Abstract

Background

In Australia and elsewhere, fiscal measures such as alcohol taxation are a commonly used intervention and cost-effective strategy to reduce alcohol consumption and associated harm. However, alcohol taxation policies distort the market for alcohol, specifically increasing the marginal cost of alcohol. It is proposed that a volumetric tax, which taxes alcohol equally across all beverage types, is less distortive of consumer preferences and more efficient at reducing alcohol consumption than the current Australian tax model, where taxes are charged at varying amounts per litre of pure alcohol, depending on the beverage type.

Objective

This paper quantifies the effect of four different alcohol taxation systems, relative to the current Australian system: two different types of volumetric taxation (deadweight loss neutral and tax revenue neutral); the recent strategy trialled in Australia of increasing the tax only on ready-to-drink alcoholic beverages (i.e. premixed spirits); and a tiered tax system, which may be more politically acceptable.

Methods

A partial equilibrium approach was used to measure taxation revenue, consumer welfare and consumption in alcohol markets. Estimates of taxation revenue, consumer welfare and consumption were first calculated for 2008 and then compared with the four scenarios considered.

Results

Relative to the previous alcohol taxation scheme in Australia, the taxation strategy that increased the tax solely on ready-to-drink alcoholic beverages increased taxation revenue by 479 million Australian dollars ($A), reduced pure alcohol consumption by 754000 litres and increased the net deadweight loss of taxation by $A62 million. For a tax-neutral approach, for the same level of taxation revenue as is currently generated, a volumetric tax could substantially reduce the cost of taxation (as described by the net loss in consumer welfare) by $A177 million and reduce pure alcohol consumption by 468 000 litres. Under a deadweight loss-neutral scenario, for the same amount of deadweight loss generated from the previous taxation scenario, taxation revenue could be increased by $A1153 million, in addition to reducing pure alcohol consumption by 4316000 litres. A tiered taxation regime, as modelled here, could decrease pure alcohol consumption by 2 616 000 litres whilst increasing taxation revenue by $A1101 million. However, this scenario would also increase the deadweight loss of taxation by $A113 million.

Conclusion

From these scenarios, it can be shown that, for the same tax revenue, consumer welfare can be reduced or, for the same level of loss to consumer welfare, taxation revenue can be increased. Both these scenarios result in a reduction of pure alcohol consumption.

Similar content being viewed by others

References

Babor T, Caetano R, Casswell S, et al. Alcohol: no ordinary commodity: research and public policy. Oxford: Oxford University Press; 2003

Crombie IK, Irvine L, Elliot L, et al. How do public health policies tackle alcohol-related harm: a review of 12 developed countries. Alcohol Alcohol 2007; 42(5): 492–9

Chisholm D, Rehm J, Van Ommeran M, et al. Reducing the global burden of hazardous alcohol use: a comparative cost-effectiveness analysis. J Stud Alcohol 2004; 65(6): 782–93

Kreitman N. Alcohol consumption and the preventive paradox. Br J Addict 1986; 81(3): 353–63

Wagenaar AC, Salois MJ, Komro KA. Effects of beverage alcohol price and tax levels on drinking: a meta-analysis of 1003 estimates from 112 studies. Addiction 2009; 104(2): 179–90

Preventative Health Taskforce. National preventative health strategy: the road map for action. Canberra: Preventative Health Taskforce, 2009

Freebairn J. Special taxation of alcoholic beverages to correct market failures. Econ Pap 2010; 29(2): 200–14

Ramsey FP. A contribution to the theory of taxation. Econ J 1927; 37: 47–61

Crowley S, Richardson J. Alcohol taxation to reduce the cost of alcohol-induced ill health. Melbourne: Centre for Health Program Evaluation, 1991

Richardson J, Crowley S. Optimum alcohol taxation: balancing consumption and external costs. Health Econ 1994; 3(2): 73–87

Cnossen S. Excise taxation in Australia. In: Melbourne Institute — Australia’s Future Tax and Transfer Policy Conference. University of Melbourne: Melbourne Institute of Applied Economic and Social Research, 2009

Doran CM, Shakeshaft AP. What price for public health? Using taxes to curb drinking in Australia. Lancet 2008; 372: 701–3

Shakeshaft AP, Doran CM, Byrnes J. The role of research in the failure of the alcopops excise in Australia: what have we learned? Med J Aust 2009; 191: 223–5

Doran CM, Hall W, Shakeshaft AP, et al. Alcohol policy reform in Australia: what can we learn from the evidence? Med J Aust 2010; 192: 468–70

The Treasury. Australia’s future tax system: report to the Treasurer. Canberra: Commonwealth of Australia, 2009

Australian Bureau of Statistics. Taxes and household income 2003-04. Canberra: ABS, 2007

Warren N, Harding A, Lloyd R. GST and the changing incidence of Australian Taxes: 1994-95 to 2001-02. eJ Tax Res 2005; 3(1): 114–45

Euromonitor International. Alcoholic drinks in Australia, 2008 [online]. Available from URL: http://www.euromonitor.com/Alcoholic_Drinks_in_Australia [Accessed 2009 Mar 01]

Godfrey C. Factors influencing the consumption of alcohol and tobacco: the use and abuse of economic models. Br J Addict 1989; 84(10): 1123–38

Customs Associates Ltd, 2001. Study on the competition between alcoholic drinks. Stevenage: Customs Associates Ltd, 2001

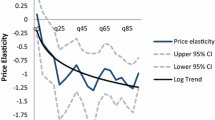

Fogarty J. The nature of the demand for alcohol: understanding elasticity. Br Food J 2006; 108(4): 316–32

Cook PJ, Moore MJ. Chapter 30. Alcohol. In: Anthony JC, Joseph PN, editors. Handbook of health economics. New York: Elsevier, 2000: 1629–73

Gallet CA. The demand for alcohol: a meta-analysis of elasticities. Aust J Agric Resour Econ 2007; 51(2): 121–35

Clements K, Selvanathan S. The economic determinants of alcohol consumption. Aust J Agric Econ 1991; 35(2): 209–31

Senate Standing Committee on Economics. Increase in excise for alcopops/ready-to-drinks (RTDs). Canberra: Australian Federal Government, 2008

Australian Bureau of Statistics. Apparent consumption of alcohol, Australia, 2007-08 [ABS Cat. No. 4307.0.55.001]. Canberra: ABS, 2009

Purshouse RC, Meier PS, Brennan A, et al. Estimated effect of alcohol pricing policies on health and health economic outcomes in England: an epidemiological model. Lancet 2010; 375(9723): 1355–64

Australian Bureau of Statistics. National health survey: summary of results, 2007–2008 (reissue). Canberra: ABS, 2009

Clements KW, Johnson LW. The demand for beer, wine, and spirits: a system wide analysis. J Bus 1983; 56(3): 273–304

Clements KW. Taxation of alcohol in Australia. In: Head JG, editor. Taxation issues of the 1980s. Sydney: Australian Taxation Research Foundation, 1983: 365–84

Srivastava P, Zhao X. What do the bingers drink? Micro-economic evidence on negative externalities and drinker characteristics of alcohol consumption by beverage types. Melbourne: Department of Econometrics and Business Statistics, Monash University, 2010

Wicki M, Kuntsche E, Grichting E. Is alcopop consumption in Switzerland associated with riskier drinking patterns and more alcohol-related problems? Addiction 2006; 101(4): 522–33

McElduff P, Dobson AJ. How much alcohol and how often? Population based case-control study of alcohol consumption and risk of a major coronary event. BMJ 1997; 314(7088): 1159–64

Mukamal KJ, Conigrave KM, Mittleman MA, et al. Roles of drinking pattern and type of alcohol consumed in coronary heart disease in men. N Eng J Med 2003; 348(2): 109–18

Rehm J, Ashley MJ. On the emerging paradigm of drinking patterns and their social and health consequences. Addiction 1996; 91(11): 1615–21

Rehm J, Baliunas D, Borges GLG, et al. The relation between different dimensions of alcohol consumption and burden of disease: an overview. Addiction 2010; 105(5): 817–43

Manning WG, Blumberg L, Moulton LH. The demand for alcohol: the differential response to price. J Health Econ 1995; 14(2): 123–48

Williams J, Chaloupka FJ, Wechsler H. Are there differential effects of price and policy on college students’ drinking intensity? Contemp Econ Policy 2005; 23(1): 78–90

Chaloupka FJ, Wechsler H. Binge drinking in college: the impact of price, availability, and alcohol control policies. Contemp Econ Policy 1996; 14(4): 112–24

Acknowledgements

No sources of funds were used to prepare this research. The authors have no conflicts of interest and have each made a substantial contribution to the work.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Byrnes, J., Petrie, D.J., Doran, C.M. et al. The efficiency of a volumetric alcohol tax in Australia. Appl Health Econ Health Policy 10, 37–49 (2012). https://doi.org/10.2165/11594850-000000000-00000

Published:

Issue Date:

DOI: https://doi.org/10.2165/11594850-000000000-00000