interest rate on FDI (Mahmood 2018; Mishra and Jena 2019) or a negative impact (de Angelo et al. 2010; Chen 2018) or no effect at all (Hossain 2021). Regarding the studies in Bangladesh, Hossain (2021) observed no impact of interest rate on inward FDI; however, Mahmood (2018) observed a positive effect between FDI and interest rate in Bangladesh.

In addition, many papers in the FDI–TO nexus revealed a positive connection between FDI and TO (Asongu et al. 2018; Aziz and Mishra 2016; Okafor et al. 2017; Rjoub et al. 2017; Saleem et al. 2020). However, there are studies that claimed that TO does not play a significant role (Blonigen and Piger 2014) in drawing FDI. Against this backdrop, the FDI–TO nexus has not been assessed extensively in the context of Bangladesh. Among a handful of studies, Saleem et al. (2020) did not find any long-run cointegration between FDI and TO whereas Mahmood (2018) observed a negative association in the nexus. Moreover, there is no causality study so far in the FDI–TO nexus in Bangladesh.

Regarding the effect of the corporate tax rate on FDI, most of the scholarly attempts unveiled that corporate tax rate discourages the FDI inflow in host nations (Andersen et al. 2017; Du et al. 2014; Nazir et al. 2020; Tang et al. 2014). However, there are some conflicting outcomes as well. For example, Jones and Temouri (2016) observed very minimal impact of the tax rate on FDI among the OECD nations, and others found no effect at all (Hunady and Orviska 2014; Kinda 2018). A substantial number of studies on the FDI–corporate tax nexus unearthed a negative relationship in Bangladesh (Alam and Quazi 2003; Mahbub and Jongwanich 2019). However, none has conducted a causality analysis in the nexus. Besides, research within the FDI–wage rate nexus have mostly claimed that low wage rate attracts more FDI and persuades the foreign firms to mobilize their production units where the labor cost is minimum (Bilgili et al. 2012; Blanc-Brude et al. 2014; Economou 2019; Hunady and Orviska 2014). Few studies in Bangladesh have found labor cost as an important determinant of inward FDI; however, the dataset for these studies is not large (Nasrin et al. 2010; Sadekin et al. 2015). Moreover, none of these papers mentioned above has done a causality analysis in the FDI–wage rate nexus.

From the above discussion, it is evident that there is an insufficient number of studies focusing on FDI determinants in Bangladesh. No study conducted the causality analysis considering the economic determinants of FDI using a large dataset. In addition, there is no study that tested the determinants considering the structural break issue in the dataset. Besides, the FDI literature is teeming with conflicting outcomes; therefore, the findings of this study will help to evaluate the macroeconomic determinants from a different angle in the context of Bangladesh.

Methodology

Data and description of variables

This study has used the yearly time-series data of the dependent and independent variables spanning from 1975 to 2015. The inflation rate and wage rate data were collected from the Bangladesh Bureau of Statistics (BBS), corporate tax rate data were collected from the National Board of Revenue (NBR) and data on other variables (FDI data, GDP growth, interest rate, exchange rate and TO data) were collected from the World Development Indicators (WDI) of World Bank (2018). The descriptions of the variables have been incorporated in Table 1.

Unit root test and structural break

Non-stationary dataset may produce spurious regressions (Granger and Newbold 1974); hence, we applied several unit root tests to check the stationarity of our dataset. Initially, the Augmented Dickey–Fuller (ADF) test propounded by Dickey and Fuller (1979) is applied. However, with a structural break, this test performs poorly (Perron 1989). Therefore, another powerful test known as the KPSS test proposed by Kwiatkowski et al. (1992) has been used to test stationarity. Besides, the results have been cross-checked by Phillips–Perron (PP) test suggested by Phillips and Perron (1988). The Dickey–Fuller test can take the following format:

where δ = 1 represents the unit root, t is the deterministic time trend where t = 1, 2… T and Ɛt is the white noise error term. The testing procedure for the Augmented Dickey–Fuller (ADF) test is

Here, \({\Delta Y}_{t-1}=({Y}_{t-1}-{Y}_{t-2})\), \({\Delta Y}_{t-2}=\left({Y}_{t-2}-{Y}_{t-3}\right),\) etc. The lag order is selected based on Akaike Information Criterion (AIC) or Schwarz Bayesian Information Criterion (BIC). The KPSS test can be written as

where \({r}_{t}={r}_{t-1}+{u}_{t}\) is a random walk, \(\beta\) serves as an intercept, t is the time index, and \({u}_{t}\) is stationary error which is identically distributed (0, \({\sigma }^{2}u\)). To identify any major fluctuation in the FDI inflow in Bangladesh, this study has employed the Zivot and Andrews (2002) test to identify the presence of any structural break in the FDI dataset.

The VAR econometric model and Granger causality analysis

The basic model for this study is as follows:

Therefore, the empirical model can be written as follows:

where α is the constant and β’s are the regression parameter of the independent variables, \({X}_{jt}\) is the jth number of explanatory variables and \({\varepsilon }_{t}\) is the error term of the overall period.

The vector autoregression (VAR) model has been applied to trace the causality between FDI and other independent variables. We have harnessed this model for the following reasons. First, it enables both forecasting and estimation of the possible effects of the parameters on the dependent variable (Kennedy 2008). Second, this is a straightforward model where all the variables are treated as endogenous; therefore, there will be no exogenous and endogenous complexity (Gujarati 2003). The exogeneity condition is an important condition that needs to be met and if incorrectly specified it will generate erroneous outcomes. Third, this model provides all the necessary tools to describe the dynamic characteristics economic and financial time-series. Fourth, this model assists in estimating and predicting multiple time-series parameters in one single model. Fifth, VAR model allows other extensions like the usage of VECM model, IRF and VDC, which jointly assists in accurate estimation and forecasting. The VAR model including the matrix notation for k can be expressed as follows:

where \({X}_{t}\) = (\({X}_{1t}, {X}_{2t}\dots \dots \dots \dots , {X}_{kt}), {A}_{1}, {A}_{2}, \dots \dots \dots \dots . {A}_{p}\) are k × k matrices and \({U}_{t}\) is k dimensional vector of disturbance (Maddala and Kim 1998). In terms of the lag length selection, Akaike Information Criterion (AIC) (Akaike 1974) and Schwarz Bayesian Information Criterion (BIC) (Schwarz 1978) have been used.

We have further assessed the relationship between FDI and independent variables harnessing the Granger causality test proposed by Granger (1969). The Granger causality test for two stationary variables \({X}_{t}\) and \({Y}_{t}\) involve the estimation of following equation:

where \({\varepsilon }_{yt}\) and \({\varepsilon }_{xt}\) are uncorrelated white noise error terms. The null hypothesis is tested using F-test. When the p value is significant, the null hypothesis of the F-statistic is rejected, which implies that the first series Granger causes the second series and vice versa (Enders 1995).

Empirical model’s shock and robustness analysis

The impulse response function (IRF) has been used to identify the level of shock in the VAR model coming from the regressors to the FDI in Bangladesh. A more robust and extended response in the IRF in FDI due to the shock from one variable reveals that this particular variable causes FDI. Besides, IRF will also help to trace alternative shock between variables (in this case, from FDI to another regressor) (Enders 1995). This study has also exploited the variance decomposition (VDC) from an estimated VAR model. The VDC is bit different from the IRF. VDC determines the causality between two variables based on the relative contribution. Therefore, VDC is the way through which we can identify the most influential variable that affects FDI inflow the most in the case of Bangladesh.

To analyze the robustness of the VAR model, we have employed the vector error correction model (VECM). This model will help to find out the presence of a long-run relationship among different time-series data. To run the VECM model, we have first tested the existence of any co-integration relationship among the variables. Although the Engle and Granger (1987) test is popular for co-integration analysis; however, it can identify only a single co-integration; whereas the Johansen (1988) test permits more than one co-integration and considers all variables as endogenous (Koççat, 2008). The Johansen test is a combination of two tests; the maximum eigenvalue test and the trace test. For both cases, the null hypothesis is the r number of co-integration against an alternative hypothesis of more than r number of co-integrations. To execute the VECM model, an error correction model (ECM) constituting an error correction term (ECT) has been constructed. The ECT can be written as follows:

where \(\beta\) stands as cointegrating coefficient and \({\varepsilon }_{t}\) is the error derived from a regression of \({Y}_{t}\) on \({X}_{t}\). Therefore, the ECM can be written as follows:

where \({U}_{t}\) is independent and identically distributed, \({\varepsilon }_{t-1}\) is the equilibrium error of the previous period and if it is non-zero then the model is out of equilibrium and vice versa, \(\beta\) is the long-run parameter, \(\alpha\) and \(\gamma\) are short-run parameters. Furthermore, the model reliability has also been tested. The Jarque–Bera test is applied to test the normality of the main econometric model (Bera and Jarque 1981), the Breusch–Pagan test is applied to test the heteroskedasticity in the model (Breusch and Pagan 1979) and the Breusch–Godfrey Lagrange Multiplier (LM) test (Breusch 1978; Godfrey 1978) is applied to test the serial autocorrelation in the model.

Results and discussion

Unit root and structural break test results

We took advantage of three-unit root tests (ADF, KPSS and PP tests) to detect the unit root issues. The test outcomes (Table 2) delineate that all the time-series have unit root issues at the level confirmed by the ADF test. However, after the first difference, all the time-series become stationary at 1% level of significance (except for interest rate and wage, which are stationary at 10 and 5% level, respectively) shown by the ADF test. Similar outcomes have also been observed through the KPSS test and PP test (Table 2). Therefore, we can conclude that there is no unit root issue among the time-series after the first difference.

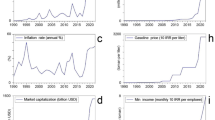

Regarding the structural break in the dataset, the Zivot–Andrew test identifies a break in 1995 among 21 observations. The break is portrayed in Fig. 5. From the figure, it is evident that in 1995, the inward FDI in Bangladesh experienced a shock and therefore, the total inflow reduced than the anterior and posterior years. The sudden fall in the FDI inflow in Bangladesh in 1995 was due to political unrest as the opposition parties called around 200 days of strikes. Due to the strikes, the business environment became so hostile that the MNCs and other foreign nations withdrew their investment from Bangladesh. However, in 1996 when a new democratic government came into power, the inflow jumped again.

Presence of structural break in the FDI inflow in Bangladesh in 1995. Source: World Bank Data (2018)

Analysis of VAR results and Granger causality test

As the variables are stationary at their first difference; therefore, we can now run the VAR model. Here, we have applied the first difference data to avoid any spurious regression among the variables. The optimal lag length selected by BIC is zero, whereas by AIC it is three. The AIC has the minimum value, so we choose lag three for our model. However, at lag three, there exists autocorrelation, which has been identified by the LM test (the discussion will follow in the model reliability section); hence, we have chosen lag two for our VAR model. At lag two, there is no autocorrelation problem.

The VAR model outcomes (Table 3) delineate that FDI is influenced by its own lag in Bangladesh. In contrast, interest rate (dinterest), corporate tax rate (dtax), exchange rate (dexchange) and wage rate (dwage) have no effect on inward FDI in Bangladesh. The findings of our paper contradict with the outcomes of other empirical endeavors. For instance, Boateng et al. (2015) observed that the exchange rate and interest rate significantly affect the inward FDI in Norway. Similar outcomes were also reported by Kumari and Sharma (2017), Mahmood (2018), and Mishra and Jena (2019). However, our finding regarding interest rate is in line with Hossain (2021). Interest rate in Bangladesh is not playing any crucial role in attracting foreign investment because of two major reasons. First, the deposit interest rate in Bangladesh’s financial institutions is not very attractive, and therefore investors feel reluctant to deposit their money (Hossain 2021). Second, the lending interest rate in Bangladesh is very high (a double-digit figure), which discourages potential investors to borrow money from banks in Bangladesh.

Regarding the effect of corporate tax rate, the findings of this paper are in line with several other studies (Hunady and Orviska 2014; Kinda 2018). The effect of corporate tax is insignificant in Bangladesh because the nation has failed to present an attractive tax, VAT, and customs policy. Consequently, venture capitalists and investor giants are less interested in investing in Bangladesh (at least up until 2015). Besides, due to the less attractive corporate taxation policy Bangladesh has been performing poorly in the ease of doing business index. Therefore, we recommend that the NBR should take meaningful initiatives to relax Bangladesh’s existing corporate tax policy to attract the MNCs that are looking for alternative homes for investment.

Furthermore, the wage rate does not have any effect on the inward FDI in Bangladesh (Table 3). Our finding contradicts with the findings of Fan et al. (2018), and Seetanah and Rojid (2011). This outcome is unacceptable given that Bangladesh is the world’s cheapest labor supplier. On an average, the wage rate in Bangladesh is below USD 100/month (The Guardian 2019). Contrarily, Bangladesh’s main competitors such as China, Vietnam, Indonesia and Cambodia provide labor for USD 150–260, 125–180, 110–180 and 180, respectively (The Financial Express 2020a); however, these nations are still the chosen destinations to MNCs for investment. Based on our observation, we can claim that domestic wage rate does not determine FDI in Bangladesh. Conversely, many studies unveiled that FDI can influence the wage rate among the host nations (Pandya 2010; Saucedo et al. 2020), and also FDI can enhance wage inequality (Te Velde and Morrissey 2004). The wage inequality is an effect of the differences of skill level of the domestic labors where highly skilled labors are paid handsomely by the MNCs. The issue with Bangladesh’s labor market is that most of the labors are unskilled who are apt for low-end manual jobs. As MNCs require skilled labors; hence, Bangladesh should focus more on the quality of the labor rather than the wage level. Therefore, policymakers must focus on developing skilled and semi-skilled labors through institutional and vocational training to build a more competitive labor market. Regarding the effect of exchange rate on inward FDI, we found no impact at all. One reason could be the unwillingness of currency devaluation (as BDT is gaining strength against USD) by the monetary policymakers. Bangladesh is still going through a negative Balance of Trade (BOT) (import > export); therefore, currency devaluation could bring a negative impact on Bangladesh’s international trade by making import even dearer. Another issue of currency devaluation would be high inflation. However, the devaluation can make the export more competitive and can increase the volume of total export. The export–FDI–exchange rate nexus in Bangladesh is very complex. For instance, Hossain (2021) observed that export and FDI are substitutes. For this reason, he suggested the FDI-led development as an intermediary solution until export can surpass the total import. In other words, strong export growth may decrease inward FDI in Bangladesh. Therefore, for an FDI-led development, this study suggests keeping up with the exchange rate appreciation policy.

Findings also delineate that the GDP growth rate, inflation rate and trade openness have a significant positive effect on inward FDI in Bangladesh. Our findings are also analogous with others (Aziz and Mishra 2016; Hossain 2021; Izadi et al. 2021). Although several studies (Agudze and Ibhagui 2021; Boateng et al. 2015; Rashid et al. 2017; Sabir et al. 2019) witnessed negative effect of inflation on FDI, we present a positive effect in the context of Bangladesh. The findings are also consistent with the findings of Bangladesh Bank and BBS. Bangladesh’s average inflation rates in 2018 and 2019 were 5.55 and 5.6%, respectively (The Daily Star 2020). During these years, Bangladesh received USD 2.58 and 3.89 billion as FDI, respectively (The Financial Express 2020b). Furthermore, we reveal that economic growth is a boon for attaining FDI in Bangladesh (Table 3). Bangladesh has been maintaining a steady growth rate of 7% or so since the last couple of years. Thus, the upward trend of inward FDI (Fig. 4) and high growth rate are perfectly compatible. Besides, Bangladesh liberalized its trade rules since the 1990s, and after that, has established many bilateral and multilateral trade relationships with other nations. Being open now, Bangladesh is more transparent to the MNCs, which opens new windows of international cooperation along with international fund transfer.

To put credibility on the outcomes in Table 3, we performed the Granger causality test to detect the direction of causation between FDI and other regressors (Table 4). It is obvious from the outcomes that the GDP growth rate does not Granger cause the FDI inflow in Bangladesh. This finding is completely different from what Hossain (2021) found in the case of Bangladesh. However, other studies have reported similar outcomes (Asheghian 2016; Temiz and Gökmen 2014). Further, the Granger causality test establishes that it is not the growth rate but the inflation and openness that cause FDI inflow in Bangladesh. The FDI–inflation–exchange rate nexus in Bangladesh is very complex. The bidirectional causality between FDI and inflation means both can cause each other. However, one causality is natural and the other one is superficial. For instance, as inflation soars, FDI inflow gets upsurged. Bangladesh receives FDI in the form of USD making BDT stronger against USD, which makes the import cheaper and the export dearer. Bangladesh is still experiencing a negative trade balance (import > export) and as long as this is the case, FDI-led development will be feasible for Bangladesh. Therefore, we claim that inflation causes FDI in Bangladesh and it is the natural causality.

Conversely, “FDI causes inflation” is less feasible for Bangladesh. Because, if FDI brings inflation, then the currency gets devalued (which is not the case in Bangladesh now) and as a consequence the export will increase and it will surpass the total import (export > import) (which is still not the case in Bangladesh) and most importantly, it will increase the wage rate which completely contradicts with the present labor cost of Bangladesh. Therefore, we can label this causation as superficial or fake at least for now. Hence, as long as the FDI-led development of Bangladesh holds true, “inflation causes FDI” will also hold true. Thus, this empirical finding will be one of the pioneering outcomes of this paper and will assist in mitigating the ongoing debate in the FDI–inflation–exchange rate nexus.

A unidirectional causality exists between interest rate and FDI in Bangladesh, but the direction goes from FDI to interest rate, not from interest rate to FDI. Hence, the interest rate is not an influential factor for FDI in Bangladesh (the reasons are mentioned above). Qamruzzaman et al. (2019)witnessed a bidirectional causality between FDI and exchange rate in Bangladesh using a non-linear ARDL framework. However, we have found no evidence of causality between FDI and exchange rate in Bangladesh. Besides, Rai and Sharma (2020) observed a bidirectional causality between FDI and corporate tax in Bangladesh and other South Asian nations; however, this paper did not find any such causality. Furthermore, wage rate Granger does not cause FDI inflow in Bangladesh which is dissimilar from other findings. For instance, Saleem et al. (2018) found bidirectional causality between labor cost and FDI in China. Lastly, this paper reveals bidirectional causality between FDI and TO in Bangladesh, which is consistent with Rathnayaka Mudiyanselage et al. (2021) in the case of Romania but different from Saleem et al. (2020) in the case of Bangladesh. Moreover, “TO causes FDI” and “FDI causes TO” both are natural relationships. Thus, the VAR-Granger endorses that inflation and TO are responsible for inward FDI in Bangladesh.

Impulse response function (IRF) and variance decomposition (VDC) findings analysis

The findings of the IRF are depicted in Fig. 6. In the IRF, for a dependent variable, any shock on explanatory variables causes the impulse response dies out to zero, which explains the stability of the VAR model. The response of FDI inflow due to the shock in the exchange rate is almost zero (a slight variation in the path initially and after that, there is no change in the time path). Same conclusion is valid for GDP growth, interest and wage rate, which discloses the poor explanatory power of these regressors. In the case of tax rate, we observe a negative trend, and immediately the trend moves into a positive shock which is around 5% at the early stage, and after year four, the shock dies out to zero. But in the case of shock in interest, exchange and wage rate, their innovations on FDI inflow are around zero for the whole period. Furthermore, the response of FDI inflow due to inflation shock is relatively trivial, and we found the impact only at the early stage. After year two, the impact of the shock is reduced to zero, and we do not observe any other influence throughout the whole period. In the case of openness, the result is quite clear. The innovation of openness influences the inflow of FDI up to year four by around 10%. After that, the shock reduces, and it dies out at year six. Therefore, the impulse response function summarizes that the impact on the inflow of FDI due to shock in openness lasts longer compared to the other explanatory variables. Thus, the result is very similar to the Granger causality test, where we found the bidirectional relationship between FDI and openness.

Impulse response function (IRF) analysis

The findings of the VDC are posted in Table 5. The VDC is calculated over a 10-year forecast horizon to determine how much of the forecast error variance for the variables in the model can be explained by innovations to each explanatory variable. From Table 5, FDI inflow is influenced by its own shock, which is 94.45% in year two, which gets reduced to 77.12 and 74.29% in year six and ten, respectively. Thus, in the long run, the influence of the own shock reduces. The VDC outcomes also unveil the explanatory power of the explanatory variables. In a 2-year time period (short-run), variables GDP, inflation, interest, tax, exchange and wage rate, and openness can explain 0.6, 1.0, 0.08, 0.03, 0.002, 0.02 and 3.5% of the variation of FDI inflow. Therefore, in the short run, the variation in the FDI inflow can be explained better by openness and inflation. However, openness has a more acute effect than inflation (in 6 years, the contribution of openness is 10.48%, whereas inflation is 0.8%). Again, for 10 years (long run), the contributions of GDP, inflation, interest, tax, exchange and wage rate, and openness to explain the variation of FDI inflow are 2.26, 1.06, 2.37, 6.41, 1.00, 2.41 and 10.16%, respectively. Therefore, from Table 5, we can conclude that openness has the maximum explanatory power to define FDI inflow in Bangladesh in both the short and long runs. It is also evident that inflation has better explanatory power in the short run and tax rate has better explanatory power than inflation in the long run to describe FDI inflow variation in Bangladesh.

Model reliability and robustness analysis

To test the model reliability, we have employed the Breusch–Godfrey Lagrange Multiplier (LM) autocorrelation test, Breusch–Pagan heteroskedasticity test and Jarque–Bera normality test. The outcome of the LM test is shown in Table 6. The Chi-squared value of the LM test at lag-2 is 79.28, and it proves that there is no autocorrelation in the model. The Breusch–Pagan test that holds a null hypothesis of no heteroskedasticity in the model shows a Chi-squared value of 0.14 where the probability of accepting the null is 71.33%. Therefore, we can establish that there is no heteroskedasticity in the model. Jarque–Bera test for normality of the model states that the residuals are normally distributed (see Table S1, appendix), and the probability of accepting the null in case of FDI, inflation, interest, exchange and wage rate, and openness are very high which are 18.52, 22.49, 28.68, 69.80, 79.16 and 58.54%, respectively. Lastly, the eigenvalue stability test results show (Table S2, appendix) that all the eigenvalues lie inside the unit circle, which satisfies the stability condition of the VAR. Therefore, we can say that the VAR model is stable and normal.

Moreover, we also conducted the Johansen test for our model. Johansen test assumes r number of cointegration as the null hypothesis where the alternative hypothesis is more than r number cointegration. The results (see Table A, additional fileFootnote 1) show that at level five, we cannot reject the null hypothesis for both the maximum eigenvalue test and the trace test. Therefore, we can conclude that both the eigenvalue and trace tests show five cointegrations among the variables.

Furthermore, the robustness of the baseline results of the VAR model is further assessed by the vector error correction model (VECM), and the outcomes are presented in Table 7. It is evident from Table 7 that the ECT is negative (−0.86) and influential as the short-run shock gets adjusted in the long run. The value lies between 0 and −1, which implies that the error correction process satisfies the equilibrium condition at an advanced rate, and a deviation of the FDI inflow from the equilibrium point in the previous period will be adjusted and fixed by 86.35% rate in the current period. The findings of the VECM debunk that short-run relationships exist between FDI–openness and FDI–inflation nexus. In contrast, GDP growth, tax, exchange and interest rates have no effect on inward FDI in Bangladesh. Moreover, the wage rate, to some extent, can influence FDI inflow in the short-run. Therefore, we can conclude that the outcomes of the VECM are reliable (although the level of significance is different) and mostly represent the outcomes of the main VAR model.

Conclusion and policy recommendation

This paper intends to unveil the uncharted causality between FDI and its macroeconomic determinants in Bangladesh, harnessing a secondary dataset from 1975 to 2015 and employing the vector autoregression (VAR) approach and Granger causality test. Besides, impulse response function (IRF) and variance decomposition (VDC) methods have been used to capture the response of FDI after a given shock on an explanatory variable. Furthermore, we have tested the stability of our empirical model through different tests and checked the robustness of the core VAR model by applying the VECM approach. Based on the VAR outcomes, only the GDP growth rate, inflation, and openness are the determinants of FDI in Bangladesh, whereas interest, exchange, tax and wage rate do not affect the inward FDI in Bangladesh. However, the Granger causality test further filters the determinants. According to the Granger causality test outcomes, GDP growth rate granger does not cause FDI in Bangladesh, and it's only the openness and inflation rate that cause FDI in Bangladesh.

Regarding openness and inflation, we observed a bidirectional causality. However, we observed a natural causality (inflation granger definitely causes FDI) and a superficial causality (FDI granger does not necessarily cause FDI) between FDI and inflation rate. As inflation causes FDI in Bangladesh, BDT becomes strong against USD (exchange rate gets appreciated) which makes the import cheaper and export dearer and this results the negative BOP (import > export). However, FDI does not necessarily cause inflation in Bangladesh, because if FDI causes inflation, then BDT gets depreciated which will ultimately bring a positive balance of payment (meaning the export will surpass the import), which is undoubtedly impossible for Bangladesh. In addition, if FDI would cause inflation then the labor cost would go up which is not a common labor market picture of Bangladesh. Moreover, the FDI-led development is not possible if FDI causes inflation. Therefore, “FDI causes inflation” is a superficial causality for Bangladesh and this is one of the pioneering findings of this paper which is not explored by any other work in Bangladesh so far.

Our findings also indicate that interest rate, corporate tax rate and wage rate do not play any role in obtaining FDI in Bangladesh. In case of interest rate, we have identified that the lending interest rate is very high in Bangladesh which discourages further investment; therefore, we recommend decreasing the lending interest rate so that people do not feel reluctant in borrowing from banks. Bangladesh has not yet officially declared any tax holidays or tax incentives for the MNCs regarding the corporate tax rate. Therefore, this macro-level determinant is still insignificant. We recommend the National Board of Revenue (NBR) to launch tax incentives and tax holidays for the MNCs so that they can feel that investment in Bangladesh is not a burden. Furthermore, we found that the wage rate does not draw foreign investment in Bangladesh, and it is very unlikely given that Bangladesh is the world’s cheapest labor supplier. We also claim that labor quality is more important that the wage rate of the domestic workers. Therefore, we propose developing a semi-skilled and skilled workforce through technical and vocational training to earn the confidence of the MNCs.

Furthermore, IRF results delineate that openness has the most explanatory power on the inward FDI in Bangladesh. Besides, the VDC outcomes also endorse that in the short-run, openness and inflation have the most explanatory power, whereas, in the long run, openness has the most and tax rate has even better explanatory power than inflation in Bangladesh. We have further checked the robustness of the baseline results of the VAR model through the VECM methodology, and we have found moderately similar outcomes that reveal that both openness and inflation are the major determinants of inward FDI in Bangladesh.

This paper particularly focused on the causality between FDI and its selected determinants in Bangladesh. In doing so, we only observed the structural break (SB) only on FDI in our model; however, we did not incorporate any effect of the SB in our main model, which is a limitation of this empirical endeavor. We will try to incorporate this in our future studies. Moreover, the availability of data was another important constraint for this study, which is why the true effect of the IRF was unclear. However, we have accommodated the effects of IRF through the VDC analysis.

Availability of data and materials

The datasets generated and/or analyzed during the current study are available in the [World Bank], [BBS] and [NBR] repository at the following URLs: https://datacatalog.worldbank.org/dataset/world-development-indicators, http://www.bbs.gov.bd/ and https://nbr.gov.bd/.

Code availability

Not applicable for current study.

Notes

Table A from Additional File constitutes the Johansen test cointegration outcomes.

References

Abdouli M, Hammami S (2017) Investigating the causality links between environmental quality, foreign direct investment and economic growth in MENA countries. Int Bus Rev 26(2):264–278. https://doi.org/10.1016/j.ibusrev.2016.07.004

ADB (2020) Economic Indicators for Bangladesh. Bangladesh: Economy | Asian Development Bank (www.adb.org). Accessed 10 April 2021

ADB (2021) Economic Indicators for Bangladesh. Bangladesh: Economy | Asian Development Bank (www.adb.org). Accessed 6 March 2022.

Agudze K, Ibhagui O (2021) Inflation and FDI in industrialized and developing economies. Int Rev Appl Econ. https://doi.org/10.1080/02692171.2020.1853683

Ahmad F, Draz MU, Yang SC (2018) Causality nexus of exports, FDI and economic growth of the ASEAN5 economies: evidence from panel data analysis. J Int Trade Econ Dev 27(6):685–700. https://doi.org/10.1080/09638199.2018.1426035

Akaike H (1974) A new look at the statistical model identification. IEEE Trans Autom Control 19(6):716–723. https://doi.org/10.1109/TAC.1974.1100705

Alam I, Quazi R (2003) Determinants of capital flight: an econometric case study of Bangladesh. Int Rev Appl Econ 17(1):85–103. https://doi.org/10.1080/713673164

Alam A, Uddin M, Yazdifar H (2019) Institutional determinants of R&D investment: Evidence from emerging markets. Technol Forecast Soc 138:34–44. https://doi.org/10.1016/j.techfore.2018.08.007

Alfalih AA, Hadj TB (2020) Foreign direct investment determinants in an oil abundant host country: Short and long-run approach for Saudi Arabia. Resour Policy 66:101616. https://doi.org/10.1016/j.resourpol.2020.101616

Ambaw DT, Sim N (2018) Is inflation targeting or the fixed exchange rate more effective for attracting FDI into developing countries? Appl Econ Lett 25(7):499–503. https://doi.org/10.1080/13504851.2017.1340563

Andersen MR, Kett BR, von Uexkull E (2017) Corporate tax incentives and FDI in developing countries. World Bankhttps://doi.org/10.1596/978-1-4648-1175-3_ch3

Arel-Bundock V (2017) The political determinants of foreign direct investment: a firm-level analysis. Int Interact 43(3):424–452. https://doi.org/10.1080/03050629.2016.1185011

Asheghian P (2016) GDP growth determinants and foreign direct investment causality: the case of Iran. J Int Trade Econ Dev 25(6):897–913. https://doi.org/10.1080/09638199.2016.1145249

Asiamah M, Ofori D, Afful J (2019) Analysis of the determinants of foreign direct investment in Ghana. J Asian Bus Econ Stud 26(1):56–75. https://doi.org/10.1108/JABES-08-2018-0057

Asongu S, Akpan US, Isihak SR (2018) Determinants of foreign direct investment in fast-growing economies: evidence from the BRICS and MINT countries. Financ Innov 4:26. https://doi.org/10.1186/s40854-018-0114-0

Aziz OG, Mishra AV (2016) Determinants of FDI inflows to Arab economies. J Int Trade Econ Dev 25(3):325–356. https://doi.org/10.1080/09638199.2015.1057610

Bangladesh Bank (2018) Foreign Direct Investment (FDI) in Bangladesh: Survey Report January-June, 2018. fdisurveyjanjun2018.pdf (bb.org.bd). Accessed 8 March 2022

Bangladesh Bank (2019) Foreign Direct Investment (FDI) in Bangladesh: Survey Report January-June, 2019. fdisurveyjanjun2019.pdf (bb.org.bd). Accessed 8 March 2022

Bangladesh Bank (2020) Foreign Direct Investment and External Debt. fdisurveyjanjun2020.pdf (bb.org.bd). Accessed 3 March 2021

Bano S, Zhao Y, Ahmad A, Wang S, Liu Y (2019) Why did FDI inflows of Pakistan decline? From the perspective of terrorism, energy shortage, financial instability, and political instability. Emerg Mark Financ Trade 55(1):90–104. https://doi.org/10.1080/1540496X.2018.1504207

Behuria AK (2018) How Sri Lanka walked into a debt trap, and the way out. Strateg Anal 42(2):168–178. https://doi.org/10.1080/09700161.2018.1439327

Bera AK, Jarque CM (1981) Efficient tests for normality, homoscedasticity and serial independence of regression residuals: Monte Carlo evidence. Econ Lett 7(4):313–318. https://doi.org/10.1016/0165-1765(81)90035-5

BIDA (2022) Bangladesh Investment Handbook. BIDA Publications, Dhaka

Bilgili F, Tülüce NS, Doğan I (2012) The determinants of FDI in Turkey: A Markov regime-switching approach. Econ Model 29(4):1161–1169. https://doi.org/10.1016/j.econmod.2012.04.009

Blanc-Brude F, Cookson G, Piesse J, Strange R (2014) The FDI location decision: distance and the effects of spatial dependence. Int Bus Rev 23(4):797–810. https://doi.org/10.1016/j.ibusrev.2013.12.002

Blonigen BA, Piger J (2014) Determinants of foreign direct investment. Can J Econ 47(3):775–812. https://doi.org/10.1111/caje.12091

Boateng A, Hua X, Nisar S, Wu J (2015) Examining the determinants of inward FDI: evidence from Norway. Econ Model 47:118–127. https://doi.org/10.1016/j.econmod.2015.02.018

Boateng E, Amponsah M, Annor Baah C (2017) Complementarity effect of financial development and FDI on investment in Sub-Saharan Africa: a panel data analysis. Afr Dev Rev 29(2):305–318. https://doi.org/10.1111/1467-8268.12258

Brautigam D (2020) A critical look at Chinese ‘debt-trap diplomacy’: The rise of a meme. Area Dev Policy 5(1):1–14. https://doi.org/10.1080/23792949.2019.1689828

Breusch TS (1978) Testing for autocorrelation in dynamic linear models. Austr Econ Papers 17:334–355. https://doi.org/10.1111/j.1467-8454.1978.tb00635.x

Breusch TS, Pagan AR (1979) A simple test for heteroscedasticity and random coefficient variation. Econometrica 47(5):1287–1294. https://doi.org/10.2307/1911963

The Business Standard (2020) How the country paid for the dream project. www.tbsnews.net. Accessed 3 March 2021.

Cavusoglu B, Alsabr M (2017) An ARDL co-integration approach to inflation, FDI and economic growth in Libya. J Adv Res Law Econ 8:2373

Çeviş I, Camurdan B (2007) The economic determinants of foreign direct investment in developing countries and transition economies. Pak Dev Rev 46(3):285–299

Chanegriha M, Stewart C, Tsoukis C (2017) Identifying the robust economic, geographical and political determinants of FDI: an extreme bounds analysis. Empir Econ 52:759–776. https://doi.org/10.1007/s00181-016-1097-1

Chen HJ (2018) Innovation, FDI, and the long-run effects of monetary policy. Rev Int Econ 26(5):1101–1129. https://doi.org/10.1111/roie.12351

Contractor FJ, Nuruzzaman N, Dangol R, Raghunath S (2021) How FDI inflows to emerging markets are influenced by country regulatory factors: an exploratory study. J Int Manag 27(1):100834. https://doi.org/10.1016/j.intman.2021.100834

Contractor FJ, Dangol R, Nuruzzaman N, Raghunath S (2020) How do country regulations and business environment impact foreign direct investment (FDI) inflows? Int Bus Rev 29(2):101640. https://doi.org/10.1016/j.ibusrev.2019.101640

Cushman DO, De Vita G (2017) Exchange rate regimes and FDI in developing countries: a propensity score matching approach. J Int Money Finance 77:143–163. https://doi.org/10.1016/j.jimonfin.2017.07.018

de Angelo CF, Eunni RV, Fouto NM (2010) Determinants of FDI in emerging markets: evidence from Brazil. Int J Commerce Manag 20(3):203–216. https://doi.org/10.1108/10569211011076901

Deseatnicov I, Akiba H (2016) Exchange rate, political environment and FDI decision. Int Econ 148:16–30. https://doi.org/10.1016/j.inteco.2016.05.002

Dhaka Tribune (2020) FDI in Bangladesh falls by 32% in H1 of 2020. Dhaka Tribune

Dickey DA, Fuller WA (1979) Distribution of the estimators for autoregressive time series with a unit root. J Am Stat Assoc 74(366a):427–431. https://doi.org/10.1080/01621459.1979.10482531

Du L, Harrison A, Jefferson G (2014) FDI spillovers and industrial policy: the role of tariffs and tax holidays. World Dev 64:366–383. https://doi.org/10.1016/j.worlddev.2014.06.005

Economou F (2019) Economic freedom and asymmetric crisis effects on FDI inflows: the case of four South European economies. Res Int Bus Finance 49:114–126. https://doi.org/10.1016/j.ribaf.2019.02.011

Enders W (1995) Applied Econometric Time Series, 14th edn. Wiley, New York

Engle RF, Granger CW (1987) Co-integration and error correction: representation, estimation, and testing. Econometrica J Econ Soc. https://doi.org/10.2307/1913236

ESCAP (2020) Foreign Direct Investment Trends and Outlook in Asia and the Pacific 2020/2021. www.unescap.org. Accessed 3 March 2021.

Fan H, Lin F, Tang L (2018) Minimum wage and outward FDI from China. J Dev Econ 135:1–19. https://doi.org/10.1016/j.jdeveco.2018.06.013

Godfrey LG (1978) Testing against general autoregressive and moving average error models when the regressors include lagged dependent variables. Econometrica J Econ Soc 46(6):1293–1301

Granger CWJ (1969) Investigating causal relations by econometric models and cross-spectral methods. Econometrica J Econ Soc 37(3):424–438. https://doi.org/10.2307/1912791

Granger CWJ, Newbold P (1974) Spurious regressions in econometrics. J Econom 2(2):111–120. https://doi.org/10.1016/0304-4076(74)90034-7

The Guardian (2019) Why are wages so low for garment workers in Bangladesh? The Guardian

Gujarati DN (2003) Basic econometrics. Megraw-Hill, New York, pp 363–369

Gupta J (2018) Trends and macro-economic determinants of FDI inflows to India. In: Singh M, Gupta P, Tyagi V, Flusser J, Ören T (eds) Advances in computing and data sciences. ICACDS 2018. Communications in computer and information science, vol 906. Springer, Singapore

Hossain MR (2021) Inward foreign direct investment in Bangladesh: Do we need to rethink about some of the macro-level quantitative determinants? SN Bus Econ 1(3):1–23. https://doi.org/10.1007/s43546-021-00050-z

Hou L, Li Q, Wang Y, Yang X (2021) Wages, labor quality, and FDI inflows: a new non-linear approach. Econ Model 102:105557. https://doi.org/10.1016/j.econmod.2021.105557

Hu D, You K, Esiyok B (2021) Foreign direct investment among developing markets and its technological impact on host: evidence from spatial analysis of Chinese investment in Africa. Technol Forecast Soc 166:120593. https://doi.org/10.1016/j.techfore.2021.120593

Hunady J, Orviska M (2014) Determinants of foreign direct investment in EU countries–do corporate taxes really matter? Procedia Econ Finance 12:243–250. https://doi.org/10.1016/S2212-5671(14)00341-4

Hussain ME, Haque M (2016) Foreign direct investment, trade, and economic growth: an empirical analysis of Bangladesh. Economies 4(2):7. https://doi.org/10.3390/economies4020007

Ibrahim OA, Abdel-Gadir SE (2015) Motives and determinants of FDI: a VECM analysis for Oman. Glob Bus Rev 16(6):936–946. https://doi.org/10.1177/0972150915597596

Ibrahim OA, Devesh S, Shaukat M (2020) Institutional determinants of FDI in Oman: Causality analysis framework. Int J Finance Econ. https://doi.org/10.1002/ijfe.2366

Izadi S, Rashid M, Izadi P (2021) FDI inflow and financial channels: international evidence before and after crises. J Financ Econ Policy. https://doi.org/10.1108/JFEP-04-2020-0091

Jaiblai P, Shenai V (2019) The determinants of FDI in sub-Saharan economies: A study of data from 1990–2017. Int J Financ Stud 7(3):43. https://doi.org/10.3390/ijfs7030043

Johansen S (1988) Statistical analysis of cointegration vectors. J Econ Dyn Control 12(2–3):231–254. https://doi.org/10.1016/0165-1889(88)90041-3

Jones C, Temouri Y (2016) The determinants of tax haven FDI. J World Bus 51(2):237–250. https://doi.org/10.1016/j.jwb.2015.09.001

Kennedy P (2008) A guide to econometrics, 6th edn. Blackwell Publishing, Oxford

Kinda T (2018) The quest for non-resource-based FDI: Do taxes matter? Macroecon Finance Emerg Market Econ 11(1):1–8. https://doi.org/10.1080/17520843.2016.1244095

Kishor N, Singh RP (2015) Determinants of FDI and its impact on BRICS countries: a panel data approach. Transnatl Corp Rev 7(3):269–278. https://doi.org/10.5148/tncr.2015.7302

Kleineick J, Ascani A, Smit M (2020) Multinational investments across Europe: a multilevel analysis. Rev Reg Res 40(1):67–105. https://doi.org/10.1007/s10037-020-00139-2

Koççat H (2008) Exchange rates, exports and economic growth in Turkey: evidence from Johansen cointegration tests. J Econ Manag Perspect 2(1):5–11

Kumari R, Sharma A (2017) Determinants of foreign direct investment in developing countries: a panel data study. Int J Emerg Mark 12(4):658–682. https://doi.org/10.1108/IJoEM-10-2014-0169

Kurtović S, Maxhuni N, Halili B, Talović S (2020) The determinants of FDI location choice in the Western Balkan countries. Post-Communist Econ 32(8):1089–1110. https://doi.org/10.1080/14631377.2020.1722584

Kwiatkowski D, Phillips PC, Schmidt P, Shin Y (1992) Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? J Econom 54(1–3):159–178. https://doi.org/10.1016/0304-4076(92)90104-Y

Latief R, Lefen L (2018) The effect of exchange rate volatility on international trade and foreign direct investment (FDI) in developing countries along “one belt and one road.” Int J Financ Stud 6(4):86. https://doi.org/10.3390/ijfs6040086

Liu WS, Agbola FW, Dzator JA (2016) The impact of FDI spillover effects on total factor productivity in the Chinese electronic industry: a panel data analysis. J Asia Pac Econ 21(2):217–234. https://doi.org/10.1080/13547860.2015.1137473

Liu H, Islam MA, Khan MA, Hossain MI, Pervaiz K (2020) Does financial deepening attract foreign direct investment? Fresh evidence from panel threshold analysis. Res Int Bus Finance 53:101198. https://doi.org/10.1016/j.ribaf.2020.101198

Maddala GS, Kim IM (1998) Unit roots, cointegration, and structural change. Cambridge University Press, Cambridge

Mahbub T, Jongwanich J (2019) Determinants of foreign direct investment (FDI) in the power sector: a case study of Bangladesh. Energy Strategy Rev 24:178–192. https://doi.org/10.1016/j.esr.2019.03.001

Mahmood H (2018) An investigation of macroeconomic determinants of FDI inflows in Bangladesh. Acad Account Financ Stud J 22(1):1–7

Mensah L, Bokpin GA, Dei Fosu-Hene E (2017) Foreign exchange rate moments and FDI in Ghana. J Econ Finance 41(1):136–152. https://doi.org/10.1007/s12197-015-9342-6

Mishra B, Jena P (2019) Bilateral FDI flows in four major Asian economies: a gravity model analysis. J Econ Stud 46(1):71–89. https://doi.org/10.1108/JES-07-2017-0169

Mostafa MM (2020) Impacts of inflation and exchange rate on foreign direct investment in Bangladesh. Int J Sci Bus 4(11):53–69

Mourao PR (2018) What is China seeking from Africa? An analysis of the economic and political determinants of Chinese Outward Foreign Direct Investment based on Stochastic Frontier Models. China Econ Rev 48:258–268. https://doi.org/10.1016/j.chieco.2017.04.006

Nasrin S, Baskaran A, Muchie M (2010) Major determinants and hindrances of FDI inflow in Bangladesh: perceptions and experiences of foreign investors and policymakers. In GLOBELICS-8th International Conference. Making Innovation Work for Society: Linking, Leveraging and Learning, Nov 1, p. 1–3

Nazir MS, Hafeez Q, U-Din S (2020) Did reduction in corporate tax rate attract FDI in Pakistan? Int J Finance Econ. https://doi.org/10.1002/ijfe.2271

Ning L, Wang F (2018) Does FDI bring environmental knowledge spillovers to developing countries? The role of the local industrial structure. Environ Resour Econ 71(2):381–405. https://doi.org/10.1007/s10640-017-0159-y

Okafor G, Piesse J, Webster A (2017) FDI determinants in least recipient regions: the case of sub-Saharan Africa and MENA. Afr Dev Rev 29(4):589–600. https://doi.org/10.1111/1467-8268.12298

Oladipo OS (2013) Does foreign direct investment cause long run economic growth? Evidence from the Latin American and the Caribbean countries. Int Econ Econ Policy 10:569–582. https://doi.org/10.1007/s10368-012-0225-4

Omri A, Nguyen DK, Rault C (2014) Causal interactions between CO2 emissions, FDI, and economic growth: evidence from dynamic simultaneous-equation models. Econ Model 42:382–389. https://doi.org/10.1016/j.econmod.2014.07.026

Osabutey EL, Okoro C (2015) Political risk and foreign direct investment in Africa: the case of the Nigerian telecommunications industry. Thunderbird Int Bus Rev 57(6):417–429. https://doi.org/10.1002/tie.21672

Pandya SS (2010) Labor markets and the demand for foreign direct investment. Int Org 64(3):389–409

Paul J, Jadhav P (2019) Institutional determinants of foreign direct investment inflows: evidence from emerging markets. Int J Emerg Mark 15(2):245–261. https://doi.org/10.1108/IJOEM-11-2018-0590

Peng H, Tan X, Li Y, Hu L (2016) Economic growth, foreign direct investment and CO2 emissions in China: a panel granger causality analysis. Sustainability 8(3):233. https://doi.org/10.3390/su8030233

Perron P (1989) The great crash, the oil price shock, and the unit root hypothesis. Econometrica J Econ Soc. https://doi.org/10.2307/1913712

Phillips PC, Perron P (1988) Testing for a unit root in time series regression. Biometrika 75(2):335–346. https://doi.org/10.1093/biomet/75.2.335

Polat B, Payaslıoğlu C (2016) Exchange rate uncertainty and FDI inflows: the case of Turkey. Asia-Pac J Account Econ 23(1):112–129. https://doi.org/10.1080/16081625.2015.1032312

Qamruzzaman M, Karim S, Wei J (2019) Does asymmetric relation exist between exchange rate and foreign direct investment in Bangladesh? Evidence from nonlinear ARDL analysis. J Asian Finance Econ Bus 6(4):115–128. https://doi.org/10.13106/jafeb.2019.vol6.no4.115

Rai SK, Sharma AK (2020) Causal Nexus between FDI inflows and its determinants in SAARC countries. South Asia Econ J 21(2):193–215. https://doi.org/10.1177/1391561420940838

Rashid M, Looi XH, Wong SJ (2017) Political stability and FDI in the most competitive Asia Pacific countries. J Financ Econ Policy 9(2):140–155. https://doi.org/10.1108/JFEP-03-2016-0022

Rathnayaka Mudiyanselage MM, Epuran G, Tescașiu B (2021) Causal links between trade openness and foreign direct investment in Romania. J Risk Financ Manag 14(3):90. https://doi.org/10.3390/jrfm14030090

Rjoub H, Aga M, Abu Alrub A, Bein M (2017) Financial reforms and determinants of FDI: evidence from landlocked countries in Sub-Saharan Africa. Economies 5(1):1. https://doi.org/10.3390/economies5010001

Sabir S, Rafique A, Abbas K (2019) Institutions and FDI: evidence from developed and developing countries. Financ Innov 5(1):1–20. https://doi.org/10.1186/s40854-019-0123-7

Sadekin M, Muzib M, Al Abbasi AA (2015) Contemporary situation of FDI and its determinants: Bangladesh scenario. Am J Trade Policy 2(2):121–124

Saleem H, Jiandong W, Khan MB, Khilji BA (2018) Reexamining the determinants of foreign direct investment in China. Transnatl Corp Rev 10(1):53–68. https://doi.org/10.1080/19186444.2018.1436654

Saleem H, Shabbir MS, Khan B, Aziz S, Husin MM, Abbasi BA (2020) Estimating the key determinants of foreign direct investment flows in Pakistan: new insights into the co-integration relationship. South Asian J Bus Stud 10(1):91–108. https://doi.org/10.1108/SAJBS-07-2019-0123

Sarker B, Khan F (2020) Nexus between foreign direct investment and economic growth in Bangladesh: an augmented autoregressive distributed lag bounds testing approach. Financ Innov 6(1):10. https://doi.org/10.1186/s40854-019-0164-y

Saucedo E, Ozuna T, Zamora H (2020) The effect of FDI on low and high-skilled employment and wages in Mexico: a study for the manufacture and service sectors. J Labour Mark Res 54(1):1–15. https://doi.org/10.1186/s12651-020-00273-x

Schwarz G (1978) Estimating the dimension of a model. Ann Stat 6(2):461–464. https://doi.org/10.1214/aos/1176344136

Seetanah B, Rojid S (2011) The determinants of FDI in Mauritius: a dynamic time series investigation. Afr J Econ Manag 2(1):24–41. https://doi.org/10.1108/20400701111110759

Sharma R, Kautish P (2020) Examining the nonlinear impact of selected macroeconomic determinants on FDI inflows in India. J Asia Bus Stud 14(5):711–733. https://doi.org/10.1108/JABS-10-2019-0316

Shimul SN, Abduallah SM, Siddiqua S (2009) An examination of FDI and growth nexus in Bangladesh: Engle Granger and bound testing cointegration approach. BRAC Univ J 6(1):69–76

Sothan S (2017) Causality between foreign direct investment and economic growth for Cambodia. Cogent Econ Finance 5(1):1277860. https://doi.org/10.1080/23322039.2016.1277860

Sunde T (2017) Foreign direct investment, exports and economic growth: ADRL and causality analysis for South Africa. Res Int Bus Finance 41:434–444. https://doi.org/10.1016/j.ribaf.2017.04.035

Tang CF, Yip CY, Ozturk I (2014) The determinants of foreign direct investment in Malaysia: a case for electrical and electronic industry. Econ Model 43:287–292. https://doi.org/10.1016/j.econmod.2014.08.017

Te Velde D, Morrissey O (2004) Foreign direct investment, skills and wage inequality in East Asia. J Asia Pac Econ 9(3):348–369. https://doi.org/10.1080/1354786042000272991

Temiz D, Gökmen A (2014) FDI inflow as an international business operation by MNCs and economic growth: an empirical study on Turkey. Int Bus Rev 23(1):145–154. https://doi.org/10.1016/j.ibusrev.2013.03.003

The Daily Star (2020) Inflation crawling up. The Daily Star

The Financial Express (2020a) Removing hurdles to higher FDI inflow. www.thefinancialexpress.com.bd. Accessed 12 March 2021

The Financial Express (2020b) Covid causes nearly 40pc decline in FDI inflow into Bangladesh. www.thefinancialexpress.com.bd. Accessed 13 March 2021.

Tomohara A, Takii S (2011) Does globalization benefit developing countries? Effects of FDI on local wages. J Policy Model 33(3):511–521. https://doi.org/10.1016/j.jpolmod.2010.12.010

Ullah S, Haider SZ, Azim P (2012) Impact of exchange rate volatility on foreign direct investment: a case study of Pakistan. Pak Econ Soc Rev 50(2):121–138

Vi Dũng N, BíchThủy ĐT, NgọcThắng N (2018) Economic and non-economic determinants of FDI inflows in Vietnam: a sub-national analysis. Post-Communist Econ 30(5):693–712. https://doi.org/10.1080/14631377.2018.1458458

World Bank (2018) World development indicators 2018. World Bank, Washington, DC. https://datacatalog.worldbank.org/dataset/world-development-indicators. Accessed 13 August 2018

World Bank (2020) South Asia: Prospects of an Economic Rebound. www.worldbank.org. Accessed 11 March 2021

Xing Y (2006) Exchange Rate Policy and the Relative Distribution of FDI Among Host Countries. BOFIT Discussion Paper No. 15/2006. DOI: https://doi.org/10.2139/ssrn.1002515

Yalta AY (2013) (2013) Revisiting the FDI-led growth hypothesis: the case of China. Econ Model 31:335–343. https://doi.org/10.1016/j.econmod.2012.11.030

Yimer A (2017) Macroeconomic, political, and institutional determinants of FDI inflows to Ethiopia: an ARDL approach. In: Heshmati A (ed) Studies on economic development and growth in selected African countries frontiers in African business research. Springer, Singapore

Zhang H, Yang X (2016) Trade-related aspects of intellectual property rights agreements and the upsurge in foreign direct investment in developing countries. Econ Anal Policy 50:91–99. https://doi.org/10.1016/j.eap.2016.03.001

Zivot E, Andrews DW (2002) Further evidence on the great crash, the oil-price shock, and the unit-root hypothesis. J Bus Econ Stat 20(1):25–44. https://doi.org/10.1198/073500102753410372

Acknowledgements

The authors would like to thank the Government of Bangladesh for funding the research and the University of Leeds for collaboration to conduct the research work. In addition, the authors gratefully acknowledge the contribution of the research supervisor Dr. Fazil Acar for his valuable time and suggestions.

Funding

The research was supported and funded by the Government of Bangladesh under the project of “Strengthening Government through Capacity Development of BCS Cadre Officials”.

Author information

Authors and Affiliations

Contributions

Mohammad Razib Hossain and Niaz Morshed have contributed equally. Mohammad Razib Hossain wrote the whole paper and Niaz Morshed did the analysis. Both authors will be considered as the first authors of this manuscript. Both authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no competing interests.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Morshed, N., Hossain, M.R. Causality analysis of the determinants of FDI in Bangladesh: fresh evidence from VAR, VECM and Granger causality approach. SN Bus Econ 2, 64 (2022). https://doi.org/10.1007/s43546-022-00247-w

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s43546-022-00247-w