Abstract

Electric vehicles (EVs) are experiencing a rise in popularity over the past few years as the technology has matured and costs have declined, and support for clean transportation has promoted awareness, increased charging opportunities, and facilitated EV adoption. Suitably, a vast body of literature has been produced exploring various facets of EVs and their role in transportation and energy systems. This paper provides a timely and comprehensive review of scientific studies looking at various aspects of EVs, including: (a) an overview of the status of the light-duty-EV market and current projections for future adoption; (b) insights on market opportunities beyond light-duty EVs; (c) a review of cost and performance evolution for batteries, power electronics, and electric machines that are key components of EV success; (d) charging-infrastructure status with a focus on modeling and studies that are used to project charging-infrastructure requirements and the economics of public charging; (e) an overview of the impact of EV charging on power systems at multiple scales, ranging from bulk power systems to distribution networks; (f) insights into life-cycle cost and emissions studies focusing on EVs; and (g) future expectations and synergies between EVs and other emerging trends and technologies. The goal of this paper is to provide readers with a snapshot of the current state of the art and help navigate this vast literature by comparing studies critically and comprehensively and synthesizing general insights. This detailed review paints a positive picture for the future of EVs for on-road transportation, and the authors remain hopeful that remaining technology, regulatory, societal, behavioral, and business-model barriers can be addressed over time to support a transition toward cleaner, more efficient, and affordable transportation solutions for all.

Export citation and abstract BibTeX RIS

This article was updated on 29 April 2021 to add the name of the fifth author and to correct the name of the eighth author.

1. Introduction

First introduced at the end of the 1800s, electric vehicles (EVs) 12 have been experiencing a rise in popularity over the past few years as the technology has matured and costs (especially of batteries) have declined substantially. Worldwide support for clean transportation options (i.e. low emissions of greenhouse gasses [GHG] to mitigate climate change and criteria pollutants) has promoted awareness, increased charging opportunities, and facilitated adoption of EVs. EVs present numerous advantages compared to fossil-fueled internal-combustion-engine vehicles (ICEVs), inter alia: zero tailpipe emissions, no reliance on petroleum, improved fuel economy, lower maintenance, and improved driving experience (e.g. acceleration, noise reduction, and convenient home and opportunity recharging). Further, when charged with clean electricity, EVs provide a viable pathway to reduce overall GHG emissions and decarbonize on-road transportation. This decarbonization potential is important, given limited alternative options to liquid fossil fuels. The ability of EVs to reduce GHG emissions is dependent, however, upon clean electricity. Therefore, EV success is intertwined closely with the prospect of abundant and affordable renewable electricity (in particular solar and wind electricity) that is poised to transform power systems (Jacobson et al 2015, Kroposki et al 2017, Gielen et al 2019, IEA 2020b). Coordinated actions can produce beneficial synergies between EVs and power systems and support renewable-energy integration to optimize energy systems of the future to benefit users and offer decarbonization across sectors (CEM 2020). A cross-sectoral approach across the entire energy system is required to realise clean future transformation pathways (Hansen et al 2019). EVs are expected to play a critical role in the power system of the future (Muratori and Mai).

EV success is increasing rapidly since the mid-2010s. EV sales are breaking previous records every year, especially for light-duty vehicles (LDVs), buses, and smaller vehicles such as three-wheelers, mopeds, kick-scooters, and e-bikes (IEA 2017, 2018a, 2019, 2020). To date, global automakers are committing more than $140 billion to transportation electrification, and 50 light-duty EV models are available commercially in the U.S. market (Moore and Bullard 2020). Approximately 130 EV models are anticipated by 2023 (AFDC 2020, Moore and Bullard 2020). Future projections of the role of EVs in LDV markets vary widely, with estimates ranging from limited success (∼10% of sales in 2050) to full market dominance, with EVs accounting for 100% of LDV sales well before 2050. Many studies project that EVs will become economically competitive with ICEVs in the near future or that they are already cost-competitive for some applications (Weldon et al 2018, Sioshansi and Webb 2019, Yale E360 2019, Kapustin and Grushevenko 2020). However, widespread adoption requires more than economic competitiveness, especially for personally owned vehicles. Behavioral and non-financial preferences of individuals on different technologies and mobility options are also important (Lavieri et al 2017, Li et al 2017, McCollum et al 2018, Ramea et al 2018). EV adoption beyond LDVs has been focused on buses, with significant adoption in several regions (especially China). Electric trucks also are receiving great attention, and Bloomberg New Energy Finance (BloombergNEF) projects that by 2025, alternative fuels will compete with, or outcompete, diesel in long-haul trucking applications (Moore and Bullard 2020). These recent successes are being driven by technological progress, especially in batteries and power electronics, greater availability of charging infrastructure, policy support driven by environmental benefits, and consumer acceptance. EV adoption is engendering a virtuous circle of technology improvements and cost reductions that is enabled and constrained by positive feedbacks arising from scale and learning by doing, research and development, charging-infrastructure coverage and utilization, and consumer experience and familiarity with EVs.

Vehicle electrification is a game-changer for the transportation sector due to major energy and environmental implications driven by high vehicle efficiency (EVs are approximately 3–4 times more efficient than comparable ICEVs), zero tailpipe emissions, and reduced petroleum dependency (great fuel diversity and flexibility exist in electricity production). Far-reaching implications for vehicle-grid integration extend to the electricity sector and to the broader energy system. A revealing example of the role of EVs in broader energy-transformation scenarios is provided by Muratori and Mai, who summarize results from 159 scenarios underpinning the special report on Global Warming of 1.5 °C (SR1.5) by Intergovernmental Panel on Climate Change (IPCC). Muratori and Mai also show that transportation represents only ∼2% of global electricity demand currently (with rail responsible for more than two-thirds of this total). They show that electricity is projected to provide 18% of all transportation-energy needs by 2050 for the median IPCC scenario, which would account for 10% of total electricity demand. Most of this electricity use is targeted toward on-road vehicle electrification. These projections are the result of modeling and simulations that are struggling to keep pace with the EV revolution and its role in energy-transformation scenarios as EV technologies and mobility are evolving rapidly (McCollum et al 2017, Venturini et al 2019, Muratori et al 2020). Recent studies explore higher transportation-electrification scenarios: for example, Mai et al (2018) report a scenario in which 75% of on-road miles are powered by electricity, and transportation represents almost a quarter of total electricity use during 2050.

Vehicle electrification is a disruptive element in energy-system evolution that radically changes the roles of different sectors, technologies, and fuels in long-term transformation scenarios. Traditionally, energy-system-transformation studies project minimal end-use changes in transportation-energy use over time (limited mode shifting and adoption of alternative fuels), and the sector is portrayed as a 'roadblock' to decarbonization. In many decarbonization scenarios, transportation is seen traditionally as one of the biggest hurdles to achieve emissions reductions (The White House 2016). These scenarios rely on greater changes in the energy supply to reduce emissions and petroleum dependency (e.g. large-scale use of bioenergy, often coupled to carbon capture and sequestration) rather than demand-side transformations (IPCC 2014, Pietzcker et al 2014, Creutzig et al 2015, Muratori et al 2017, Santos 2017). In most of these studies, electrification is limited to some transportation modes (e.g. light-duty), and EVs are not expected to replace ICEVs fully (The White House 2016). More recently, however, major mobility disruptions (e.g. use of ride-hailing and vehicle ride-sharing) and massive EV adoption across multiple applications are proposed (Edelenbosch et al 2017, Van Vuuren et al 2017, Hill et al 2019, E3 2020, Zhang and Fujimori 2020). These mobility disruptions allow for more radical changes and increase the decarbonization role of transportation and highlight the integration opportunities between transportation and energy supply, especially within the electricity sector. For example, Zhang and Fujimori (2020) highlight that for vehicle electrification to contribute to climate-change mitigation, electricity generation needs to transition to clean sources. They note that EVs can reduce mitigation costs, implying a positive impact of transport policies on the economic system (Zhang and Fujimori 2020). In-line with these projections, many countries are establishing increasingly stringent and ambitious targets to support transport electrification and in some cases ban conventional fossil fuel vehicles (Wentland 2016, Dhar et al 2017, Coren 2018, CARB 2020, State of California 2020).

EV charging undoubtedly will impact the electricity sector in terms of overall energy use, demand profiles, and synergies with electricity supply. Mai et al (2018) show that in a high-electrification scenario, transportation might grow from the current 0.2% to 23% of total U.S. electricity demand in 2050 and significantly impact system peak load and related capacity costs if not controlled properly. Widespread vehicle electrification will impact the electricity system across the board, including generation, transmission, and distribution. However, expected changes in U.S. electricity demand as a result of vehicle electrification are not greater than historical growth in load and peak demand. This finding suggests that bulk-generation capacity is expected to be available to support a growing EV fleet as it evolves over time, even with high EV-market growth (U.S. DRIVE 2019). At the same time, many studies have shown that 'smart charging' and vehicle-to-grid (V2G) services create opportunities to reduce system costs and facilitate the integration of variable renewable energy (VRE). Charging infrastructure that enables smart charging and alignment with VRE generation, as well as business models and programs to compensate EV owners for providing charging flexibility, are the most pressing required elements for successfully integrating EVs with bulk power systems. At the local level, EV charging could increase and change electricity loads significantly, which could impact distribution networks and power quality and reliability (FleetCarma 2019). Distribution-network impacts can be particularly critical for high-power charging and in cases in which many EVs are concentrated in a specific location, such as clusters of residential LDV charging and possibly fleet depots for commercial vehicles (Muratori 2018).

This paper provides a timely status of the literature on several aspects of EV markets, technologies, and future projections. The paper focuses on multiple facets that characterize technology status and the role of EVs in transportation decarbonization and broader energy-transformation pathways focusing on the U.S. context. As appropriate, global context is provided as well. Hybrid EVs (for which liquid fuel is the only source of energy) and fuel cell EVs (that power an electric powertrain with a fuel cell and on-board hydrogen storage) have some similarities with EVs and could complement them for many applications. However, these technologies are not reviewed in detail here. The remainder of this paper is structured as follows. Section 2 focuses on the status of the light-duty-EV market and provides a comparison of projections for future adoption. Section 3 provides insights on market opportunities beyond LDVs. Section 4 offers a review of cost and performance evolution for batteries, power electronics, and electric machines that are key components of EV success. Section 5 reviews charging-infrastructure status and focuses on modeling and analysis studies used to project charging-infrastructure requirements, the economics of public charging, and some considerations on cybersecurity and future technologies (e.g. wireless charging). Section 6 provides an overview of the impact of EV charging on power systems at multiple scales, ranging from bulk power systems to distribution networks. Section 7 provides insights into life-cycle cost and emissions studies focusing on EVs. Finally, section 8 touches on future expectations.

1.1. Summary of take-away points

1.1.1. EV adoption

- The global rate of adoption of light-duty EVs (passenger cars) has increased rapidly since the mid-2010s, supported by three key pillars: improvements in battery technologies; a wide range of supportive policies to reduce emissions; and regulations and standards to promote energy efficiency and reduce petroleum consumption.

- Adoption of advanced technologies has been underestimated historically in modeling and analyses; EV adoption is projected to remain limited until 2030, and high uncertainty is shown afterward with widely different projections from different sources. However, EVs hold great promise to replace conventional LDVs affordably.

- Barriers to EV adoption to date include consumer skepticism toward new technology, high purchase prices, limited range and lack of charging infrastructure, and lack of available models and other supply constraints.

- A major challenge facing both manufacturers and end-users of medium- and heavy-duty EVs is the diverse set of operational requirements and duty cycles that the vehicles encounter in real-world operation.

- EVs appear to be well suited for short-haul trucking applications such as regional and local deliveries. The potential for battery-electric models to work well in long-haul on-road applications has yet to be established, with different studies indicating different opportunities.

1.1.2. Batteries and other EV technologies

- Over the last 10 years, the price of lithium-ion battery packs has dropped by more than 80% (from over $1000 kWh−1 to $156 kWh−1 at the end of 2019, BloombergNEF 2020). Further price reduction is needed to achieve EV purchase-price parity with ICEVs.

- Over the last 10 years, the specific energy of a lithium-ion battery cell has almost doubled, reaching 240 Wh kg−1 (BloombergNEF 2020), reducing battery weight significantly.

- Reducing or eliminating cobalt in lithium-ion batteries is an opportunity to lower costs and reduce reliance on a rare material with controversial supply chains.

- While batteries are playing a key role in the rise of EVs, power electronics and electric motors are also key components of an EV powertrain. Recent trends toward integration promise to deliver benefits in terms of increased power density, lower losses, and lower costs.

1.1.3. Charging infrastructure

- With a few million light-duty EVs on the road, currently, there is about one public charge point per ten battery electric vehicles (BEVs) in U.S. (although most vehicles have access to a residential charger).

- Given the importance of home charging (and the added convenience compared to traditional refueling at public stations), charging solutions in residential areas comprising attached or multi-unit dwellings is likely to be essential for EVs to be adopted at large scale.

- Although public charging infrastructure is clearly important to EV purchasers, how best to deploy charging infrastructure in terms of numbers, types, locations, and timing remains an active area for research.

- The economics of public charging vary with location and station configuration and depend critically on equipment and installation costs, incentives, non-fuel revenues, and retail electricity prices, which are heavily dependent on station utilization.

- The electrification of medium- and heavy-duty commercial trucks and buses might introduce unique charging and infrastructure requirements compared to those of light-duty passenger vehicles.

- Wireless charging, specifically high-power wireless charging (beyond level-2 power), could play a key role in providing an automated charging solution for tomorrow's automated vehicles.

1.1.4. Power system integration

- Accommodating EV charging at the bulk power-system level (generation and transmission) is different in each region, but there are no major known technical challenges or risks to support a growing EV fleet, especially in the near term (approximately one decade).

- At the local level, however, EV charging can increase and change electricity loads significantly, causing possible negative impacts on distribution networks, especially for high-power charging.

- The integration of EVs into power systems presents opportunities for synergistic improvement of the efficiency and economics of electromobility and electric power systems, and EVs can support grid planning and operations in several ways.

- There are still many challenges for effective EV-grid integration at large scale, linked not only to the technical aspects of vehicle-grid-integration (VGI) technology but also to societal, economic, business model, security, and regulatory aspects.

- VGI offers many opportunities that justify the efforts required to overcome these challenges. In addition to its services to the power system, VGI offers interesting perspectives for the full exploitation of synergies between EVs and VRE as both technologies promise large-scale deployment in the future.

1.1.5. Life-cycle cost and emissions

- Many factors contribute to variability in EV life-cycle emissions, mostly the carbon intensity of electricity, charging patterns, vehicle characteristics, and even local climate. Grid decarbonization is a prerequisite for EVs to provide major GHG-emissions reductions.

- Existing literature suggests that future EVs can offer 70%–90% lower GHG emissions compared to today's ICEVs, most obviously due to broad expectations for continued grid decarbonization.

- Operational costs of EVs (fuel and maintenance) are typically lower than those of ICEVs, largely because EVs are more efficient than ICEVs and have fewer moving parts.

1.1.6. Synergies with other technologies and future expectations

- Vehicle electrification fits in broader electrification and mobility macro-trends, including micro-mobility in urban areas, new mobility business models regarding ride-hailing and car-sharing, and automation that complement well with EVs.

- While EVs are a relatively new technology and automated vehicles are not readily available to the general public, the implications and potential synergies of these technologies operating in conjunction are significant.

- The coronavirus pandemic is impacting transportation markets negatively, including those for EVs, but long-term prospects remain undiminished.

- Several studies project major roles for EVs in the future, which is reflected in massive investment in vehicle development and commercialization, charging infrastructure, and further technology improvement. Consumer adoption and acceptance and technology progress form a virtuous self-reinforcing circle of technology-component improvements and cost reductions.

- EVs hold great promise to replace ICEVs affordably for a number of on-road applications, eliminating petroleum dependence, improving local air quality and enabling GHG-emissions reductions, and improving driving experiences.

- Forecasting the future, including technology adoption, remains a daunting task. However, this detailed review paints a positive picture for the future of EVs across a number of on-road applications.

2. Status of electric-LDV market and future projections

This section provides a current snapshot of the electric-LDV market in a global and U.S. context, but focuses on the latter. The global rate of adoption of electric LDVs has increased rapidly since the mid-2010s 13 . By the end of 2019, the global EV fleet reached 7.3 million units—up by more than 40% from 2018—with more than 1.25 million electric LDVs in the U.S. market alone (IEA 2020). EV sales totaled more than 2.2 million in 2019, exceeding the record level that was attained in 2018, despite mixed performances in different markets. Electric-LDV sales increased in Europe and stagnated or declined in other major markets, particularly in China (with a significant slowdown due to changes in Chinese subsidy policy in July 2019), Japan, and U.S. U.S. EV adoption varies greatly geographically—nine counties in California currently see EVs accounting for more than 10% of sales (8% on average for California as a whole), but national-level sales remain at less than 3% (Bowermaster 2019). BEV sales exceeded those of plug-in hybrid electric vehicles (PHEVs) in all regions.

The rapid increase in EV adoption is underpinned by three key pillars:

- (a)Improvements and cost reductions in battery technologies, which were enabled initially by the large-scale application of lithium-ion batteries in consumer electronics and smaller vehicles (e.g. scooters, especially in China, IEA 2017). These developments offer clear and growing opportunities for EVs and HEVs to deliver a reduced total cost of ownership (TCO) in comparison with ICEVs.

- (b)A wide range of supportive policy instruments for clean transportation solutions in major global markets (Axsen et al 2020), which are mirrored by private-sector investment. These developments are driven by environmental goals (IPCC 2014), including reduction of local air pollution. These policy instruments support charging-infrastructure deployment (Bedir et al 2018) and provide monetary (e.g. rebates and vehicle-registration discounts) and non-monetary (e.g. access to high-occupancy-vehicle lanes and preferred parking) incentives to support EV adoption (IEA 2018a, AFDC 2020).

- (c)Regulations and standards that support high-efficiency transportation solutions and reduce petroleum consumption (e.g. fuel-economy standards, zero-emission-vehicle mandates, and low-carbon-fuel standards). These regulations are being supported by technology-push measures, consisting primarily of economic instruments (e.g. grants and research funds) that aim to stimulate technological progress (especially batteries), and market-pull measures (e.g. public-procurement programs) that aim to support the deployment of clean-mobility technologies and enable cost reductions due to technology learning, scale, and risk mitigation.

Transport electrification also has started a virtuous self-reinforcing circle. Battery-technology developments and cost reductions triggered by EV adoption provide significant economic-development opportunities for the companies and countries intercepting the battery and EV value chains. Adoption of alternative vehicles both is enabled and constrained by powerful positive feedback arising from scale and learning by doing, research and development, consumer experience and familiarity with technologies (e.g. neighborhood effect), and complementary resources, such as fueling infrastructure (Struben and Sterman 2008). In this context, more diversity in make and model market offerings is supporting vehicle adoption. As of April 2020, there are 50 EV models available commercially in U.S. markets (AFDC 2020), and ∼130 are anticipated by 2023 (Moore and Bullard 2020).

Measures that support transport electrification have been, and increasingly shall be, accompanied by policies that control for the unwanted consequences. Thus, the measures need to be framed in the broader energy and industry contexts.

When looking at the future, EV-adoption forecasts remain highly uncertain. Technology-adoption projections are used by a number of stakeholders to guide investments, inform policy design and requirements (Kavalec et al 2018), assess benefits of previous and ongoing efforts (Stephens et al 2016), and develop long-term multi-sectoral assessments (Popp et al 2010, Kriegler et al 2014). However, projecting the future, including technology adoption, is a daunting task. Past projections often have turned out to be inaccurate. Still, progress has been made to address projection uncertainty (Morgan and Keith 2008, Reed et al 2019) and contextualize scenarios to explore alternative futures in a useful way. Scenario analysis is used largely in the energy-environment community to explore the possible implications of different judgments and assumptions by considering a series of 'what if' experiments (BP 2019).

Adoption of advanced technologies historically has been underestimated in modeling and analysis results (e.g. Creutzig et al 2017), which fail to capture the rapid technological progress and its impact on sales. Historical experiences suggest that technology diffusion, while notoriously difficult to predict, can occur rapidly and with an extensive reach (Mai et al 2018). Projecting personally owned LDV sales is particularly challenging because decisions are made by billions of independent (not necessarily rational) decision-makers valuing different vehicle attributes based on incomplete information (e.g. misinformation and skepticism toward new technologies) and limited financial flexibility.

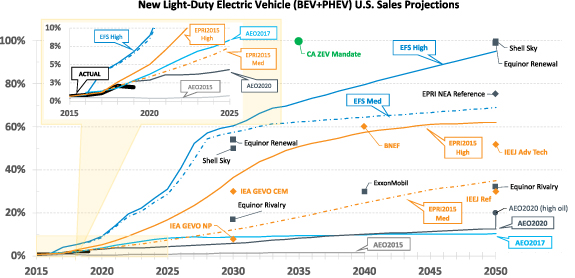

Many studies make projections for future EV sales (see figure 1 for a comparison of different projections). Some organizations (e.g. Energy Information Administration [EIA]) historically have been conservative in projecting EV success, mostly due to scenario constraints and assumptions. Still, U.S. EV-sales projections from EIA in recent years are much higher than in the past. Others (e.g. BloombergNEF and Electric Power Research Institute [EPRI]) consistently have been more optimistic in terms of EV sales and continue to adjust sales projections upward. Policy ambition for EV adoption is also optimistic. For example, in September 2020, California passed new legislation that requires that by 2035 all new car and passenger-truck sales be zero-emission vehicles (and that all medium- and heavy-duty vehicles be zero-emission by 2045) (California, 2020). Projected EV sales and outcomes from major energy companies vary widely, ranging from somewhat limited EV adoption (e.g. ExxonMobil) to full market success (e.g. Shell). A survey from Columbia University (Kah 2019) considers 17 studies and shows that 'EV share of the global passenger vehicle fleet is not projected to be substantial before 2030 given the long lead time in turning over the global automobile fleet' and that 'the range of EVs in the 2040 fleet is 10% to 70%'. The studies compared in figure 1 show an even greater variability for 2050 projections, ranging from 13% to 100% of U.S. EV adoption for LDVs.

Figure 1. Electric LDV (BEV and PHEV) new sales projections from numerous international sources. Unless otherwise noted, data refer to new U.S. sales. AEO2015 = EIA Annual Energy Outlook 2015, Reference Scenario. AEO2017 = EIA Annual Energy Outlook 2017, Reference Scenario. AEO2020 = EIA Annual Energy Outlook 2020, Reference Scenario. AEO2020HO = EIA Annual Energy Outlook 2020, High Oil Scenario. EFS Med = National Renewable Energy Laboratory (NREL) Electrification Futures Study, Medium Scenario. EFS High = NREL Electrification Futures Study, High Scenario. EPRI Med = EPRI Plug-in Electric Vehicle Projections: Scenarios and Impacts, Medium Scenario. EPRI High = EPRI Plug-in Electric Vehicle Projections: Scenarios and Impacts, High Scenario. EPRI NEA = EPRI National Electrification Assessment, Reference Scenario. GEVO NP = IEA Global EV Outlook 2019, New Policies Scenario. GEVO CEM = IEA Global EV Outlook 2019, Clean Energy Ministerial 30@30 Campaign Scenario. BNEF = BloombergNEF EV Outlook 2020. Equinor Riv = Equinor 2019 Energy Perspectives, Rivalry Scenario. Equinor Ren = Equinor 2019 Energy Perspectives, Renewal Scenario. Shell Sky = Shell Sky Scenario. ExxonMobil = 2019 ExxonMobil Outlook for Energy. IEEJ Ref = The Institute of Energy Economics, Japan. 2019 Outlook, Reference Scenario (global sales). IEEJ Adv = The Institute of Energy Economics, Japan. 2019 Outlook, Advanced Technologies Scenario (global sales). CA ZEV Mandate = California zero-emission vehicle (ZEV) Executive Order N-79-20 (September 2020).

Download figure:

Standard image High-resolution imageThe future remains uncertain, but there is a clear trend in projections of light-duty EV sales toward more widespread adoption as the technology improves, consumers become more familiar with the technology, automakers expand their offerings, and policies continue to support the market.

A number of studies analyze the drivers of EV adoption (Vassileva and Campillo 2017, Priessner et al 2018) and highlight several barriers for EVs to achieve widespread success, including consumer skepticism for new technologies (Egbue and Long 2012); uncertainty around environmental benefits (consumers wonder whether EVs actually are green; see section 7 for more clarity on the environmental benefits of EVs) and continued policy support; unclear battery aging/resale value; high costs (Haddadian et al 2015, Rezvani et al 2015, She et al 2017); lack of charging infrastructure (Melaina et al 2017 , Narassimhan and Johnson 2018); range anxiety (the fear of being unable to complete a trip) associated with shorter-range EVs; longer refueling times compared to conventional vehicles (Franke and Krems 2013, Neubauer and Wood 2014; Melaina et al 2017); dismissive and deceptive car dealerships (De Rubens et al 2018); and other EV-supply considerations, such as limited model availability and limited supply chains.

A recent review of 239 articles published in top-tier journals focusing on EV adoption draws attention to 'relatively neglected topics such as dealership experience, charging infrastructure resilience, and marketing strategies as well as identifies much-studied topics such as charging infrastructure development, TCO, and purchase-based incentive policies' (Kumar and Alok 2019). Similar reviews published recently focus on different considerations, such as market heterogeneity (Lee et al 2019a), incentives and policies (Hardman 2019, Tal et al 2020), and TCO (Hamza et al 2020). Other than some limited discussions on business models and TCO, the literature is focused on one side of the story, namely demand. However, the availability (makes and models) of EVs is extremely limited compared to ICEVs (AFDC 2020). This is justified, in part, by new technologies requiring time to be introduced, and, in part, by the higher manufacturer revenues associated with selling and providing maintenance for ICEVs. Moreover, slow turnover in legacy industry (Morris 2020) and other supply constraints can be a major barrier to widespread EV uptake (Wolinetz and Axsen 2017, De Rubens et al 2018). Kurani (2020) argues that in most cases, 'Results of large sample surveys and small sample workshops mutually reinforce the argument that continued growth of PEV markets faces a barrier in the form of the inattention to plug-in electric vehicles (PEVs) of the vast majority of car-owning and new-car-buying households even in a place widely regarded as a leader. Most car-owning households are not paying attention to PEVs or the idea of a transition to electric-drive.'

3. EVs beyond light-duty applications

While much of the recent focus on vehicle electrification is with LDVs and small two- or three-wheelers (primarily in China), major progress also is being made with the electrification of medium- and heavy-duty vehicles. This includes heavy-duty trucks of various types, urban transit buses, school buses, and medium-duty vocational vehicles. As of the end of 2019, there were about 700 000 medium- and heavy-duty commercial EVs in use around the world (EV Volumes 2020, IEA 2020).

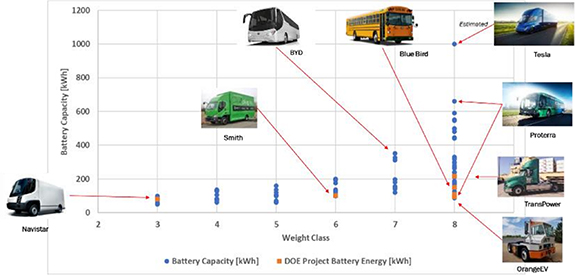

A major challenge facing both manufacturers and end-users of medium- and heavy-duty vehicles is the diverse set of operational requirements and duty cycles that the vehicles encounter in real-world operation. When designing powertrain configurations and on-board energy-storage needs for new technologies, it is of critical importance to represent vehicle behavior accurately for different operations, including possible changes triggered by electrification (Delgado-Neira 2012). Medium- and heavy-duty vehicles can require a large number of powertrain and battery configurations, control strategies, and charging solutions. These needs depend on vehicle type (covering the full U.S. gross vehicle weight ratings [GVWR] spectrum from class 3 to class 8, 10 001–80 000 lb [4536–36 287 kg]), commercial operational situations and activities, and diverse drive cycles and charging opportunities (e.g. depot-based operations vs. long-haul). An example of this potential variability and its effect on the required battery capacity across multiple vehicle vocations is shown in figure 2 (Smith et al 2019).

Figure 2. Battery capacity requirements vs. weight class for medium- and heavy-duty vehicles (Smith et al 2019).

Download figure:

Standard image High-resolution imageAnother example of the highly variable use cases for medium- and heavy-duty EVs shows energy efficiencies range between 0.8 kWh mile−1 and 3.2 kWh mile−1 (0.5–2.5 kWh km−1) (Gao et al 2018). If the on-board energy-storage needs for these vehicles are considered, assuming a daily operational range of between 50 miles and 200 miles (80–322 km), this results in battery-size requirements between 40 kWh and 640 kWh (assuming that the vehicle is recharged once daily). If additional charging strategies are considered (with their variability in expected charge times and associated power ratings), the range of vehicle-hardware and charging-infrastructure possibilities increases further. When adding variability across use cases with respect to temperature effects, battery-capacity degradation, payload, and road grade, it becomes clear that medium- and heavy-duty truck manufacturers face a significant challenge in designing, developing, and manufacturing systems that are able to meet the diverse operational requirements.

There are potential synergies between components of light-duty and medium- and heavy-duty electric vehicles. However, the requirements of medium- and heavy-duty vehicles place much greater burdens on powertrain components. The power and energy needs in heavy-duty applications are much larger than in light-duty applications. Heavy-duty vehicles could demand twice the peak power, four times the torque, and can consume more than five times the energy per mile (or km) driven compared to LDVs. In addition to using more energy per mile (or km) driven, typically, commercial vehicles drive many more miles (or km) per day, requiring much larger batteries and possibly much higher-power charging. Moreover, heavy-duty-vehicle users expect their vehicles to last more than a million miles, pointing to significantly higher durability requirements for heavy-duty-vehicle components (Smith et al 2019). Overall, these requirements, in combination with the needs for very high durability and very high-power drivelines and charging, may cause battery chemistries of heavy-duty vehicle batteries to diverge from those that are used in LDVs, hindering economies of scale. Demands for high efficiency, high power, and lower weight will put pressure on commercial vehicles to work at higher voltages than LDVs do. While LDVs are designed typically with powertrains that operate at a few hundred volts, it may be desirable to design large EVs with kilovolt powertrains. This will have a particularly significant impact on power electronics and could drive the development of wide-bandgap power electronics.

Historically, EVs have not been considered capable alternatives to heavy-duty diesel trucks (above 33 000 lb [14 969 kg] GVWR) due to high capital costs, high energy and power requirements, and weight and range-related battery constraints. International Council on Clean Transportation (ICCT), for example, suggests that while conventional EV-charging methods may be sufficient for small urban commercial vehicles, overhead catenary or in-road charging are required for heavier vehicles (Moultak et al 2017). Recent studies dispute this, anticipating a much greater opportunity for EVs to replace diesel trucks in the short-term, even for long-haul applications (Mai et al 2018, McCall and Phadke 2019, Borlaug et al Forthcoming), but the potential for battery-electric models to work well in long-haul applications has yet to be established (NACFE 2018). Studies show that a significant amount of payload capacity will be consumed by batteries, potentially up to 7 tons or 28% of capacity in a truck with a 500 mile (805 km) range with 1100 kWh battery capacity (Burke and Fulton 2019). Thus, batteries would reduce significantly the amount of cargo that can be carried. Other studies suggest this could be much less―on the order of 4% of lost payload capacity for 500 mile range (805 km) trucks and with overall lower TCO than diesel trucks (Phadke et al 2019). For short-haul applications, such as port drayage and regional or local deliveries, EVs appear well suited and battery weight may not affect the cargo or payload capacity adversely. Several heavy-duty battery-electric trucks for short- and medium-haul applications have been developed and tested in recent years by Balqon, Daimler Trucks NA, Peterbilt, TransPower, Tesla, US Hybrid, Volvo, and others (AFDC 2020).

Urban buses are also a major emerging market for electrification. In California, Innovative Clean Transit rules require transit agencies to transition completely to zero-emission technologies (batteries or fuel cells), with all new bus purchases being zero-emission by 2029 (CARB 2018). Eight of the ten largest transit agencies in California already are adopting zero-emission technologies into their fleets (CARB 2018). In a comparative study of urban buses running on diesel, compressed natural gas, diesel hybrid, fuel cells, and batteries, the battery buses are estimated to have the lowest CO2 emissions in both California and Finland bus duty cycles at the time of the study (Lajunen and Lipman 2016). This study also shows that battery buses have only slightly higher overall costs per mile (or km) than fossil-fuel-based alternatives. Future projections out to 2030 show that electric buses have the lowest overall life-cycle costs, especially when CO2 costs are included (Lajunen and Lipman 2016).

Medium-duty delivery vehicles (typically 10 000–33 000 lb [4536–14 969 kg] GVWR) are another attractive emerging area for electrification. The goods-delivery market is growing at approximately 9% per year in recent years, with a projected $343 billion global industry value in 2020 (Accenture 2015). The 'last mile' delivery vehicles that are needed for this market are undergoing changes and present good opportunities for electrification. Amazon, for example, has announced plans to purchase 100 000 custom-designed Rivian electric delivery vans by 2030, with 10 000 of the vehicles delivered by late 2022 (Davies 2019).

A significant challenge with electrifying these heavy- and medium-duty vehicles revolves around the installation of the required charging infrastructure (either at depots or along highways). While LDVs typically charge at power levels of 3 kW–10 kW, and potentially 50 kW–250 kW with DC fast chargers (DCFCs), a heavy-duty vehicle may require higher-power charging, depending on its duty cycle. Fleets of these vehicles charging in one location, such as a truck depot or travel center, may require several megawatts of power. This requires expensive charging infrastructure, potentially including costly and time-consuming distribution-grid upgrades, to provide the higher voltage and current levels that are needed. For example, a single 350 kW DCFC that may be suitable for heavy-duty applications costs almost $150 000 today (Nelder and Rogers 2019, Nicholas 2019). These costs would, in turn, impact the business case for vehicle electrification. Potential costs of grid upgrades to support these new electrical loads would be additional expenses that may or may not be supported by the local utility, depending on the circumstances. To enable reliable, low-cost charging, which is crucial when considering the TCO for a fleet owner, the installation and operational costs of the charging infrastructure must be optimized, requiring engagement with power-supply stakeholders.

4. Batteries, power electronics, and electric machines

Electrification is a key aspect of modern life, and electric motors and machines are prevalent in manufacturing, consumer electronics, robotics, and EVs (Zhu and Howe 2007). One reason for the recent success and rise in adoption of EVs is the use of advanced lithium-ion batteries with improved performance, life, and lower cost. Improved energy and power performance, increased cycle and calendar life, and lower costs are leading to EVs with longer electric range and better acceleration at lower cost premia that are attracting consumers. This section summarizes the state-of-the-art for batteries and for power electronics, electric machines, and electric traction drives in terms of cost, performance, power and energy density, and reliability, and highlights some research challenges, pathways, and targets for the future.

4.1. Batteries

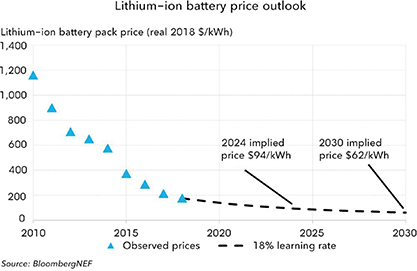

Over the last 10 years, the price of a lithium-ion battery pack has dropped by almost 90% from over $1000 kWh−1 in 2010 to $156 kWh−1 at the end of 2019 (BloombergNEF 2020). Meanwhile, the specific energy of a lithium-ion battery cell has almost doubled from 140 Wh kg−1 to 240 Wh kg−1 during that same window of time (BloombergNEF 2020). The improvement in performance and cost comes mainly from engineering improvements, use of materials with higher capacities and voltages, and development of methods to increase stability for longer life and improved safety. Improvements in cell, module, and pack design also help to improve performance and lower costs. Increases in manufacturing volume due to EV sales contribute significantly to cost reductions (Nykvist and Nilsson 2015, Nykvist et al 2019). However, further reductions in battery costs, along with a reduction in the cost of electric machines and power electronics, are needed for EVs to achieve purchase-price parity with ICEVs. This parity is estimated by U.S. Department of Energy (DOE) to be achieved at battery costs of ∼$100 kWh−1 (preferably less than $80 kWh−1 ) (VTO, 2020). At that point, EVs should have both a purchase- and a lifetime-operating-cost benefit over ICEVs. Such cost benefits are likely to trigger drastic increases in EV sales. Figure 3 shows the observed price of lithium-ion battery packs from 2010 to 2018, as well as estimated prices through 2030. BloombergNEF projects that by 2024 the price for original equipment manufacturers (OEMs) to acquire battery packs will go below $100 kWh−1 and reach ∼$60 kWh−1 by 2030 if high levels of investments continue in the future (BloombergNEF 2020).

Figure 3. Evolution of battery prices over the last 10 years and future projections (Goldie-Scot 2019). BloombergNEF 2019.

Download figure:

Standard image High-resolution imageThe typical anode material that is used in most lithium-ion EV batteries is graphite (Ahmed et al 2017). Research is underway to utilize silicon, in addition to graphite, due to its higher specific-energy capacity. For cathodes, there is more variety (Lee et al 2019, Manthiram 2020). Consumer electronics such as mobile phones and computers almost exclusively have used lithium cobalt oxide, LiCoO2, due to its high specific-energy density (Keyser et al 2017). Most EV manufacturers (except Tesla) have avoided using LiCoO2 in EVs due to its high cost and safety concerns. Lithium iron phosphate also has been used for electric cars and buses because of its long life and better safety and power capabilities. However, due to its low specific-energy density (110 Wh kg−1) when paired with a graphite anode, lithium iron phosphate is not used commonly for light-duty EVs in U.S. In recent years, battery makers and vehicle OEMs have moved to lithium nickel manganese cobalt oxides (NMC) with varying ratios of the three transition metals. Initially, OEMs used NMC111 (the numbers represent the molar fractions of nickel, manganese, and cobalt, which are equal in this case), but they have transitioned to NMC532 and utilize NMC622 now while working to stabilize the NMC811 cathode structure. The goal is eventually to reduce the amount of cobalt in the cathode to less than 5% and perhaps even eliminate the use of cobalt. The use of these cathodes with higher specific-energy density and less cobalt leads to lower battery cost per unit energy ($ kWh−1). Table 1 shows the specific energy and estimated (bottom-up) cost from Argonne National Laboratory's BatPaC Battery Performance and Cost model (Ahmed et al 2016) based on large-volume material processing, cell manufacturing, and pack manufacturing.

Table 1. Calculated specific energy and cost of advanced lithium-ion batteries with different cathode/anode chemistries. Numbers are from BatPaC (Ahmed et al 2016) and are intended for relative comparison only. Final values can change depending on the components used and production volume, and costs reported do not reflect what a negotiated price could be between a battery and EV maker.

| Type of chemistry | Specific energy | Specific energy | Estimated cost | |

|---|---|---|---|---|

| (cathode/anode) | (cells) Wh kg−1 | (pack) Wh kg−1 | (pack) $ kWh−1 | |

| Current | LCO/Gr | 224.1 | 181.8 | 250 |

| NMC111/Gr | 204.9 | 167.6 | 145 | |

| NMC622/G | 224.1 | 181.7 | 135 | |

| NMC811/Gr | 241.3 | 194.2 | 120 | |

| NCA/Gr | 230.4 | 186.4 | 130 | |

| Future | High Voltage NMC622/Gr | 231.4 | 186.5 | 125 |

| High Voltage NMC622/Si | 294.8 | 235.3 | 110 | |

| High Voltage NMC/Li Metal | 332.4 | 259.3 | 120 | |

| Lithium–Sulfur | 346.2 | 257.3 | 95 |

The cost of batteries is expected to decline in the future due to improved capacity of materials (such as Si anodes), increased percentage of active material components, use of lower-cost elements (no cobalt), improved packaging, and continued automation to increase yield while leading to a longer electric range. However, price increases for certain metals such as Ni and Li could prevent achieving those lower-battery-cost projections. Moreover, different battery chemistries can lead to very different costs and specific energies. For example, table 1 shows results obtained from bottom-up calculations with Argonne National Laboratory's BatPaC Battery Performance and Cost Model (Ahmed et al 2016), for a 100 kWh battery pack showing great variability in battery cost and performance for different chemistries.

Opportunities to improve performance and reduce costs further are being pursued in a number of major research areas. The battery community is investigating a number of materials, with the aim of reducing the cost and increasing the energy density of battery systems (Deign and Pyper 2018). Future work will involve utilizing silicon (Salah et al 2019) or lithium metal (Zhang et al 2020) as the anode while utilizing high-energy cathodes, such as NMC811 or lithium sulfur (Zhu et al 2019). Reducing the amount of critical material in lithium-ion batteries, especially cobalt, is an opportunity to lower the cost of batteries and improve supply-chain resilience. The private and public sectors are working toward developing new cathode materials along these lines (Li et al 2009, 2017b). Research and development (R&D) projects are underway to develop infrastructure and recycling technologies to collect batteries and recover the key battery materials economically and environmentally (Harper et al 2019). Reuse of end-of-life batteries from EVs would delay the need for additional battery materials, which should have positive environmental benefits (Neubauer et al 2012). Different battery technologies also are being explored. To increase energy density, reduce cost, and improve safety, the battery community is pursuing development of solid-state batteries with solid-state electrolytes (Randau et al 2020) that have ionic conductivities approaching those of today's liquid electrolyte systems. Solid-state lithium batteries enable the use of metallic lithium anodes, together with solid electrolytes and high-energy cathodes (such as high-nickel NMC or sulfur). Lithium-metal batteries based on solid electrolytes can, in principle, alleviate the safety concerns with current lithium-ion batteries with a flammable organic electrolyte. The main challenges facing lithium-metal anodes are dendritic growth, especially at low temperatures and higher current rates. Dendritic growth could lead to short circuit and thermal runaway and low Coulombic efficiency leading to poor cycle life (Xia et al 2019). Slow ion transport through the solid-state electrolyte leading to low power densities and manufacturing challenges, including poor mechanical integrity, pose additional challenges. Significant R&D activities are focused on developing solid-state electrolytes that prevent dendrite growth, have high ionic conductivity, good voltage-stability windows, and low impedance at the electrode–electrolyte interface. Recent cathode formulations in Li-S cells overcome the polysulfide problem, which could lead to lower efficiency and cycle life. Nevertheless, the deployment of cells with lower electrolyte-to-sulfur ratios for scale-up to large sizes is a remaining challenge. It may take another 5 to 10 years to mass-produce solid-state lithium batteries for EV applications.

As is discussed in section 5, a network of fast chargers and batteries that can handle high charging-power rates is needed to address any potential barriers to widespread EV adoption. Research is focusing on developing batteries that can be charged very quickly (e.g. 80% of capacity in less than 15 min). A number of challenges to high-power charging, such as lithium plating, thermal management, and poor cycle life, need to be addressed (Ahmed et al 2017; DOE 2017, Michelbacher et al 2017). Significant efforts also have focused on developing electrochemical and thermal modeling of batteries for EV applications (Kim et al 2011, Chen et al 2016, Keyser et al 2017, Zhang et al 2017) to improve battery lifetime and efficiency in real-world applications. These efforts include lifetime-estimation and degradation modeling under different real-world climate and driving conditions (Hoke et al 2014, Neubauer and Wood 2014, Liu et al 2017b, Harlow et al 2019, Li et al 2019); simplified models for control and diagnostics (e.g. state-of-charge estimation) (Muratori et al 2010, Fan et al 2013, Cordoba-Arenas et al 2015, Bartlett et al 2016); and developing effective thermal management and control strategies (Pesaran 2001, Serrao et al 2011).

Besides EV applications, batteries can offer energy-storage solutions for hybrid- or distributed-energy systems. These solutions include the use of batteries in integrated configurations with wind or solar photovoltaic (PV) systems or with EV fast-charging stations (Bernal-Agustín and Dufo-Lopez 2009, Badwawi et al 2015, Muratori et al 2019a). Batteries also can provide stabilization and flexibility and can improve resilience and efficiency for power systems in general, especially for critical services or when a high share of variable power generation (e.g. from solar or wind) is expected (Divya and Østergaard 2009, Denholm et al 2013; De Sisternes et al 2016). Lithium-ion batteries that have been developed for EV applications have found their way into stationary applications (Pellow et al 2020) because of their lower cost and modularity compared to other energy-storage technologies (Chen et al 2020). Moreover, EV batteries can be reused or repurposed at the end of their 'vehicle life' (usually considered when energy storage capacity drops below 70%–80% of the original nominal value, (Podias et al 2018)) for stationary applications, improving their economic and environmental performance (Assuncao et al 2016, Ahmadi et al 2017, Martinez-Laserna et al 2018, Olsson et al 2018, Kamath et al 2020).

4.2. Power electronics, electric machines, and electric-traction-drive systems

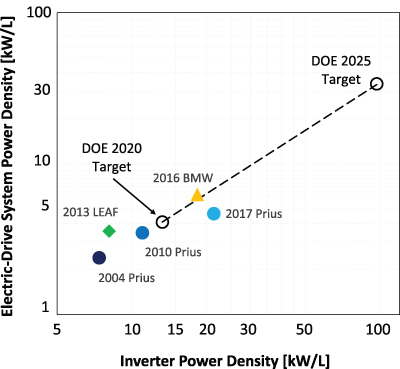

While batteries are playing a key role in the rise of EVs, power electronics and electric motors and machines are also key components of an EV powertrain. Traditionally, the motor and power electronics drive were separate components in an EV. However, recent trends toward integration promise to deliver benefits in terms of increased power density, lower losses, and lower costs compared with separate motor and motor-drive solutions (Reimers et al 2019). Figure 4 shows the 2020 power density for power electronics, electric machines, and electric-traction-drive system from some example commercial vehicles as well as the 2025 DOE and U.S. DRIVE Partnership targets for near-term improvements (U.S. DRIVE 2017, Chowdhury et al 2019). Commercially available vehicles exceed the 2020 power-density target. However, the 2025 target is at least a factor of six to eight higher than current commercial baselines. U.S. DRIVE Partnership also proposes electric-traction-drive-cost targets for 2020 and 2025: $8 kW−1 and $6 kW−1, respectively, both of which are challenging targets (U.S. DRIVE 2017, Chowdhury et al 2019). The authors are not aware of commercial systems meeting the 2020 target, and the 2025 target represents a further 33% reduction.

Figure 4. Integrated electric-drive system and inverter power density for several commercial light-duty vehicles and DOE targets (data from U.S. DRIVE 2017, Chowdhury et al 2019).

Download figure:

Standard image High-resolution imageImprovements in compact power electronics and electric machines are applicable to novel emerging wheel-integrated solutions as well (Iizuka and Akatsu 2017, Fukuda and Akatsu 2019). The development of advanced electric traction drive with improved efficiency is a strategy for increasing the range of electric-drive vehicles. In addition to this, chassis light-weighting is another strategy that is being pursued by the industry and the research community for increasing EV driving ranges. There are several technical challenges in meeting the DOE power-density targets (shown in figure 4). Challenges in meeting related DOE cost targets remain as well. A range of integration approaches are proposed in the literature, including surface mounting the power electronics on the motor housing (Nakada, Ishikawa, and Oki 2014), mounting on the motor stator iron (Wheeler et al 2005), and piecewise integration. Piecewise integration involves modularizing both power modules and machine stators into smaller units (Brown et al 2007). In all cases, the close physical positioning of the power electronics relative to the machine and the associated harsh thermal environment necessitate new concepts related to the active cooling of both components. A first strategy may be to isolate the power electronics from the machine thermally using parallel cooling mechanisms (Wheeler et al 2005). Another approach may be to use a fully integrated, series-connected, active-cooling loop (Tenconi et al 2008, Gurpinar et al 2018). In either case, cost benefits may be realized through the possible elimination or combination of cooling loops. Significant research also has been focused on reducing rare-earth and heavy-rare-earth materials within the electric machines because that is an additional important pathway to reduce costs (U.S. DRIVE 2017).

Higher levels of integration go hand-in-hand with the utilization of wide-bandgap (WBG) semiconductor devices, which may be used at higher operational temperatures (e.g. >200 °C versus 150 °C for silicon) with reduced switching loss (Millán et al 2014). However, the adoption of WBG devices requires new packaging technologies to support the end goals of high temperature, high frequency, higher voltages, and more compact footprints. High-performance electrical interconnects (Cheng et al 2013), die-attach (Liu et al 2020), encapsulation (Cao et al 2010), and power-module-substrate technologies (Stockmeier et al 2011), along with thermal management and reliability of these technologies (Moreno et al 2014, Paret et al 2016, 2019), are critical aspects to consider. The new materials, devices, and components must be cost-effective and high-temperature-capable to be compatible with WBG devices. The downsizing of passive electrical components is another added benefit of adopting WBG devices and a further necessity for integrated machine-drive packaging solutions. Fortunately, the higher switching frequencies that are supported by WBG devices enable the downsizing of both the inductors and capacitors found in a traditional power-control unit (Hamada et al 2015). The development of economically viable and high-temperature-capable passives, capacitors in particular (Caliari et al 2013), is an area of great interest.

Besides EV applications, power electronics and electric machines with low cost, high performance, and high reliability are important for numerous energy-efficiency and renewable-energy applications, such as solar inverters, generators and electric drives for wind, grid-tied medium-voltage power electronics, and sensors and electronics for high-temperature geothermal applications (PowerAmerica 2020).

5. Charging infrastructure

Infrastructure planning and deploying an ecosystem of cost-effective and convenient public and private chargers is central to supporting EV adoption (CEM 2020). The lack of a sufficient refueling infrastructure has hampered many past efforts to promote alternatives to petroleum fuels (McNutt and Rodgers 2004). Extensive research is being done to address the diverse challenges that are posed by a transition from fossil-fuelled ICEVs to EVs and the special role of charging infrastructure in this transition (Muratori et al 2020b).

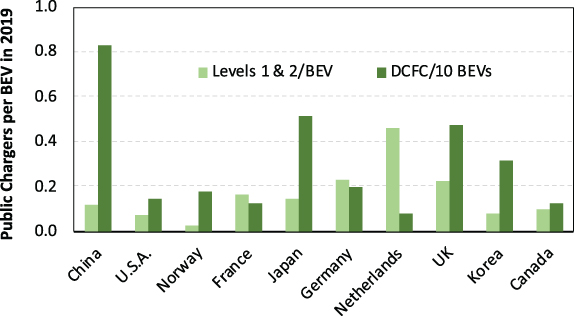

At the end of 2019, there were an estimated 7.3 million EV chargers (or plugs) worldwide, of which almost 0.9 million were public, including approximately 264 000 public DCFCs (81% in China) (IEA 2020). Significant government support and private investments are helping to expand the network of public charging stations worldwide. With about 7.2 million light-duty BEVs on the road, there is about one public charger per 10 light-duty BEVs, and most vehicles have access to a residential charger. However, the number of public chargers per BEV varies widely among the 10 countries with the most BEVs (figure 5) because of different strategies for deploying fast versus slow public chargers. In addition to these LDV chargers, IEA estimated there are 184 000 fast chargers dedicated to electric buses (95% in China).

Figure 5. Public charging availability by country in 2019, measured as Level-1 and Level-2 chargers per BEV and DCFC per 10 BEVs (Data from IEA 2020).

Download figure:

Standard image High-resolution imageStudies show consistently that today's EVs do the majority (50%–80%) of their charging at home, followed by at work (15%–25% when workers use their vehicles to commute), and using public chargers (only about 5% of charging) (Hardman et al 2018). PHEVs conduct more charging at home than BEVs do, and they rely more on level-1 charging (Tal et al 2019). While single-household detached residences readily can accommodate level-1 or -2 charging, multi-unit dwellings require curbside public charging or installations in shared parking facilities (Hall and Lutsey 2017). Historical data on the charging behavior of California BEV owners reveals that 11% of their charging sessions were at level 1, 72% were at level 2, and 17% used DCFCs (Tal et al 2019). Use of DCFCs is lowest for BEVs with less than 100 miles (161 km) of range, highest for medium-range BEVs, and lower again for BEVs with ranges of 300 miles (483 km) or more.

5.1. Charging-siting modeling

Public charging infrastructure is clearly important to EV purchasers and supports EV sales by adding value (Narassimhan and Johnson 2018, Greene et al 2020). However, how best to deploy charging infrastructure, in terms of numbers, types, locations, and timing remains an active area for research (Ko et al 2017, Funke et al 2019 provide reviews). The literature includes many examples of geographically and temporally detailed models to optimize the location, number, and types of charging stations (e.g. Wood et al 2017, Wu and Sioshansi 2017, Zhao et al 2019). Geographically and temporally detailed data recording the movements of PEVs and their charging behavior are scarce. With few exceptions (e.g. Gnann et al 2018), simulation analyses rely on conventional ICEV databases (e.g. Dong et al 2014, Wood et al 2015, 2018), which do not reflect the changes PEV owners will make to maximize the utility of PEVs.

Given the importance of home charging, access to chargers for on-street parking in residential areas comprising attached or multi-unit dwellings is likely to be essential for PEVs to be adopted at large scale. Grote et al (2019) employ heuristic methods with geographical-information systems to locate curbside chargers in urban areas using a combination of census and parking data. The works of Nie and Ghamami (2013), Ghamami et al (2016), and Wang et al (2019) are examples of the variety of optimization methods that are applied to design DCFC networks to support intercity travel. Despite these examples, applied research is hindered by the scarcity of data on long-distance vehicle travel by PEVs (Eisenmann and Plötz 2019). Jochem et al (2019) estimate that 314 DCFC stations could provide minimum coverage of EU intercity routes with approximately 0.7 charging points per 1000 BEVs. Using a database of simulated U.S. intercity travel, He et al (2019) employ a mixed-integer model to optimize the location and number of DCFCs. They conclude that 250 stations could serve 98% of the long-distance miles of BEVs with ranges of 150 miles (241 km) or greater but only 73% of the long-distance miles of 100 mile range (161 km range) BEVs. Similarly, Wood et al (2017) estimate that 400 DCFC stations are required to cover the U.S. interstate-highway network with a 40 mile (64 km) spacing between stations. Others consider the optimal location of dynamic, wireless charging in combination with stationary charging (Liu and Wang 2017).

Optimization models for locating chargers to support commercial PEV fleets also appear in the literature (Jung et al 2014, Shahraki et al 2015). In the future, if vehicle sharing becomes much more common, the downtime for charging could be an important disadvantage for PEVs. Using an integer model to optimize station allocation and PEV assignment, Roni et al (2019) find that charging time represents 72%–75% of vehicle downtime but that charging time could be reduced by almost 50% by optimal deployment of charging stations.

5.2. Beyond LDV charging

The electrification of medium- and heavy-duty commercial trucks and buses introduces unique charging and infrastructure requirements compared to those of LDVs. These requirements stem from the significantly higher battery capacities required on-board the vehicles, potentially shorter charging-dwell times (due to the in-service time requirements of the vehicles), and the potential of large facility charging loads (due to multiple trucks or buses charging in one location). One challenge is to understand the costs associated with the multitude of charging scenarios for commercial vehicles for current operations as well as future operations. It is expected that on-road freight vehicle miles (or km) traveled will increase by 75% from 2012 to 2045 (McCall and Phadke 2019). This increase may bring about new business models and potentially new charging-infrastructure approaches to meet this demand with electrified trucks. California's Innovative Clean Transit regulation, which will require California transit agencies to adopt zero-emission buses by 2040, is likely to drive large charging-infrastructure investments for buses (CARB 2018).

Today's commercial diesel-powered trucks in small fleets typically are fueled at publicly available on-road fueling stations, while nearly half of trucks in fleets of 10+ vehicles use company-owned facilities (Davis and Boundy 2020). Likewise, commercial EVs are charged primarily in fleet-owned facilities as their daily schedule allows (most often overnight). This depot-charging approach, which enables seamless integration of EVs into fleet logistics, might limit the electrification of some vehicle segments in the long term due to the battery capacity that is needed to satisfy their daily-range requirements (the need to complete their full-day function) and return to the facility to recharge fully 14 . Some studies suggest that long-haul battery-electric trucks are technically feasible and economically compelling (Phadke et al 2019) while others are more skeptical (Held et al 2018). Publicly available, high-power charging or en-route charging infrastructure for commercial vehicles could enable electrification for longer-distance vehicles (by enabling smaller on-board battery-capacity needs), but this scenario has cost challenges. En-route, high-power charging of over 1 MW might be needed to enable 500 miles (805 km) or more of daily driving. Installation of a 20 MW truck-charging station in California (capable of multiple 1.5 MW charge events for heavy-duty freight vehicles) is estimated to cost as much as 15 million USD. McCall and Phadke (2019) estimate that as many as 750 of these stations are needed to electrify the fleet of California Class-8 combination trucks. Charging commercial vehicles at depots requires additional infrastructure costs to install lower-power EV-supply equipment networks (e.g. 50 kW–100 kW) capable of charging multiple vehicles at these lower rates. These depot charging systems also will challenge existing facility electrical systems by adding a significant load that was not planned previously at the facility (Borlaug et al Forthcoming).

5.3. Economics of public charging

PEV-charging economics vary with location and station configuration and depend critically on equipment and installation costs and retail electricity prices, which are dependent on utilization (Muratori et al 2019b, Borlaug et al 2020). In the early stages of market development, when there are relatively few vehicles, future demand is uncertain, and most charging is done at an EV's home base (Nigro and Frades 2015, Madina et al 2016). Public charging stations tend to be lightly used during these initial stages (e.g. INL 2015), which poses a difficult challenge for private investment. Understanding and quantifying the value of public charging is hindered by lack of experience with PEVs on the part of consumers (Ito et al 2013, Greene et al 2020, Miele et al 2020) and the complexity of network effects in the evolution of alternative-fuel-vehicle markets (Li et al 2017a). Nevertheless, it is likely that DCFCs will be profitable with sufficient demand. Considering vehicle ranges of between 100 km and 300 km and charging-power levels of between 50 kW and 150 kW, Gnann et al (2018) conclude that charger-usage fees could be between 0.05 € kWh−1 and 0.15 € kWh−1 in addition to the cost of electricity. The estimates were based on simulations with average daily occupancy of charging points of 10%–25% and peak-hour utilization of 20%–70%. In their simulations, utilization rates increase with increasing charger power and decrease with increased EV range. For intercity travel along European Union highways, Jochem et al (2019) estimate that a surcharge of 0.05 € kWh−1 of DCFC would make a minimal coverage of 314 stations (with 20 charge plugs each) profitable, even for station capital costs of one million EUR. He et al (2019) optimize DCFC locations along U.S. intercity routes and conclude that providing an adequate nationwide charging network for long-distance travel by 100 mile (161 km) range BEVs is more economical than increasing vehicle range and reducing the number of charging stations. Muratori et al (2019a) consider a set of charging scenarios from real-world data and thousands of U.S. electricity retail rates. They conclude that batteries can be highly effective at mitigating electricity costs associated with demand charges and low station utilization, thereby reducing overall DCFC costs.

Early estimates show that the cost of public DCFC in U.S. can vary widely based on the station characteristics and level of use (Muratori et al 2019a). Numerous new technology options are being explored to provide lower-cost electricity for light-duty passenger and medium- and heavy-duty commercial BEVs. Increasing the range of EVs through higher-power public charging stations as well as accommodating new potential BEV business models, such as transportation-network companies or automated vehicles, are driving new charging-technology solutions. Managed charging solutions that are available today can provide increased value to the BEV owner (lower electricity costs), charging station owner (lower operating costs), or grid operator (lower infrastructure-investment costs). For example, a managed-charging solution has been adopted and is currently in operation at a Santa Clara Valley Transportation Authority depot to charge a fleet of Proterra electric buses optimally to ensure minimal stress on the grid (Ross 2018).

5.4. Emerging charging technologies

Wireless charging, specifically high-power wireless charging (beyond level-2 power levels), could play a key role in providing an automated charging solution for tomorrow's automated vehicles (Lukic and Pantic 2013, Qiu et al 2013, Miller et al 2015, Feng et al 2020). Wireless charging also can enable significant electric range for BEVs by providing en-route opportunity charging (static or dynamic charging opportunities). If a network of wireless charging options is available to provide convenient and fast en-route charging, it could help reduce the amount of battery that is needed on-board a vehicle and reduce the cost of ownership for a BEV owner. Wireless charging is being developed for power levels of up to 300 kW for LDVs, 500 kW for medium-duty vehicles, and 1000 kW for heavy-duty vehicles. Bidirectional functionality, improved efficiency, interoperability of different systems, improved cybersecurity, and increased human-safety factors continue to be developed (Ozpineci et al 2019).

Connectivity and communication advances will enable new BEV-charging infrastructure and managed charging solutions. However, emerging cybersecurity threats also are being identified and should be addressed. There are concerns associated with data exchange, communications network, infrastructure, and firmware/software elements of the EV infrastructure (Chaudhry and Bohn 2012), and new charging-system security requirements and protocols are being developed to address these concerns (ElaadNL 2017). New emulation and simulation platforms also are being developed to address these threats and help understand the consequences and value of mitigating cyberattacks that could affect BEVs, electric-vehicle-supply equipment, or the electric grid (Sanghvi et al 2020).

6. Vehicle-grid integration (VGI)

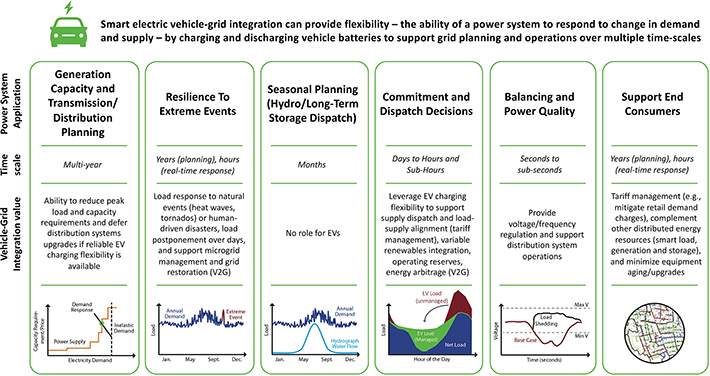

Connecting millions of EVs to the power system, as may occur in the coming decades in major cities, regions, and countries around the world, introduces two fundamental themes: (a) challenges to meet reliably overall energy and power requirements, considering temporal load variations, and (b) VGI opportunities that leverage flexible vehicle charging ('smart charging') or V2G services to provide power-system services from connected vehicles. Multiple studies, which are reviewed in detail below, investigate the potential load growth, impact on load shapes, and infrastructure implications of increased EV adoption. These works focus especially on impact on distribution systems and opportunities for flexible charging to reshape aggregate power loads. Mai et al (2018), for example, shows that in a high-electrification scenario, transportation might grow from the current 0.2% to 23% of total U.S. electricity demand by 2050. This growth would impact system peak load and related capacity costs significantly if not controlled properly. In-depth analytics indicate a complex decision framework that requires critical understanding of potential future mobility demands and business models (e.g. ride-hailing, vehicle sharing, and mobility as a service), technology evolution, electricity-market and retail-tariff design, infrastructure planning (including charging), and policy and regulatory design (Codani et al 2016, Eid et al 2016, Knezovic et al 2017, Borne et al 2018, Hoarau and Perez 2019, Gomes et al 2020, Muratori and Mai 2020, Thompson and Perez 2020).

While accommodating EV charging at the bulk-power (generation and transmission) level will be different in each region, no major technical challenges or risks have been identified to support a growing EV fleet, especially in the near term (FleetCarma 2019, U.S. DRIVE 2019, Doluweera et al 2020). At the same time, many studies show that smart charging and V2G create opportunities to reduce system costs and facilitate VRE integration (Sioshansi and Denholm 2010, Weiller and Sioshansi 2014, IRENA 2019, Zhang et al 2019). Therefore, charging infrastructure that enables smart charging (e.g. widespread residential and workplace charging) and alignment with VRE generation and business models and programs to compensate EV owners for providing charging flexibility are critical elements for successful integration of EVs with bulk power systems.

6.1. Impact of EV loads on distribution systems

At the local level, EV charging can increase and change electricity loads significantly, having possible negative impacts on distribution networks (e.g. cables and distribution transformers) and power quality or reliability (Khalid et al 2019). Residential EV charging represents a significant increase in household electricity consumption that can require upgrades of the household electrical system which, unless managed properly, may exceed the maximum power that can be supported by distribution systems, especially for legacy infrastructure and during times of high electricity utilization (e.g. peak hours and extreme days) (IEA 2018b). The impact of EVs on distribution systems also is influenced by the simultaneous adoption of other distributed energy resources, e.g. rooftop PV panels. While this interdependency complicates assessing the impact of EV charging, Fachrizal et al (2020) show that the two technologies support one other. Similarly, Vopava et al (2020) show that line overloads caused by rooftop PV panels can be reduced (but not avoided) by increasing EV adoption and vice versa.

The impact of EV charging on distribution systems is particularly critical for high-power charging and in cases in which many EVs are concentrated in specific locations, such as clusters of residential LDV charging and possibly fleet depots for commercial vehicles (Saarenpää et al 2013, Liu et al 2017a, Muratori 2018). Smart charging, by which EV charging is timed based on signals from the grid and electricity prices that vary over time, or other forms of control, can help to minimize the impact of EV charging on distribution networks. However, smart charging requires both appropriate business models and signals (with related communication and distributed-control challenges). The market for distribution-system operators to provide such services is not mature yet (Everoze 2018, Crozier, Morstyn, and McCulloch 2020). Time-varying pricing schemes, which are effective at influencing the timing of EV charging (PG&E 2017), typically do not include any distribution-level considerations. Thus, while consumers are responsive to such signals, the business models to include distribution-level metrics still are lacking. Moreover, price signals are offered usually to a large consumer base with the intent of reshaping the overall system load. At the local level, however, multiple consumers responding to the same signal might cause 'rebound peaks' (Li et al 2012, Muratori and Rizzoni 2016) that can overstress distribution systems, calling for coordination among consumers connected to the same distribution network (e.g. direct EV-charging control from an intermediate aggregator).

Charging of larger commercial vehicles and highway fast-charging stations typically involves higher power levels: DCFC is typically at 50 kW/plug today, but power levels are increasing rapidly. Commercial charging locations with multiple plugs co-located at a specific location may lead to possible MW-level loads, which is roughly equivalent to the peak load of a large hotel. Commercial DCFC may require costly upgrades to distribution systems that can impact the cost-effectiveness of public fast charging heavily, especially if stations experience low utilization (Garrett and Nelder 2016, Muratori et al 2019b). While charging timing and speed at commercial stations is less flexible (consumers want to charge and leave or commercial fleets must meet business requirements), business models are often already in place to incentivize curbing maximum peak power from commercial installations. For example, demand charges (a fixed monthly payment that is proportional to the peak power that is drawn during a given month) are fairly common in U.S. retail tariffs and provide a reason to limit peak power. Furthermore, Muratori et al (2019a) show that distributed batteries can be effective at mitigating the cost associated with demand charges by up to 50%, especially for 'peaky' or low-utilization EV-charging loads. Batteries also can facilitate coupling EV-charging stations with local solar electricity production or can provide grid services (Megel, Mathieu, and Andersson 2015), generating additional revenue.

6.2. Value of managed ('smart') EV charging for power systems