Implications of corporate innovation investment on environment sustainability with moderating role of managerial stock incentives: A case of the oil and gas sector of the United States of America

Honglei Tang

Honglei Tang Zeeshan Rasool

Zeeshan Rasool Muzammal Ilyas Sindhu4*

Muzammal Ilyas Sindhu4* - 1School of Economics and Management, Huzhou University, Huzhou, China

- 2School of Economics and Finance, Messey University, Palmerston North, New Zealand

- 3Department of Management Sciences, MNS UET Multan, Multan, Pakistan

- 4Bahria University, Islamabad, Pakistan

- 5University of South Asia, Lahore, Pakistan

This study examines the impact of corporate innovation investment on environmental sustainability in oil and gas companies in the United States of America. We have compiled the empirical data set of 90 major and renowned companies from 2009 to 2019. To examine the cause-and-effect relationship between the specific factors, we applied the generalized method of movement, and the statistical result reflected a significant and positive relationship between corporate innovation investment and environmental sustainability. This indicates that the positive inclusion of intangible assets leads to motivation in innovation that enhances the context of environmental sustainability. Managerial stock incentives significantly and positively moderate the relationship between corporate innovation investment and environmental sustainability. Enterprises should not only consider their management stock mechanism during the formulation of an innovation strategy but also design the contract according to the innovation level of the enterprise to determine the level of managerial incentives. This study provides insight regarding the significant role of corporate innovation, which establishes a way forward to environmental sustainability.

Introduction

The environmental policy emerged in the last few decades with increase in environmental issues (Yang et al., 2012), leading to more international attention. These issues have globally affected people’s quality of life (Li et al., 2018). Access to worthy natural and technological resources is increasing, leading to waste and environmental pollution. So, in addition to the government, there is a need to involve other stakeholders who should play a wise role in protecting environmentally friendly resources and reducing pollution.

Business and corporate entities need to be involved in remedial measure-related activities other than maximizing shareholder wealth. The environmental protection industry needs to invest more money in buying advanced technology to ensure environmental protection (Arouri et al., 2012). Moreover, environmental protection has no direct economic benefit; therefore, it goes against the principles of economic efficiency. Therefore, when it comes to cost-effectiveness, the business environment is scarce in the initiative (Chang and Hu, 2011), while even in the presence of limitations, there is growing concern about climate change and sustainable development.

Organizations involved in environmentally friendly activities can positively affect their performance (Orlitzky et al., 2003). Environmental protection often leads to better financial performance. It can reduce waste and raw materials, increase productivity and competitiveness, reduce population and community, and even help the standardized future, increasing competition’s value. During scarce availability of environmental resources, businesses and government should invest in the allocation and utilization of innovative ways of environmental protection.

Innovation investment means an investment in managing services. If a corporation invested in an innovation in the past, this means showing consistency in future innovation. The main reason for innovation investment is that modernization is good for past innovation and can offer the benefits of innovation to the economy (Suárez, 2014). As competition in the manufacturing business environment is constantly changing, companies need to manage innovation investments in the long term, thus ensuring competitiveness benefits in a competitive environment (Allen et al., 2005). Innovation has the potential to increase profitability and company sales, which tends to increase for financial support for future innovations (Triguero and Córcoles, 2013).

In the modern world, innovation is characterized by high information asymmetry and adaptability, which generally limits the change process. Policymakers may assume that a specific policy fits all dimensions of a business, but they need to decide how to adjust the rules to fit the size of the business. While regulations may be better suited for larger companies, the government’s initiative to keep customers informed about environmental issues may be straightforward but, in many ways, promotes the environmental development of the economy. This means that environmental laws are necessary to serve a small group of companies.

The diverse nature of corporate ownership leads to firm resource allocation and investment opportunities being significantly different. The nature of ownership does not affect the company’s view of the business and the information of a disclosure environment but always affects the decision-making process. Evidence from the United States and Europe reported that the state’s ownership had been compromised incentives for innovation and were reduced (Verspagen, 2006).

Natural resource-based theory (NRBV) has enlightened the essential innovations to maximize the environmental benefits of environmental management. Its goal is to develop, implement, manage, operate, and monitor the business’s environmental activities. Many studies have found a significant link between environmental sustainability and a firm’s performance (Clarkson et al., 2011; Yang et al., 2011). However, very few research studies have linked corporate innovation and environmental sustainability to the performance of the firm relating environmental innovation. In this sense, this study investigates the mediating role of environmental sustainability in the relationship between corporate innovation investment and a firm’s financial performance. The literature has shown that environmental sustainability is a prerequisite for company performance (Chang, 2011; Liao, 2016).

Grekova et al. (2013) illustrate the mediating role of environmental innovation in environmental management and a firm’s performance. Similarly, environmental studies also show a positive relationship between environmental sustainability and environmental performance (Dowell et al., 2000; Clarkson et al., 2011). Previous literature has attempted to incorporate environmental strategies with increasing environmental impact (such as new product launches, enhancements, and product processes) and environmental improvements (such as reducing pollution and waste costs), making the company aware of its competitive advantage. The natural-resource-based view explained the context of natural resources contributing to sustainable development. These can create a competitive advantage and significantly benefit country-level economies (Wu and Yang, 2021). Environmental innovation and sustainability create a competitive environment for unique, low-cost, and hard-to-mimic companies (Hart and Dowell, 2011). Environmental sustainability shows the goal of achieving environmental strategies that form the basis of innovation (Forsman, 2013). High environmental performance reflects the ability of companies to identify and apply new environmental knowledge to improve product performance and processes (Wu and Yang, 2021).

However, little research has been carried out on the relationship between corporate innovation investment and environmental sustainability. This study addresses the gap and analyzes the impact of corporate innovation investments, such as incremental intangible assets, on their involvement in environmental sustainability, such as the environmental, social, and governance Index.

Literature review

Government and pressure groups worldwide have been promoting the concept of sustainable development for 3 decades. The most important way to improve environmental performance is through environmental innovation, which can describe new or improved technologies, products, processes, or business forms as they reduce or eliminate environmental impacts. Although the concept of sustainable development is well-established, the participation of local companies can be competitive, and there is substantial evidence that they can positively impact their performance.

Business and environmental sustainability

The concept of environmental sustainability is the third aspect of the three most important dimensions. The structure for the sustainable development of literature is based on three pillars, namely, economic, social, and environmental development, which form the basis of the general concept (Goodland, 1995). The principle of social equality or sustainable social equality applies to all members of the society with equal rights to all resources and opportunities. An essential need to define sustainable development is developing a sustainable and equitable environment (Swanso and Zhang, 2012). Sustainability to meet social needs refers to social equality between generations, and it is considered that equality in each generation is greater. Ecological sustainability aims to reduce the size of our ecological footprint (Borim-de-Souza et al., 2015).

Environmental sustainability aims to preserve the natural environment. Illegal spending limits the use of lifeguards by the ability to function properly. Any sector can have a negative impact on the environment, even if it is just to control the lighting in the work environment or be more efficient, such as reducing the generation and emissions of waste in our tax office, which is pollution control and prevention of products. It is assumed that only small businesses everywhere will have a greater impact than large companies. Although previous research has focused on the economic impact on the environment, Musa and Chinniah (2016) consider that the impact of SMEs on the environment is great. However, due to a lack of funding and technical skills, most SMEs cannot measure their environmental impact (Dillard et al.,. 2010). In addition, Musa and Chinniah (2016) warned that many SMEs worldwide do not have sufficient knowledge about environmental management and do not understand the concept of environmental management. As a result, the opportunities for SMEs to participate in socio-environmental activities are very limited.

Most research on financial performance has focused on the importance of financial performance, excluding other company metrics. For modern studies, the effect of financial performance in relation to environmental performance was analyzed. However, the relationship between environmental performance and environmental performance’s environmental, ecological, and environmental impacts has not been well-established. Many companies, including SMEs, are aware of the benefits of following innovation and ecological goals and measuring their performance against these indicators. As a result, eco-innovation reduces costs (for example, energy management), reduces risks (for example, improving security), increases sales and availability benefit (for example, through the use of premium organic products), improves reputation and value, improves attractiveness as an employer, and develops innovative talent (Bigliardiet al. 2012). Bossle et al. (2016) also show that eco-development improves efficiency and competitiveness. Thus, based on the background, the following assumptions are made to specify and direct the concept of performance.

Corporate innovation investment and environmental sustainability

Environmental sustainability reflects the company’s environment through environmental strategies, supported by a strong cognitive theory (Eisenhardt and Martin, 2000; Teece, 2007). In the same way, Crossan and Apaydin (2010) reaffirmed the role of professionalism as a determinant of innovation. This is because environmental performance means the success of companies in implementing the environment, strategies, models, and models central to innovation (Crossan and Apaydin, 2010). Environmental activities and processes form the basis for continuous progress in product development and processes through environmental improvement. In addition, the environmental performance also affects the company’s capacity (Cohen and Levinthal, 1990; Delmas and Burbano, 2011), representing the positive energy brought about by the success of environmental practices. High-quality environmental performance reflects the ability of companies to identify and apply new environmental knowledge to improve product performance and processes.

Empirical studies have demonstrated the contribution of environmental sustainability to environmental development. Wagner (2009) researched 2,000 manufacturing companies in Europe and reported a positive relationship between environmental sustainability and corporate innovation, product monitoring, and process updating. Likewise, environmental adjustments, measured as environmental protection, have been shown to interfere with the environmental performance of reducing pollution (Carrión-Flores and Innes, 2010). It has also been shown that the development of green products has a positive effect on the environmental performance of manufacturing in Taiwan (Chiou et al., 2011). The green building process has been shown to have a positive effect on the manufacturing sector’s environmental practices in Taiwan (Chen et al., 2006) and Turkey (Sezen and Cankaya, 2013).

Managerial stock incentive as a moderator between corporate innovation investment and environmental sustainability

An environmental perspective guided by business understanding defines a paid environmental approach, linking corporate innovation investment to financial performance (Figge and Hahn, 2012; Orsato, 2006). According to the business strategy, companies looking for profitability must work with a high level of corporate innovation investment and use the best environmental activities (Schaltegger and Synnestvedt, 2002) at the lowest cost and thus impact the economy. Remembered to the cost of eco-management literature (Schaltegger and Figge, 2000; Figge, 2005), the investment shows a low level of eco-efficiency as it measures only the company’s performance in reducing environmental problems with a little bit of business knowledge. Although environmental sustainability shows a higher level of economic efficiency, it provides a better view of the economy and productivity in its environmental management, which seems to bring positive results and economic benefits. This is because companies with a higher level of environmental sustainability can better bring about changes in the economy, developing new products and, therefore, raising the money-creating capacity of everything (Porter and Linde, 2000; Ambec and Lanoie, 2008). Likewise, improvements in ecological processes also result in reduced operating costs due to the reduction of waste caused by construction projects. Therefore, companies need to expand their investment opportunities through environmental processes and practices in the business environment to enjoy the benefits of special money features. As a result, companies can achieve significant cost savings by implementing their new corporate strategy to improve green products and processes the standards.

Data and methodology

This study examines the relationship between corporate innovation investment and environmental sustainability. Positivism-based research philosophy and deduction-based research approach are applied for the examination. In this study, a survey-based strategy and mono-method choice have been opted for analysis. The time horizon of the survey remains cross-sectional, and the study considered secondary data by conducting panel data analysis to examine causal research. Typically, panel data are utilized to determine a repressor’s influence on an outcome of interest. The study applies several robustness checks to evaluate the significance of the panel data set to ensure that a panel data set can identify such an effect. The critical assumptions of panel data such as linearity, exogeneity, homoscedasticity, non-autocorrelation, and multicollinearity have been tested to avoid biased results.

The stratified sampling technique is applied for sample selection because only that sample is selected, considering the environmental, social, and governance index disclosure in their annual reports. Stratified sampling remains superior to simple random sampling in terms of both the accuracy of its estimations and their precision level. When there are more variances between the strata, the amount of precision that may be gained increases. The contextual setting of the study was provided by oil- and gas-based companies in the United States of America. In modern times, a significant contribution has been made from US-based oil and gas companies, which are convinced to explore this role and highlight the sector’s importance as a model for the global world. Approximately 600 oil- and gas-based companies are working in the United States, and the stratified sampling technique is used to select the top companies. There are multiple databases available in the global world, but in the case of this study, secondary data were collected from the source of DataStream and published financial reports. For screening of data, techniques based on eliminating samples with missing variable data, notable treatment companies, deleting firm-year observations with many missing values to maintain integrity and consistency, and processing all continuous variables were used. After screening based on data availability and other under consideration factors, we used only 90 companies and the last 10 years’ data for statistical analysis.

Two equations are considered to examine the relationship between corporate innovation investment and environmental sustainability. In these equations, corporate innovation investment (CII) is measured using the proxy of incremental intangible assets. Intangible assets are closely related to corporate innovation activities, which can better represent innovation activities and better measure the innovation investment of enterprises. Increases in intangible assets are mainly the result of corporate innovation investment (Ju et al., 2013; Hu et al., 2020). Environmental sustainability (EntS) is measured using environmental, social, and governance indexes. Managerial stock incentive (MSI) was measured using the total percentage of shares held by all the executives with greater than 1% shareholding. Furthermore, Ctrl explains the controlling factors which include the number of independent board members (InBM), leverage as a proxy of capital structure (Lev), return on asset (ROA) as a proxy of financial performance, total asset (TA) as an indicator of firm size, and total debt (TD). Finally, in the abovementioned equations,

First, we examined normality measures by applying a descriptive statistics tool. Mean and standard deviation values were considered in APA format, which recommends further statistical analysis. Correlation matric is considered for analyzing the relationship between dependent, independent, and controlling factors, which proposes that significant evidence is founded. A generalized method of movement (GMM) was applied to check the dependence of factors and the significant evidence that supported the theoretical evidence.

Results

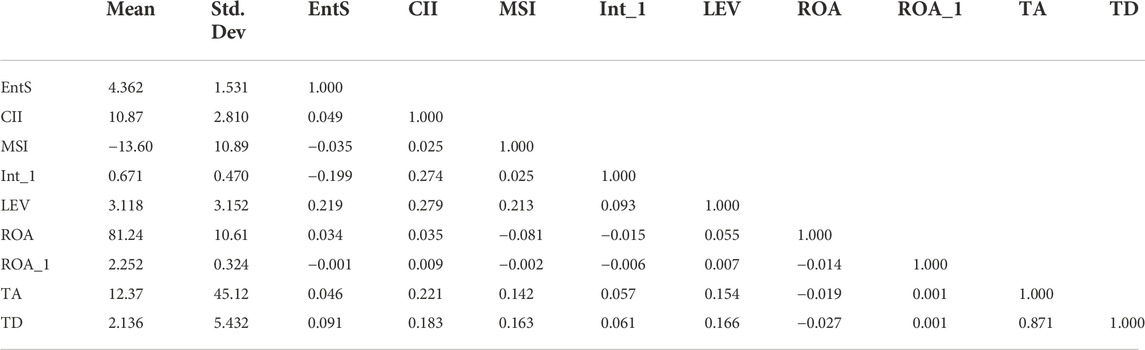

Descriptive statistics of the selected sample have been provided in Table 1. The statistics outline the properties of the data and correlation matrix. The mean value of the environmental sustainability remains (4.362) and S.D (1.53), reflecting the central deviation that states the significant difference in environmental sustainability among selected companies. Corporate innovation investment average values are (10.87) and S.D (2.810), which remain explicitly divergent among all sample units. Accordingly, the managerial stock incentives average value remains negative (-13.60), and its S.D remains (10.89), indicating a significant difference among companies selected for empirical examination.

TABLE 1. Descriptive statistics and correlation.

Moreover, the average value of intangible assets remains quite low (0.671) and S.D is (0.470), which shows that the overall incremental increase in intangible assets of American oil companies is poor. The lower value of intangible assets also reflects American firms’ poor innovation and investment capabilities. Likewise, the average value of return on asset (ROA) is quite high (81.24) and S.D is (10.61), which exhibits the high differences among companies’ performance. The mean value and standard deviation of leverage, total asset, and total debt were lower than other variables. The lower value of leverage, total asset, and total debt indicates a minor difference among these variables in companies selected as samples. Conclusively, the mean and standard deviation values indicated the sample size’s sufficiency and data normality. In addition to descriptive statistics, Table 1 also delineates the correlation matrix. The explanatory variable and dependent variable remain positively correlated. Corporate innovation investment is positively correlated with environmental sustainability and managerial stock incentives. Accordingly, the correlation matrix exhibited in Table 1 reflects no such multicollinearity issue. Therefore, examining the properties of the selected sample size and correlation matrix is statistically valid to proceed with regression analysis.

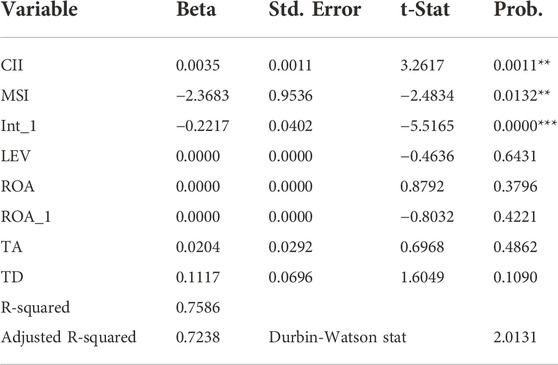

Table 2 states the regression result and confirms that corporate innovation investment significantly impacts environmental sustainability. The level of significance has been determined based on the t-value and p-value. Both values remain within the threshold, such as the t-value is (3.2617) while the p-value is (0.0011). Similarly, the managerial stock incentives as a moderating variable remain negatively significant, the t-value is (−2.4834) while the p-value is (0.0132). The negative beta (−2.3683) indicates that managerial stock inversely affects the relationship. Accordingly, the intangible asset remains a highly inverse significant t-value (−5.5165), while the p-value is (0.000).

TABLE 2. OLS regression.

The inverse significance of intangible assets reflects that it inversely determines the level of environmental sustainability. Intangible assets reflect the corporate innovation activities of a firm. However, intangible assets remain inversely correlated with environmental sustainability in the underlying sample. The managerial stock incentives as a moderating variable with corporate innovation investment negatively determine the level of environmental sustainability. In addition to these key variables, leverage, total asset, total debt, and return on asset (ROA) remain statistically insignificant. The R-squared of the estimated model remains (0.7586), indicating our model’s explanatory power.

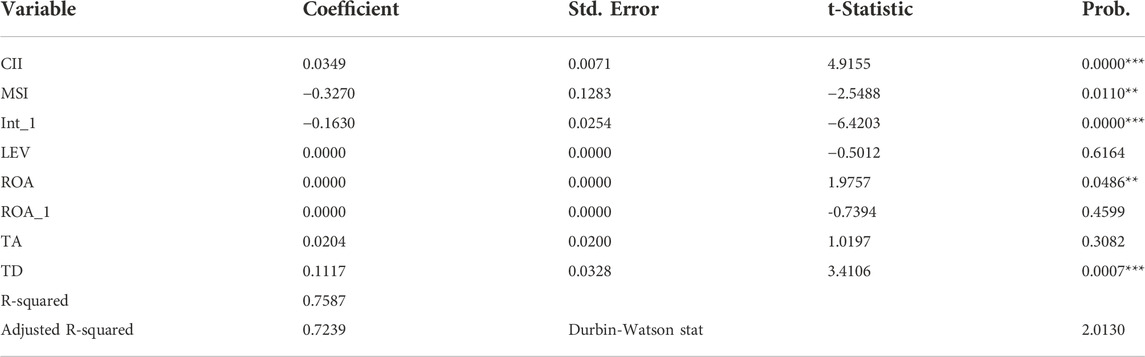

The incorporate variable determines a 0.75% variation in our dependent variable, which is quite significant and should be considered to strengthen the level of environmental sustainability. Finally, the Durbin–Watson statistic is within the threshold, which signifies no such autocorrelation problem in the estimated sample. In addition to the main OLS regression results, the robustness test has been estimated to examine any significant variation. The robustness test in Table 3 reflects significant changes in significance. The corporate innovation investment, managerial stock incentives, intangible assets, return on asset, and total debt remain significant based on t-statistic and p-value. Therefore, the data empirically proved our hypothesis regarding corporate innovation investment’s impact on environmental investment.

TABLE 3. Robustness test.

Discussion and conclusion

In this study, we mainly focused on oil- and gas-based companies in the United States of America from 2009 to 2019 as a research sample and empirically examined the impact of corporate innovation investment on environmental sustainability. Statistical results reflected a significant positive relationship between corporate innovation investment and environmental sustainability in USA-based companies. The positive inclusion of intangible assets leads to motivation in innovation that enhances the context of environmental sustainability (Ahmad and Zheng 2021; Ali et al., 2021; Ma and Qamruzzaman, 2022). There could be possible potential determinants that can increase the level of intangible assets, and corporate social responsibility is a potential factor. CSR information disclosure establishes a strong relationship between the stakeholders which can regularly associate with the company’s exposures (Ullah and Sun, 2021). This will not only establish a strong association, but stakeholders will also come to know about the actual operating conditions of the companies. These activities develop the information transparency level and improve corporate reputation among the donors and investors, which will increase corporate innovation funds (Caputo et al., 2021).

Well-reputed and international organizations found consistency in CSR information disclosure by investing money for corporate innovation, achieving sustainable development goals, and establishing a positive social role. Local organizations also need to play an exemplary role that will meet their social and financial objectives and provide a positive example for the security market. The managerial stock incentive is significant and moderates the relationship between corporate innovation investment and environmental sustainability. When formulating an innovation strategy or policy, enterprises should not only fully consider their management stock mechanism but also design the contract according to the innovation level of the enterprise to determine the level of managerial incentive.

The findings of this study are important and contribute a significant role to the existing research system. This study provides insight regarding the significant role of corporate innovation, which establishes a way forward to environmental sustainability. This study expanded the context of corporate innovation investment, which means a significant improvement in firms’ incentives to innovate can enhance the level of environmental sustainability as such type of social activities establishes a high level of corporate reputation among the investors and can mitigate the problems of financial constraints, which leads toward allocation of funds for achieving sustainable development goals, especially environmental sustainability. Moreover, the managerial stock incentive is conducive to reducing agency costs and improving information disclosure, thus strengthening the positive relationship between corporate innovation investment and environmental sustainability.

Limitations and future directions

This study has been conducted in the context of a developed economy but still has a few limitations. First, the study focused only on one country’s oil and gas sector, which can be limited in the generalizability of findings in a global world. Therefore, future studies need to incorporate the comparison of different sectors and nations, enriching the generalizability of the results and enhancing the worth of the findings. Second, the sample set of the said study considered the latest 10 years, which needs to be expanded in decades. Pre- and post-comparison for different regimes can create worthy research studies. Future studies should empirically examine other antecedents and outcomes of environmental sustainability and corporate innovation investment. Especially, the inclusion of corporate social responsibility information disclosure can enhance the worth of future studies.

Data availability statement

The original contributions presented in the study are included in the article/Supplementary Material; further inquiries can be directed to the corresponding authors.

Author contributions

All authors listed have made a substantial, direct, and intellectual contribution to the work and approved it for publication.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors, and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Ahmad, M., and Zheng, J. (2021). Do innovation in environmental-related technologies cyclically and asymmetrically affect environmental sustainability in BRICS nations? Technol. Soc. 67, 101746. doi:10.1016/j.techsoc.2021.101746

Ali, U., Li, Y., Yanez Morales, V. P., and Hussain, B. (2021). Dynamics of international trade, technology innovation, and environmental sustainability: Evidence from asia by accounting for cross-sectional dependence. J. Environ. Plan. Manag. 64 (10), 1–22. doi:10.1080/09640568.2020.1846507

Allen, F., Qian, J., and Qian, M. (2005). Law, finance, and economic growth in China. J. financial Econ. 77 (1), 57–116. doi:10.1016/j.jfineco.2004.06.010

Ambec, S., and Lanoie, P. (2008). Does it pay to be green? A systematic overview. Acad. Manag. Perspect. 22, 45–62. doi:10.5465/amp.2008.35590353

Ang, J. S., Cheng, Y., and Wu, C. (2014). Does enforcement of intellectual property rights matter in China? Evidence from financing and investment choices in the high-tech industry. Rev. Econ. Stat. 96 (2), 332–348. doi:10.1162/rest_a_00372

Arouri, M. E. H., Caporale, G. M., Rault, C., Sova, R., and Sova, A. (2012). Environmental regulation and competitiveness: Evidence from Romania. Ecol. Econ. 81, 130–139. doi:10.1016/j.ecolecon.2012.07.001

Barney, J. (2015). Firm resources and sustained competitive advantage. J. Manag. 17 (1), 99–120. doi:10.1177/014920639101700108

Bigliardi, B., Bertolini, M., Klewitz, J., Zeyen, A., and Hansen, E. G. (2012). Intermediaries driving eco innovation in SMEs: A qualitative investigation. Eur. J. Innovation Manag. 15, 442. doi:10.1108/14601061211272376

Borim-de-Souza, R., Balbinot, Z., Travis, E. F., Munck, L., and Takahashi, A. R. W. (2015). Sustainable development and sustainability as study objects for comparative management theory. Cross Cult. Manag. 22, 201. doi:10.1108/CCM-02-2013-0027

Caiazza, R., Volpe, T., Stanton, J. L., Griffith, C. J., Bossle, M. B., De Barcellos, M. D., et al. (2016). Why food companies go green? The determinant factors to adopt eco-innovations. Br. Food J. 118, 1317–1333. doi:10.1108/bfj-10-2015-0388

Caputo, F., Pizzi, S., Ligorio, L., and Leopizzi, R. (2021). Enhancing environmental information transparency through corporate social responsibility reporting regulation. Bus. Strategy Environ. 30 (8), 3470–3484. doi:10.1002/bse.2814

Carrión-Flores, C. E., and Innes, R. (2010). Environmental innovation and environmental performance. J. Environ. Econ. Manag. 59 (1), 27–42. doi:10.1016/j.jeem.2009.05.003

Chang, C. H. (2011). The influence of corporate environmental ethics on competitive advantage: The mediation role of green innovation. J. Bus. Ethics 104 (3), 361–370. doi:10.1007/s10551-011-0914-x

Chang, M. C., and Hu, J. L. (2011). Inconsistent preferences in environmental protection investment and the central government's optimal policy. Appl. Econ. 43 (6), 767–772. doi:10.1080/00036840802599891

Chen, Y. S., Lai, S. B., and Wen, C. T. (2006). The influence of green innovation performance on corporate advantage in Taiwan. J. Bus. Ethics 67 (4), 331–339. doi:10.1007/s10551-006-9025-5

Chiou, T. Y., Chan, H. K., Lettice, F., and Chung, S. H. (2011). The influence of greening the suppliers and green innovation on environmental performance and competitive advantage in Taiwan. Transp. Res. Part E Logist. Transp. Rev. 47 (6), 822–836. doi:10.1016/j.tre.2011.05.016

Clarkson, P. M., Li, Y., Richardson, G. D., and Vasvari, F. P. (2011). Does it really pay to be green? Determinants and consequences of proactive environmental strategies. J. Account. Public Policy 30 (2), 122–144. doi:10.1016/j.jaccpubpol.2010.09.013

Cohen, W. M., and Levinthal, D. A. (1990). Absorptive capacity: A new perspective on learning and innovation. Adm. Sci. Q. 35, 128–152. doi:10.2307/2393553

Crossan, M. M., and Apaydin, M. (2010). A multi-dimensional framework of organizational innovation: A systematic review of the literature. J. Manag. Stud. 47 (6), 1154–1191. doi:10.1111/j.1467-6486.2009.00880.x

Delmas, M. A., and Burbano, V. C. (2011). The drivers of greenwashing. Calif. Manag. Rev. 54 (1), 64–87. doi:10.1525/cmr.2011.54.1.64

Delmas, M., Lim, J., and Nairn-Birch, N. (2016). Corporate environmental performance and lobbying. Acad. Manag. Discov. 2 (2), 175–197. doi:10.5465/amd.2014.0065

Dillard, J., Pullman, M. E., Loucks, E. S., Martens, M. L., and Cho, C. H. (2010). Engaging small and medium sized businesses in sustainability. Sustain. Account. Manag. Policy J. 1, 178. doi:10.1108/20408021011089239

Dowell, G., Hart, S., and Yeung, B. (2000). Do corporate global environmental standards create or destroy market value? Manag. Sci. 46 (8), 1059–1074. doi:10.1287/mnsc.46.8.1059.12030

Eisenhardt, K. M., and Martin, J. A. (2000). Dynamic capabilities: What are they? Strateg. Manag. J. 21 (10-11), 1105–1121. doi:10.1002/1097-0266(200010/11)21:10/11<1105::aid-smj133>3.0.co;2-e

Eltayeb, T. K., Zailani, S., and Ramayah, T. (2011). Green supply chain initiatives among certified companies in Malaysia and environmental sustainability: Investigating the outcomes. Resour. conservation Recycl. 55 (5), 495–506. doi:10.1016/j.resconrec.2010.09.003

Figge, F., and Hahn, T. (2012). Is green and profitable sustainable? Assessing the trade-off between economic and environmental aspects. Int. J. Prod. Econ. 140 (1), 92–102. doi:10.1016/j.ijpe.2012.02.001

Figge, F. (2005). Value based environmental management. From environmental shareholder value to environmental option value. Corp. Soc. Responsib. Environ. Manag. 12 (1), 19–30. doi:10.1002/csr.74

Forsman, H. (2013). Environmental innovations as a source of competitive advantage or vice versa? Bus. Strategy Environ. 22 (5), 306–320. doi:10.1002/bse.1742

Goodland, R. (1995). The concept of environmental sustainability. Annu. Rev. Ecol. Syst. 26 (1), 1–24. doi:10.1146/annurev.es.26.110195.000245

Grekova, K., Bremmers, H. J., Trienekens, J. H., Kemp, R. G. M., and Omta, S. W. F. (2013). The mediating role of environmental innovation in the relationship between environmental management and firm performance in a multi-stakeholder environment. J. Chain Netw. Sci. 13 (2), 119–137. doi:10.3920/jcns2013.1003

Hart, S. L., and Dowell, G. (2011). Invited editorial: A natural-resource-based view of the firm: Fifteen years after. J. Manag. 37 (5), 1464–1479. doi:10.1177/0149206310390219

Hu, W., Du, J., and Zhang, W. (2020). Corporate social responsibility information disclosure and innovation sustainability: Evidence from China. Sustainability 12 (1), 409–419. doi:10.3390/su12010409

Ju, X. S., Lu, D., and Yu, Y. H. (2013). Financing constraints, working capital management and enterprise innovation sustainability. Econ. Res. 1, 4–16.

Lee, V. H., Ooi, K. B., Chong, A. Y. L., and Lin, B. (2015). A structural analysis of greening the supplier, environmental performance and competitive advantage. Prod. Plan. Control 26 (2), 116–130. doi:10.1080/09537287.2013.859324

Li, S., Niu, J., and Tsai, S. B. (2018). Opportunism motivation of environmental protection activism and corporate governance: An empirical study from China. Sustainability 10 (6), 1725. doi:10.3390/su10061725

Liao, Z. (2016). Temporal cognition, environmental innovation, and the competitive advantage of enterprises. J. Clean. Prod. 135, 1045–1053. doi:10.1016/j.jclepro.2016.07.021

Long, X., Chen, Y., Du, J., Oh, K., and Han, I. (2017). Environmental innovation and its impact on economic and environmental performance: Evidence from Korean-owned firms in China. Energy Policy 107, 131–137. doi:10.1016/j.enpol.2017.04.044

Ma, C., and Qamruzzaman, M. (2022). An asymmetric nexus between urbanization and technological innovation and environmental sustainability in Ethiopia and Egypt: What is the role of renewable energy? Sustainability 14 (13), 7639. doi:10.3390/su14137639

Musa, H., and Chinniah, M. (2016). Malaysian SMEs development: Future and challenges on going green. Procedia - Soc. Behav. Sci. 224, 254–262. doi:10.1016/j.sbspro.2016.05.457

Orlitzky, M., Schmidt, F. L., and Rynes, S. L. (2003). Corporate social and financial performance: A meta-analysis. Organ. Stud. 24 (3), 403–441. doi:10.1177/0170840603024003910

Orsato, R. J. (2006). Competitive environmental strategies: When does it pay to be green? Calif. Manag. Rev. 48 (2), 127–143. doi:10.2307/41166341

Porter, M., and Linde, C. (2000). Green and competitive: Ending the stalemate. The Dynamics of the eco-efficient economy. Cheltenham/Northampton: Edward Elgar, 33–55.

Rassier, D. G., and Earnhart, D. (2010). Does the porter hypothesis explain expected future financial performance? The effect of clean water regulation on chemical manufacturing firms. Environ. Resour. Econ. (Dordr). 45 (3), 353–377. doi:10.1007/s10640-009-9318-0

Schaltegger, S., and Figge, F. (2000). Environmental shareholder value: Economic success with corporate environmental management. Eco-Mgmt. Aud. 7 (1), 29–42. doi:10.1002/(sici)1099-0925(200003)7:1<29::aid-ema119>3.0.co;2-1

Schaltegger, S., and Synnestvedt, T. (2002). The link between ‘green and economic success: Environmental management as the crucial trigger between environmental and economic performance. J. Environ. Manag. 65 (4), 339–346. doi:10.1016/s0301-4797(02)90555-4

Sezen, B., and Cankaya, S. Y. (2013). Effects of green manufacturing and eco-innovation on sustainability performance. Procedia - Soc. Behav. Sci. 99, 154–163. doi:10.1016/j.sbspro.2013.10.481

Suárez, D. (2014). Persistence of innovation in unstable environments: Continuity and change in the firm's innovative behavior. Res. Policy 43 (4), 726–736. doi:10.1016/j.respol.2013.10.002

Swanson, L. A., and Zhang, D. D. (2012). Perspectives on corporate responsibility and sustainable development. Manag. Environ. Qual. Int. J. 23 (6), 630–639. doi:10.1108/14777831211262918

Teece, D. J. (2007). Explicating dynamic capabilities: The nature and microfoundations of (sustainable) enterprise performance. Strateg. Manag. J. 28 (13), 1319–1350. doi:10.1002/smj.640

Triguero, A., and Córcoles, D. (2013). Understanding innovation: An analysis of persistence for Spanish manufacturing firms. Res. Policy 42 (2), 340–352. doi:10.1016/j.respol.2012.08.003

Ullah, S., and Sun, D. (2021). Corporate social responsibility corporate innovation: A cross country study of developing countries. Corp. Soc. Responsib. Environ. Manag. 28 (3), 1066–1077. doi:10.1002/csr.2106

Verspagen, B. (2006). University research, intellectual property rights and European innovation systems. J. Econ. Surv. 20 (4), 607–632. doi:10.1111/j.1467-6419.2006.00261.x

Wagner, M. (2009). Innovation and competitive advantages from the integration of strategic aspects with social and environmental management in European firms. Bus. Strategy Environ. 18 (5), 291–306. doi:10.1002/bse.585

Wagner, M., and Schaltegger, S. (2004). The effect of corporate environmental strategy choice and environmental performance on competitiveness and economic performance: Eur. Manag. J. 22 (5), 557–572. doi:10.1016/j.emj.2004.09.013

Wagner, M., Van Phu, N., Azomahou, T., and Wehrmeyer, W. (2002). The relationship between the environmental and economic performance of firms: An empirical analysis of the European paper industry. Corp. Soc. Responsib. Environ. Manag. 9 (3), 133–146. doi:10.1002/csr.22

Wu, P. J., and Yang, C. K. (2021). Sustainable development in aviation logistics: Successful drivers and business strategies. Bus. Strategy Environ. 30 (8), 3763–3771. doi:10.1002/bse.2838

Yang, C. H., Tseng, Y. H., and Chen, C. P. (2012). Environmental regulations, induced R&D, and productivity: Evidence from Taiwan's manufacturing industries. Resour. Energy Econ. 34 (4), 514–532. doi:10.1016/j.reseneeco.2012.05.001

Keywords: corporate innovation investment, environment sustainability, managerial stock incentives, generalized method of movement, financial sustainability

Citation: Tang H, Rasool Z, Sindhu MI, Naveed M and Babar SF (2023) Implications of corporate innovation investment on environment sustainability with moderating role of managerial stock incentives: A case of the oil and gas sector of the United States of America. Front. Environ. Sci. 10:962258. doi: 10.3389/fenvs.2022.962258

Received: 12 June 2022; Accepted: 11 August 2022;

Published: 04 January 2023.

Edited by:

Rita Yi Man Li, Hong Kong Shue Yan University, Hong Kong, SAR ChinaReviewed by:

Mário Nuno Mata, Instituto Politécnico de Lisboa, PortugalRodrigo Salvador, Technical University of Denmark, Denmark

Copyright © 2023 Tang, Rasool, Sindhu, Naveed and Babar. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Zeeshan Rasool, zeeshan_rasool114@hotmail.com; Muzammal Ilyas Sindhu, muzammal496@gmail.com