1. Introduction

A transition from a fossil-fuel-based energy system to a decarbonized one is key to performing a cost-effective strategy to mitigate climate change [

1] and achieve the 2 °C threshold aim of the Paris agreement. Within this context, renewable energy sources (RESs) represent the most promising technology for the transition and the future system. RESs are almost free-emission technologies and, during the last few years, RESs achieved economic competitiveness against conventional energy sources. However, their deployment in traditional power systems is not absent of challenges. The stochastic nature of renewable generation, the non-storable characteristic of electricity in a cost-effective way, and the low elasticity in demand associated with its difficulties to participate in electricity markets [

2] make their variability a major issue with a wider impact on smaller systems. Moreover, the final energy consumption will tend to become electric in order to reduce emissions. Thus, future loads will impose new demands and challenges to the power system such as the massive penetration of electric vehicles (EV) to electrify transport.

In order to overcome this problem, the smart grid concept was an accepted solution for some time now. Smarts grids are electricity networks that intelligently integrate their users’ actions to efficiently deliver economic, secure, and sustainable electricity [

3]. The implementation of smart grids implies broad and sophisticated functionalities of electric transport and distribution systems, improving their flexibility, allowing bidirectional energy flows, and facilitating RES and demand response (DR) integration. The demand response is based on developing active participation of customers with new requirements that take into account technology and equipment for customer communications, relations, and services. However, just with the participation of demand, the security of supply will still be jeopardized with larger levels of stochastic production associated with renewable generation. Thus, storage systems will also be required to provide flexibility and ensure reliability to the system [

4]. Moreover, the batteries’ cost reductions make them a key component in the future power systems [

5].

Currently, the electricity sector finds itself making three classes of transformations: firstly, the improvement of the current infrastructure; secondly, the addition of the digitalization of power systems, which is the essence of communications and data generation in smart grids; thirdly, business process transformation to perform, in addition to the traditional activities, new ones, or providing infrastructure and data to agents such as aggregators and virtual power plants (VPPs). These agents do new activities related to meeting customer needs and expectations in a more efficient way than the traditional centralized system. These three transformations were approached in several different ways, which were mainly described on a very abstract level [

6] or focused on specific aspects such as just information and communication technology (ICT) [

7]. Different standardization bodies developed specific concepts such as the American National Institute of Standards and Technology (NIST) framework and roadmap for smart grid standards [

8] and the European Smart Grid Architecture Model (SGAM) [

9]. However, the necessary new activities, agents, and interactions among them in the future electricity markets are not clearly defined and authors still characterize them in different ways. Therefore, it is necessary to align specific agents to established practical conceptual architectures as suggested by Neuriter et al., [

10].

The functionality of the future power systems and markets may look quite different according to the local social, regulatory, or economic environment. Nevertheless, they have common applications and requirements for digital processing and communications to implement advanced control in all elements of the power system, allowing for bidirectional communication and energy flows [

8], understanding the automation of processes and systems as digital processing to retrieve data and perform actions. According to this context, smart grids enable greater information management and efficiency compared to conventional power systems, thus allowing the exploitation of the benefits associated with RES, demand response, storage systems, and real-time competition and response in local markets. Local markets are arising as a new mechanism to provide an efficient allocation and pricing of the growing distributed generation (DG) and flexible demand [

11,

12].

Thus, smart grids are emerging as a solution for the future of power systems [

13]. This broad concept that comprises many different agents, actors, and technology was approached in different ways. Its future faces different problems and sub-problems, which were widely studied. According to Reference [

14], some of these are operation and management, energy storage, security, stability, and protection, demand control, or service restoration, among others.

For instance, some authors proposed multi-agent systems that optimize resource scheduling in smart grids [

15,

16]. These agents enable the system to behave in a more reliable and efficient way. However, the description of these agents does not follow any standardized premise. The authors of References [

17,

18] proposed energy management systems in smart grids. The agents as in Reference [

15] did not include a clear definition of the agent boundaries of action or relationships and presented conflicts between them. A review of agent-based models was presented in Reference [

19], where the necessity of harmonization between studies was highlighted.

In order to tackle the previously mentioned standardization problems, different meta-architectures were developed. These conceptual architectures provide a family of ontologies to map smart grids and guidelines on how to use standards [

7]. The main two developments were the previously mentioned NIST work and SGAM.

In the United States of America (USA), the NIST created relevant conceptual models for the smart grid. NIST considered the approach that the smart grid can be divided into seven domains [

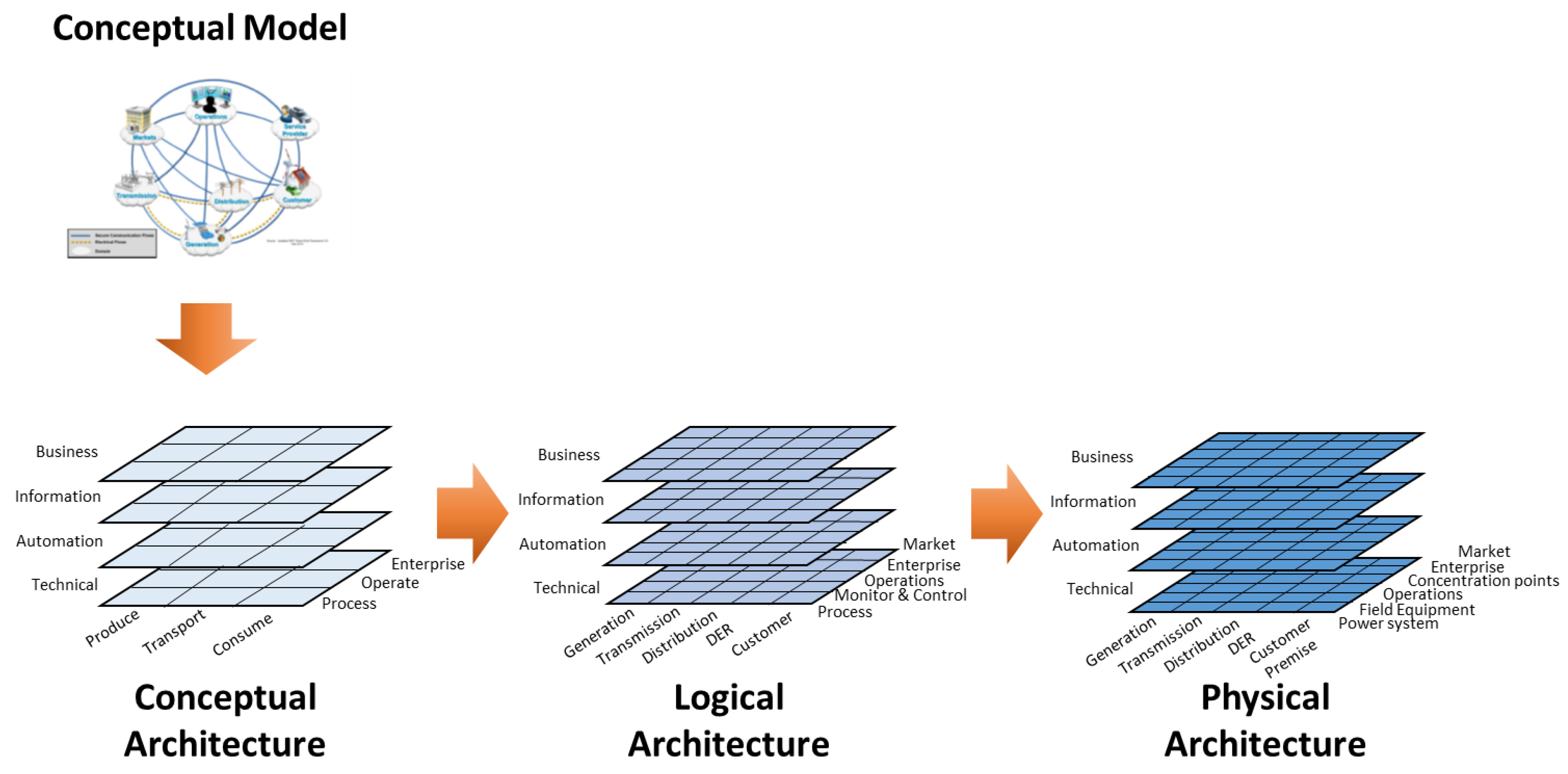

8]. These domains and their sub-domains enclose the conceptual roles and services, including stakeholders, interactions, and types of services. On the other hand, the M/490 working group on reference architectures created the SGAM, which can be seen as a similar effort on the European level. SGAM is based on NIST and proposes a model with five interoperability layers, five domains, and six zones, as can be seen in

Figure 1. Thus, every element in the model can be located in a three dimension grid according to its interoperability, domain, and zone characteristics [

9]. As in the case of NIST, SGAM requires stronger integration between the design and the use cases and formal semantics [

20], as it lacks of precise descriptions.

Highly correlated with smart grid development, the three novel agents of aggregator, storage, and virtual power plant (VPP) are being developed. In all these cases, several authors published studies on the topic. However, if the case of smart grids is still not clear and no standard definitions are used, VPP, storage, and aggregators offer an even wider range of variation and disagreement. The importance of these three agents is relevant for the conception of smart grids since these agents are crucial for the security and reliability of power systems with increasing levels of renewable penetration [

21]. For instance, some authors optimized VPP bidding strategies [

22,

23,

24], renewable energy integration [

25,

26], the use of demand response in smart grids [

27], or the usage of RESs at the residential level [

28,

29]. However, there exists a lack of a standardized definition, interactions, and roles performed by a VPP.

Demand response is also stated to have an increasing role in power systems due to its potential capacity to help manage renewable variability [

30]. Work was done in analyzing the cost of automated DR systems [

31], the suitability of different customers [

32], the evaluation of the action performance [

33,

34], or its optimization in smart grid programs [

35]. Moreover, its role among active consumers at the distribution level is gaining importance [

36]. Storage is seen as the key technology to enable RES integration in the future power systems [

4,

37]. Under this paradigm, storage systems are already a key agent in the power system as in the case of the Tesla Battery of South Australia [

38]. However, the particularities and services that they provide are far from being homogeneous or clear among scholars and systems. Finally, in a similar line, aggregators were approached in different ways by authors and regulators, but also lack a clear common definition [

39]. Moreover, authors do not share a common view on the size that optimal aggregation should have. For instance, while the authors of Reference [

40] argued that aggregation is only profitable at large levels, the authors of Reference [

41] defended that, even at low levels, aggregation offers benefits. In sum, agents are not clearly defined and the interactions between them vary among authors.

The conceptual architecture here developed is based on the NIST framework [

8] and builds on providing the relationships and interaction design between the different agents. These agents can be performed by different entities or one entity, company, or organization that could hold more than one of the agents’ responsibilities. Reference levels of power, voltage, and minimum bidding levels were parameterized to be chosen depending on the system, thus providing an easy way to implement the conceptual architecture to any power system. Thus, the proposed conceptual architecture can be applied to any type of power sector, independently of the level of decentralization and its size.

The main contributions of this paper are the following:

A novel conceptual architecture for the development of the next-generation electricity markets to unlock all the hidden potential of flexible and distributed energy resources, taking into special consideration the potential benefits for active consumers, is proposed based on the analysis of the shortcomings of the current standardized models that can be found in the literature. This model provides a path that policy-makers can follow to eliminate barriers to integrate Distributed Energy Resources (DER) in a competitive way at distribution level.

A complete description of the main roles/activities that should be assumed by the different agents in the proposed architecture is provided based on an ontological and a service-oriented analysis.

A detailed proposal of the interactions that would occur among agents of the developed architecture is presented. These interactions were carefully analyzed from all points of view: energy flows, operation services, and economic transactions.

The impacts on the performance of the conceptual model associated with the inclusion of local energy markets are analyzed and presented in this paper. This could help overcome the current flaws in real-time trading.

The rest of the paper is structured as follows:

Section 2 outlines the NIST methodology used for building the proposed design to upgrade the current one. Then, the specific agents proposed for a standardized architecture are developed in

Section 3. Finally, in

Section 4, some conclusions are drawn.

2. Materials and Methods

The power system and market conceptual design methodology is described in this section. This method is framed under the framework of the NIST roadmap for smart grids [

8]. The methodology proposed by the NIST was considered as a base to develop smart grid conceptual architectures by several authors and other standards [

9,

42]. In this regard, this methodology was selected as a meta architecture to develop the proposed upgrade of the existing architecture.

According to Reference [

7], the first action is the specification of the roles/services that should be expected from the general implementation of smart grids. In addition to the traditional roles/services that are inherent in an electricity distribution system (i.e., generators and retailers), some additional agents should be expected from the combination of the new environmental requirements and advanced technology.

In this regard, the smart grid agents need to be designed to enable the system to successfully respond to the following needs:

Providing a full technical and economic integration of distributed generation. This generation is generally difficult to integrate because of the low size, intermittent production, quality problems, and inability to provide operation services.

Providing enhanced services and opportunities to the customers, allowing more tailored trading of their demand/generation resources, including interaction with retail energy and services markets/products.

Providing an enhanced operation of the distribution system, both in normal conditions (such as reconfiguration for more efficient operation or for more secure supply) and in faulty conditions in order to allow a faster and more effective reaction to faults (fault location, reconfiguration, self-healing, etc.).

Providing information services, based on measurements, to actors in the field of the energy supply such as aggregators, energy services companies (ESCOs), VPPs, etc.

Providing the ability to accommodate and manage the presence of new loads at the customer level, such as the massive connection of electric vehicles.

It is important to highlight that the implementation of these agents can require the participation of new entities or the redesign of functions that will have to be performed by existing organizations.

A conceptual architecture is necessary to design a system capable of carrying out the roles/services that smart grids must perform according to the abovementioned needs. At this point, it is necessary to define a set of concepts that can be widely used along the description of the architecture:

Agent: a specific function, capability, or sum of services played by an entity that cannot be split. In some systems, one entity can have in its business portfolio duties of several agents of this conceptual architecture.

Activities: things that an agent does or has the capability to do.

Component: a basic part from which something is made; the physical assets that are intrinsic to each agent.

Transaction: agreement between two agents (one buys and the other one sells) to exchange goods, services, or financial instrument.

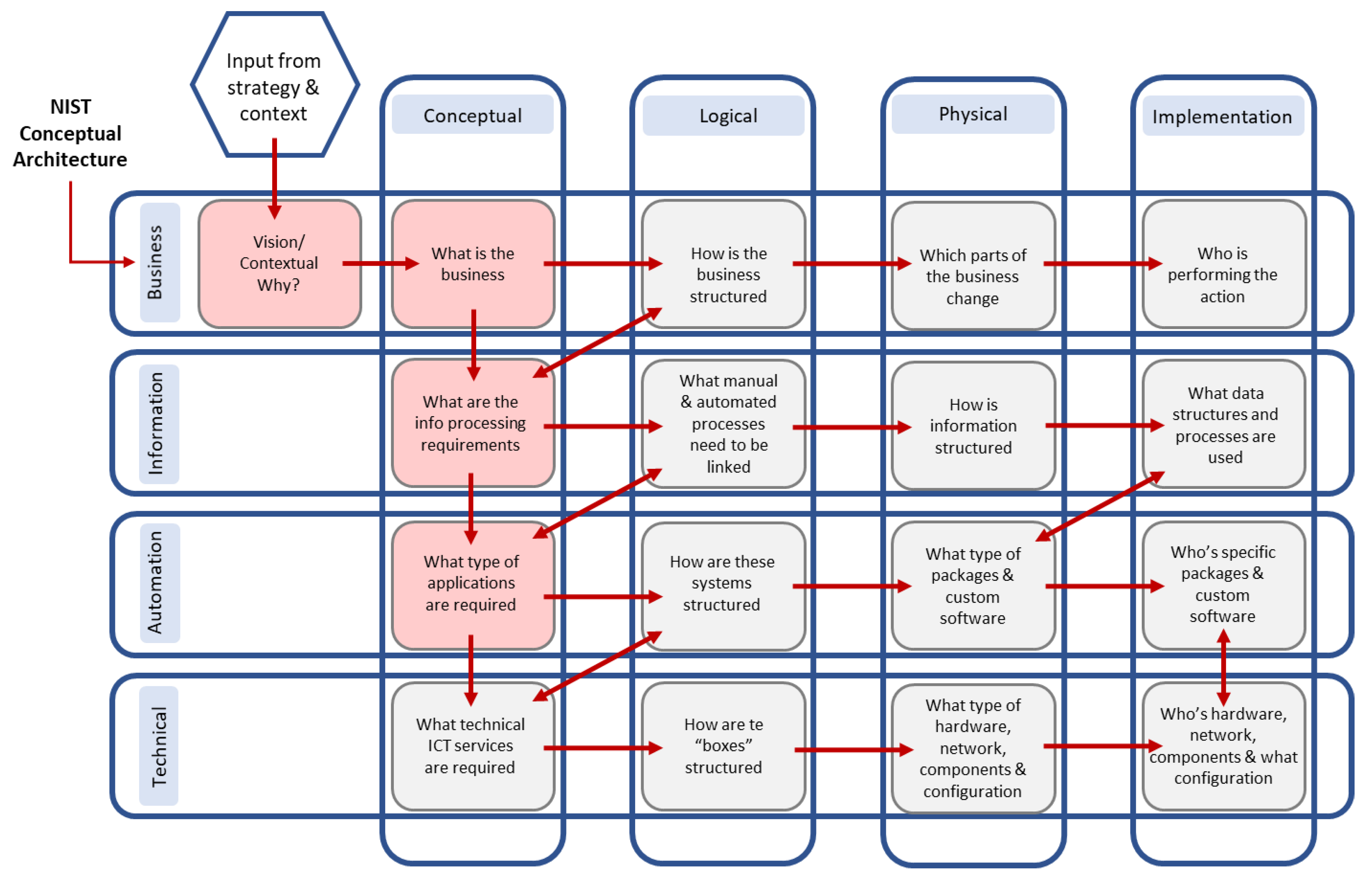

In order to align the architecture with the required services of the system, an ontological definition is required according to Reference [

7]. For doing so, the methodology proposed in NIST, shown in

Figure 2, was used.

According to this procedure, four architectural levels must be considered to design the agents: business, information, automation, and technology. All these levels must be described to answer the four required layers: conceptual, logical, physical, and its implementation.

After this first context analysis, the interactions among the different agents were carefully studied to satisfy the required relationship needs among them. The entities required to implement a smart grid are, in general, quite standard; however, some agents’ activities assigned to these entities may not be so established and, in some cases, can be a bit confusing in the literature, where different approaches to the same agents can be found.

The next section is devoted to presenting the novel conceptual architecture. Firstly, each agent is defined based on the existing knowledge and literature, and the activities expected for the agent are identified. According to these activities, the necessary physical components that each agent owns are described. This includes assets like physical generators, transmission lines, etc. Finally, the power flows, operating service, or economic transactions of each agent with the rest of them are described to fulfil the expected new requirements and functionalities of smart grids.

3. Discussion of Agent Conceptual Architecture for Market Implementation

The agents and nomenclature required for the upgraded conceptual architecture proposed in this paper are depicted in

Table 1. The integration of different types of distributed generation, storage, and demand response resources to provide firm power production, as well as the active participation of the customers, were considered in detail.

The conceptual architecture was completed with the transactions allowed between agents, as summarized in

Table 2, where economic, energy, and operation service transactions between the different agents are proposed. A matrix representation of the allowed transactions among agents is shown in different colors in this table. The possible transactions from the agent in a row to the agent in the column are represented by triangles. For instance, position T

12 shows the transactions from consumers to generators, which are only economic, as consumers just pay generators for consuming electricity. On the other hand, T

21 shows how generators provide energy to consumers. Another example could be position T

43, where aggregators provide power flows and operating services to VPPs. In exchange for this, T

34, VPPs make economic payments to aggregators.

The different agents must accomplish these transactions (economic, energy, or service) in a coordinated way, based on what is required to interchange information with the rest of the participants in the power system. Traditional and new entities coexist in the proposed model. Agents whose activities change from traditional models are described in more detail in this chapter, while traditional ones are described when some of their original characteristics change.

3.1. Active Consumers

Consumers are the end-users of electricity, and they use it to perform specific activities (industrial, commercial, or residential). Three different types of consumers are considered depending on their connection point to the grid as follows:

Low voltage (LV): Consumers. The voltage supply is lower than VHV kV, and they are connected to the LV distribution network. They are usually residential or small commercial customers.

High voltage (HV): Consumers to distribution. Connected to the distribution power system with a voltage larger than VHV kV. They are typically medium industrial and commercial consumers.

High voltage (HV): Consumers to transmission. Connected to the transmission or sub-transmission power system level with a voltage larger than VHV kV. They are typically large industrial and commercial consumers.

Consumers used to be a static agent that only consumed energy. Currently, this activity can be complemented with the production of electricity through self-generation, providing demand response resources, and being an active participant in electricity markets.

Consumers can be understood as a sum of loads that can own the metering equipment. Recently, it is becoming more and more common that customers may build their own generation resources, especially by using renewable resources. These generation facilities may range from a few kW to several MW. When generated electricity exceeds the demand, it can be sold to the main grid through retail companies that will be responsible for ensuring the economic compensation to small consumers by providing an electricity net balance with the system specified prices.

Regarding demand response resources (DRRs), they may exist in the customer facilities as a part of the demand that can be reduced/incremented according to the prices in the operation markets. Currently, it is becoming common that consumers own electric vehicles and small storage systems that can be operated in a smart way by aggregators or themselves [

49] to have the possibility to offer operation services. Consumers should have the required communication systems to provide DRR in this case. Consequently, and depending on their size, consumers may require communication systems with other agents. For example, large flexible consumers will require direct communication with the TSO if they are connected to the transmission grid or direct communication with the distribution system operator (DSO) if they are connected to the distribution system. On the other hand, small and medium consumers will just interact with aggregators.

The consumer’s main traditional transaction is to buy electricity from the grid and pay for it. Consumers can also now sell electricity to the grid and, eventually, may offer DRR directly to the DSO in a case where the size of the operable load is higher than the required POS-D. Additionally, these DRRs could also be offered directly to the transmission system operator (TSO) if they are larger than POS-T or through the aggregator. Regarding the economic transactions, consumers pay for the electricity consumed to retailers if they do not directly access the markets. If they do, they pay for energy to the wholesale market operator or the local market operator, to whom they can also sell electricity for dynamic balancing. Additionally, they can also establish bilateral contracts with generators or VPPs. Regarding the operation services, consumers receive payments for the use of their flexible resources from the TSO, DSO, aggregators, VPPs, and generators, depending on who uses their flexibility. Finally, since consumers are the end-users of the system, they defray most of the incurred costs, such as transmission and distribution system usage, market and system operators, etc. They may pay them directly to the involved agents or, more commonly, they make a single payment to the retailer who divides it up with the rest of agents that receive payments from the consumer.

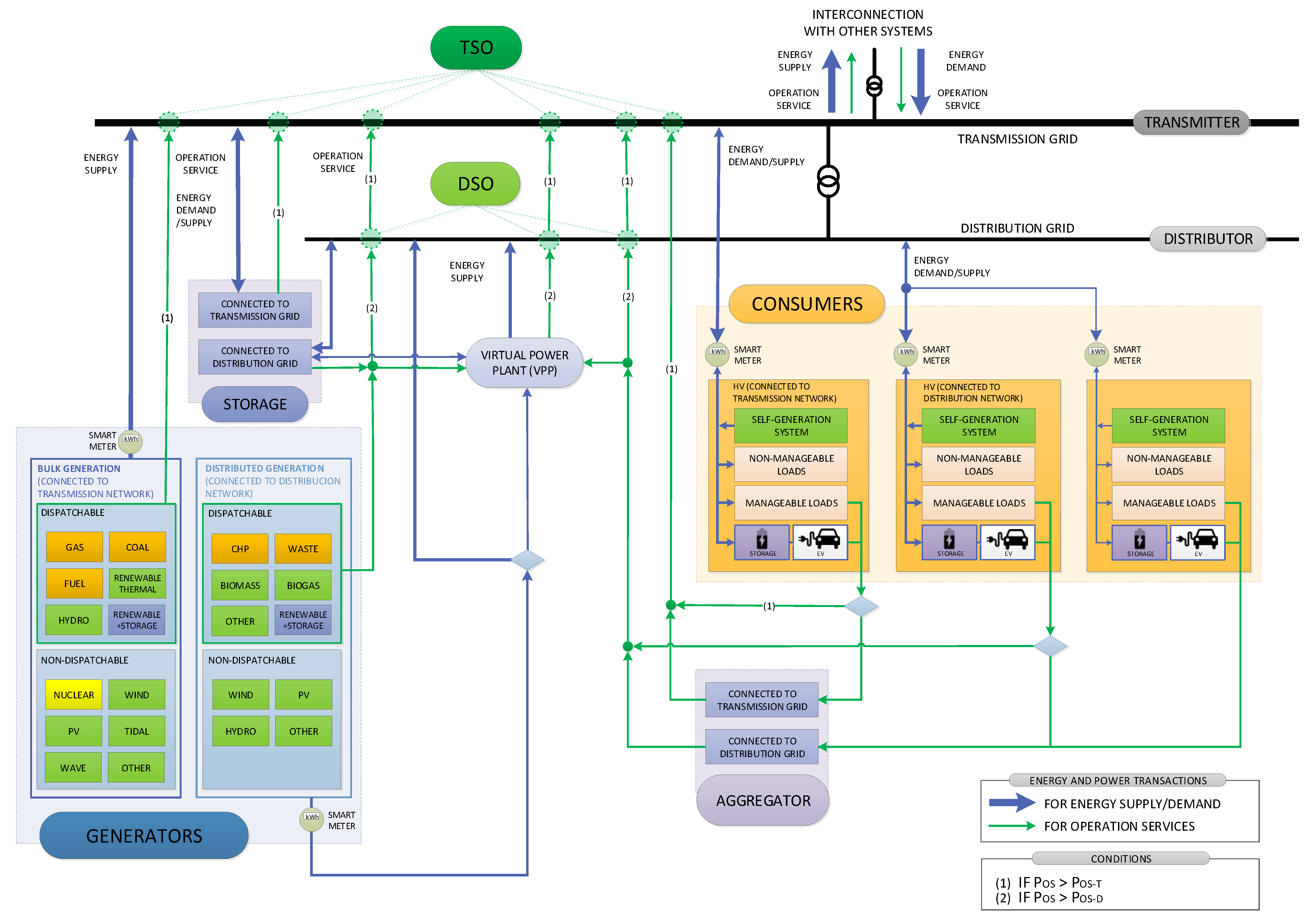

3.2. Generators

An electricity generator is an agent that owns the facilities to convert any type of primary energy into electricity.

The main activity of generators is to produce the electricity that is used by consumers. Moreover, generators have the capability to provide operation services (OSs), which are mandatory in some cases and optional in the rest. Optional OSs may be traded in markets or through contracts. Both energy and operation services can be provided to other agents via markets or bilateral contracts. Moreover, the regulation in most countries enforces the obligation to provide some type of primary (spinning) reserve to the TSO from any committed generator [

21].

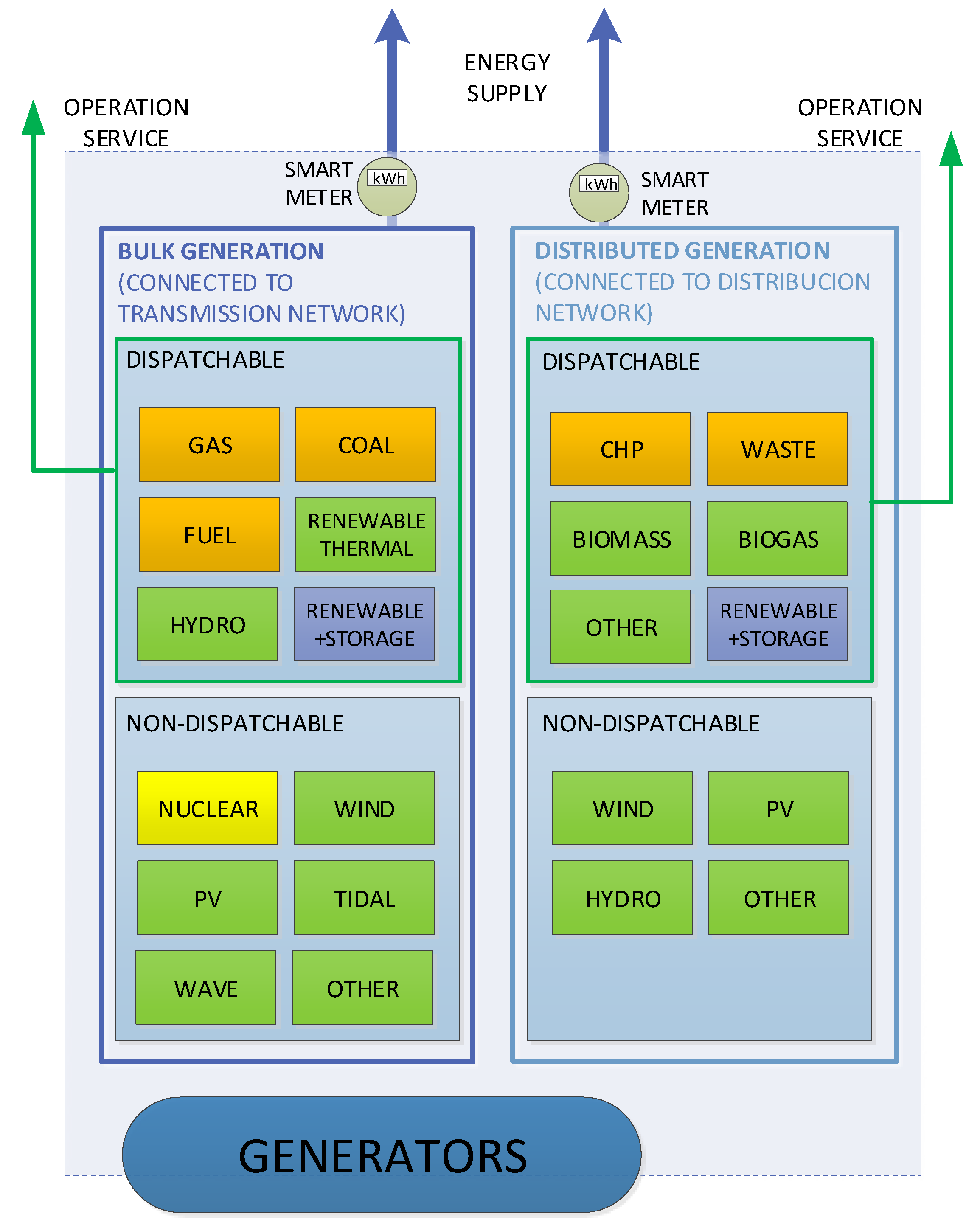

In addition to the generators and turbines, the generation plants have the control and communication systems to ensure the correct operation to supply the electricity to the grid in a reliable and secure way. New generators can also own the new assets regarding substations and transmission lines. Traditional generators were large centralized power plants, normally far away from consumers. Now, electricity generation also occurs at the distribution level and lower scales, which is known as DER [

8]. Thus, electricity generators can be differentiated regarding their connection point with the grid (transmission or distribution), size, and dispatchability. Thus, generators can be bulk generators if they have large sizes and are connected to the transmission network, or they can be connected to the distributed network as DER. Moreover, a key characteristic of generating technologies is if they have the capability of varying their power output at will. Therefore, generating technologies can be differentiated in dispatchable and non-dispatchable technologies. It is common today for renewable generators to include batteries in their facilities to operate as conventional generators and provide operation services. Among all technologies, they can also be categorized as renewable (green), non-renewable (orange), nuclear (yellow), and renewable with storage (blue). The most common ones are the following: gas, coal, fuel, Combined Heat and Power (CHP), nuclear, hydroelectric, wind, solar photovoltaics (PV), solar thermal, and biomass. These classifications of technologies based on their connection point, dispatchability, and availability can be seen in

Figure 3.

Generators mainly receive payments for the energy they produce and the operation services they offer. Generators provide electricity to the grid they are connected to (transmission or distribution), and this electricity can be managed by the generators or via a VPP that operates its assets. Regarding the operation services, they also provide them at the network level they are connected to. These services can be provided to the transmission and distribution operators if they meet the system operation service requirements (POS-T, POS-D). Thus, generators produce electricity that they sell in the wholesale market, local market (if connected to distribution), or via bilateral contracts to consumers, VPPs, and storage agents in exchange for economic transactions. Moreover, generators can also provide operation services via markets or contracts with the TSO, DSO, VPPs, and storage, receiving in exchange for them economic transactions. On the other hand, they can also purchase operation services from VPPs and storage agents. Finally, generators may pay fees for participating and using Wholesale Electricity Market (WEM), LMO, and the transmission and distribution grids (if connected to them).

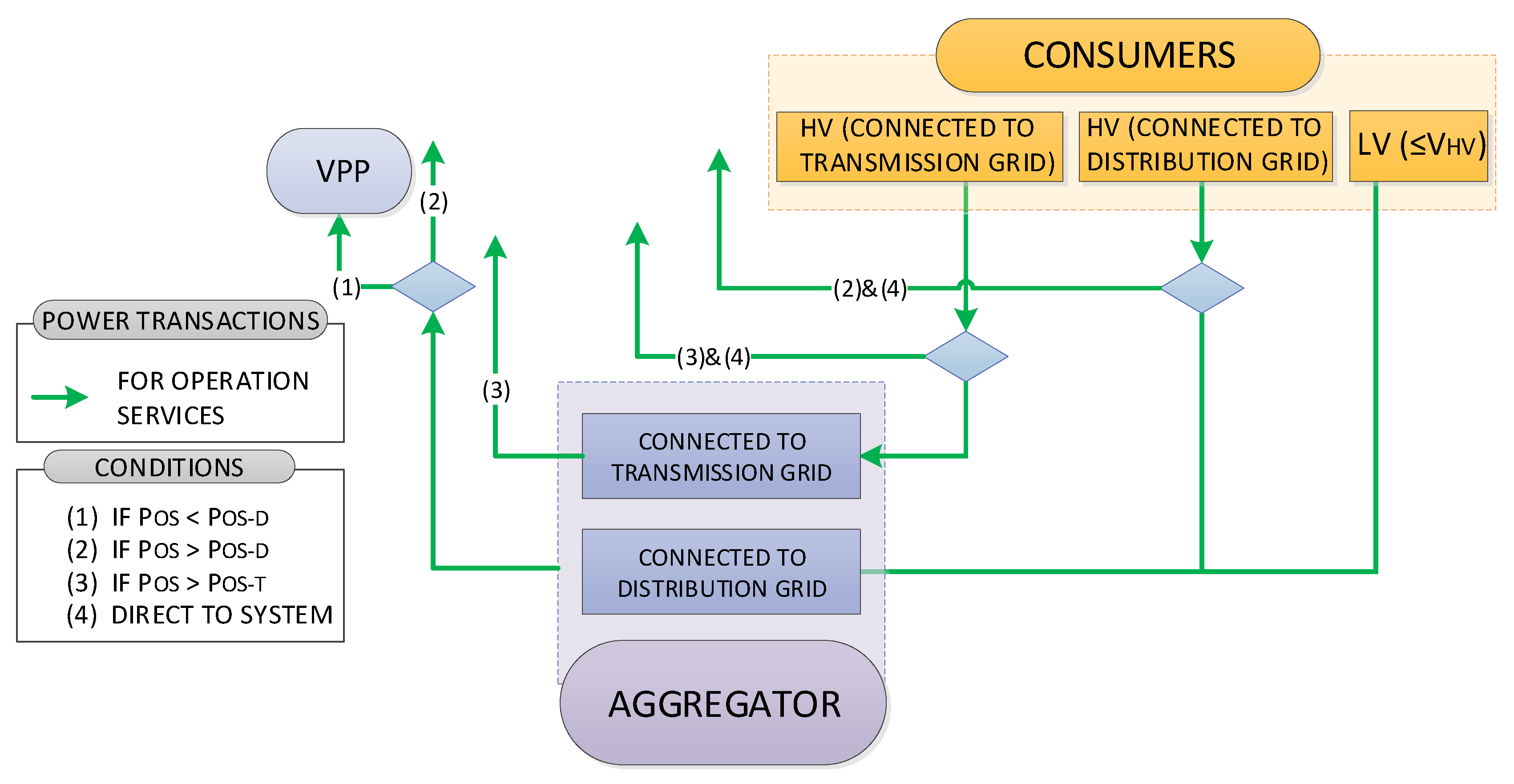

3.3. Virtual Power Plants (VPPs)

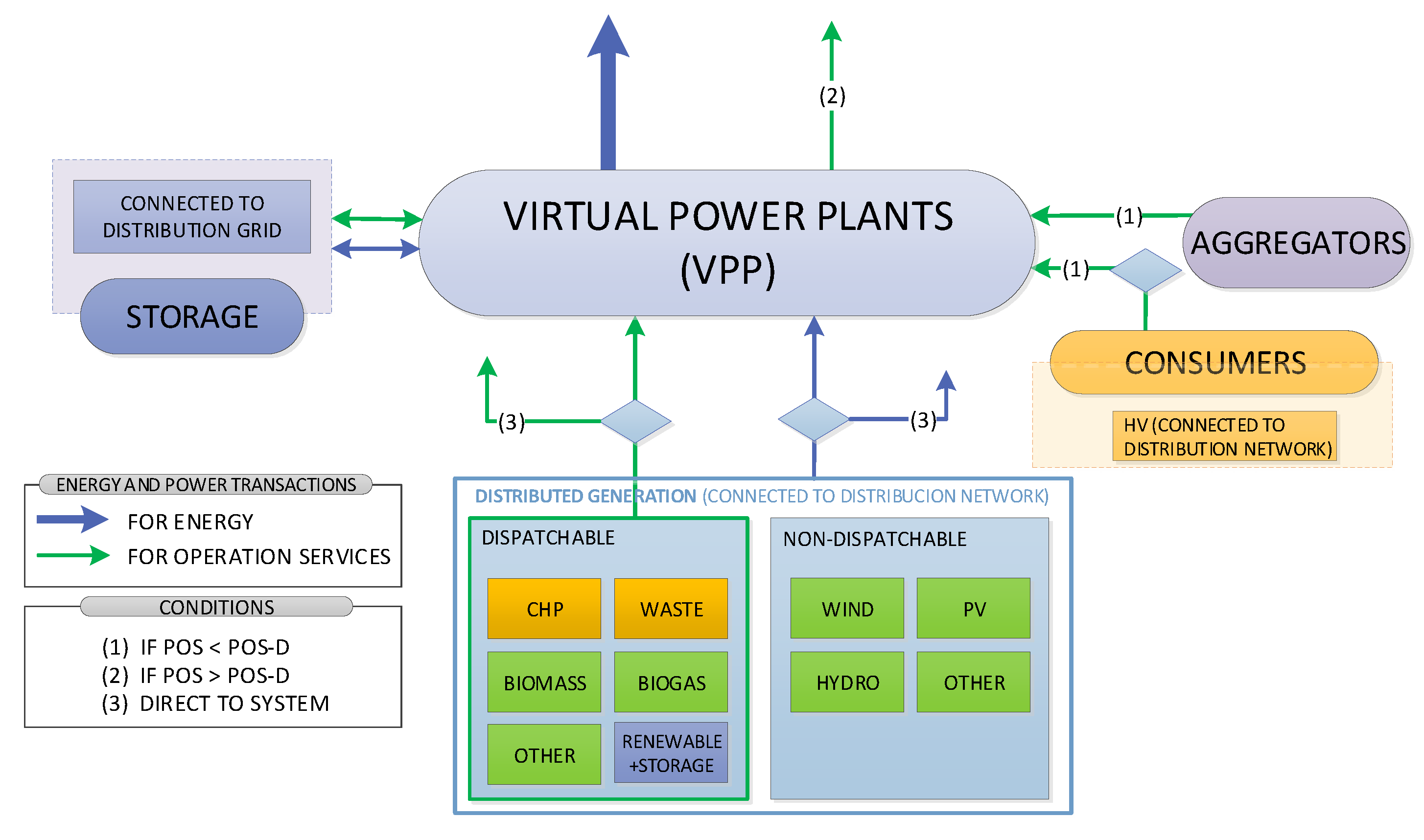

VPPs are defined as an entity that integrates small and geographically distributed generators connected to the distribution system with the objective to provide firm and tradable generation.

VPPs integrate small and disperse generation to perform as a single entity in the wholesale market and power system [

25]. Therefore, VPPs behave as a traditional generator in the system, providing energy but also operation services. VPPs help small generators, usually with no control capability, to become a viable and fully qualified generator in the market. The VPP provides this control capacity for them (primary and secondary reserve and voltage regulation) so that they can compete in energy and operation services and markets. The generation resources included in one VPP can easily be modified or switched on or off providing the required flexibility for operation purposes. This flexibility can also be obtained from the DRR by interacting directly with large consumers or through demand aggregators for small and medium-size demand resources. Energy storage may be also a key asset when providing VPP services.

The generators belonging to a VPP are usually spread out over a limited geographical area. The basic activities, relations, and minimum conditions in the framework of the proposed model are shown in

Figure 4.

VPPs agents may own or control generators such as renewables, cogeneration plants, traditional thermal generators, or storage systems. Moreover, VPPs need to have the same communication and control needs available as the traditional generators. These requirements should be more complex due to the fact that the VPP has to control large amounts of very distributed resources downstream and, in some cases, very small amounts according to their rated power. Therefore, their communication and computing systems have to be more complex to participate in energy markets.

Regarding its transactions, VPPs interact with many agents. VPPs buy electricity from DG generators connected to the distribution grid and storage agents, or from the local energy market. VPPs sell the electricity to the different markets (wholesale or local). Regarding operation services, VPPs purchase them from medium consumers connected to distribution, aggregators, and storage facilities. These are offered to DSO (if they are larger than POS-D), TSO (if they are larger than POS-T), or to other generators via bilateral contracts. Regarding their economic transactions, VPPs purchase electricity from generators and storage to sell them. Bilateral contracts can also be established between VPPs and consumers, retailers, or storage. Between storage and VPPs, bidirectional energy flows may exist. Finally, VPP agents receive payments from the TSO, DSO, and generators after providing the above-mentioned services. In order to obtain these services, VPPs have to purchase them from consumers, aggregators, and storage systems. The VPP is not supposed to pay any fee for participating in the market or using the transmission or distribution grids, as these costs will be translated to the generators that they operate or the consumers that buy electricity from them.

3.4. Aggregators

An aggregator is an entity that groups different consumer agents of a power system to represent and operate them as a single agent that participates in the operation service markets [

40,

50].

Its main activity is to put into value for the system the small customer demand response resources that, when independently considered, are not valuable for other network operators. Thus, they unlock potential resources based on economies of scale [

39]. The aggregator manages the customer demand by clustering small (a few kW) demand resources with similar characteristics, or combining them to provide valuable resources to the operator, in terms of size, duration, advance notification time, etc. These products are able to compete in quality and price with those offered by other actors like generators. One special type of aggregator activity is the electric vehicle charging management, which manages the EV load charging process (and discharging) in a specific EV concentration point or area, with the objective to manage this special and flexible load and to provide additional storage to the system. Aggregators are also responsible for managing the small generation so that they can offer DRR products combining load and generation. The aggregator requires tools to evaluate the individual consumer response (or in low aggregation levels as in the case of residential customers) so that it may evaluate and foresee the main parameters of the customer response such as reduced power, duration, up and down ramps, etc. Then, it may proceed to the associated settlement when the transaction is completed. In addition, aggregators may also implement on/off control for small generators.

The basic activities, relations, and minimum conditions for the aggregator in the proposed model are shown in the

Figure 5.

The aggregator’s main components include an extensive communication facilities system and computational capability. The first has to provide fast and reliable performance, and the second needs to properly receive the requests from the network operators and respond to them using suitable resources without compromising the customer requirements and expectations.

The aggregator’s main clients are VPPs, DSO, and TSO, to whom they provide operation services and power in exchange for economic payments. These operation services are provided according to the minimum required levels at distribution (POS-D) and transmission (POS-T). Moreover, they may also offer their services to other actors such as energy suppliers (retailers) and generators so that they may balance their buy/sell portfolio if necessary. Since all their resources come from consumers, aggregators have to pay consumers for their resources. These economic incentives that they have to provide are crucial for the seamless operation of this agent and to unlock the disaggregated opportunities.

3.5. Storage

This agent consumes and generates electricity and has the ability to store it for using it afterward.

Storage is rapidly becoming a key technology in energy systems. Storage systems can help balance and flatten the electricity load profile. They are characterized by very fast responses, which provide storage with the capability to efficiently deliver operation services such as frequency response, black-start capability, load following, or capacity mechanisms [

51]. Additionally, storage can participate in the wholesale market, leveling the load, competing with other peak power plants [

52], and balancing short-term deviations. Storage was pointed out as one of the key factors to ensure reliable large renewable penetration in power systems [

4], mainly because of its ability to balance the excess and deficit of renewable production, thereby avoiding curtailment and also helping the system operator.

This agent has the capability to store energy in other forms such as thermal, potential, mechanical, or chemical. This includes technologies such as pumped hydro, flywheels, molten salts, hydrogen, and electrochemical batteries [

53]. The storage agent also has to have available information and control systems to be allowed to participate in the electricity market.

The storage agent implements power and energy transactions with the grid it is connected to (distribution or transmission). If connected to the transmission grid, storage injects and absorbs electricity from the grid to perform its activity and provide operation services with a minimum power (POS-T) to the TSO that manages the transmission grid. If connected to the distribution grid, the storage may exchange power and operation services with a minimum size (POS-D) not only in the distribution grid and the DSO but also through VPP. These could be implemented through bilateral contracts, which can occur for aggregating capacities to better participate in the markets. With respect to economic transactions, storage can receive payments from the wholesale market, local market, and VPPs for the energy sold. It can also receive payments from the TSO, DSO, VPP, and generators for operation services. Storage can also buy electricity from the wholesale market, local markets, and VPPs, and it may have to pay for the associated fees of markets and grid assets.

3.6. Transmission System Operator

This agent ensures the correct operation of the transmission system. Its main activities are to guarantee secure operation of the power system. This agent has to obtain the resources to operate the network not only from traditional generators but also eventually from VPPs, large customers, and storage as proposed in the architecture. To do so, the TSO needs information that is provided by the WMO, transmitter, and other agents connected to the transmission grid. The TSO is committed to balancing the system and identifying network restrictions, which requires a reliable monitoring and control capability either for committed generators or VPPs and, eventually, demand response resources, directly managed or through aggregators. These control signals require fast and reliable communication.

For doing so, the TSO needs to have assets to ensure the information and measurements flow is available, regarding the operation of the transmission network through a control center. The communication and cooperation between a DSO and TSO are essential in this new conceptual architecture. Furthermore, the TSO also has to manage exchanges with other power systems considering the capacity of the interconnections.

In the proposed model, the TSO has to also consider the use of resources to operate the transmission network not only from traditional generators but also eventually from VPPs, large customers connected to transmission, and storage. All these operation services require a minimum but homogeneous power (POS-T) for all participants that is determined according to the size of the system. Agents need to fulfil these requirements to compete in equal conditions. The TSO rewards economic payments in exchange for operation services to generators, VPPs, aggregators, storage systems, and consumers connected to the transmission network. As the main beneficiaries of the reliable and secure operation of the transmission grid are consumers, they pay the maintenance of the TSO via fees.

3.7. Transmitter

This agent is in charge of carrying the electricity from the bulk generation to the distribution system. The activity that it performs is to transport the electricity throughout the assets that it owns. Moreover, the transmitter has to plan and build (usually in a regulated framework) new lines, as well as reinforce the ones to account for future demand perspectives. It also verifies the connection procedure of new-generation capacity.

This agent has a physical infrastructure between the large generators and the distribution grid or large consumers. This includes high-voltage transformers and transmission lines.

This agent is highly regulated since it is a natural monopoly [

54]. Therefore, the only transactions of this agent are the received fees from generators, storage, and consumers. The users of the transmission system bear the costs of its maintenance and modernization via taxes.

3.8. Distribution System Operator

This agent refers to the entity in charge of ensuring the operation of the distribution system. The DSO plays the important role of managing the distribution system. Moreover, since distributed generation is usually embedded in the distribution system, the system behavior increases in complexity (direction of energy flows, distribution operation constraints, etc.). To account for this situation, the DSO needs to have the necessary resources, which come from the customer resources directly operated or, if desirable, through aggregators. The following new roles that DSOs realize are of extreme importance:

Enhancement of the competition and usage of different local resources to manage technical constraints at a distribution level, allowing the optimization of network planning and solving congestions at the distribution level [

55].

Provision of the forecast and availability of flexible resource to both TSO and local market operators, helping both to accurately predict and contrast the reliability of the resources [

56].

Improvement of power quality monitoring and control strategies associated with the inclusion of distributed energy generation at the distribution level [

57].

Therefore, this agent needs to have assets to ensure the information and measurement flows are available regarding the operation of the distribution network, allowing the detection or prediction of undesirable conditions (current flows or voltages), and finding the resources to cope with the situation. According to this fact, fast and reliable communication channels with the TSO, aggregators, VPP, and generators connected to the distribution system are crucial. Moreover, they also own control centers to safeguard the operation of the system.

In the proposed model, the DSO has to also consider the use of resources to operate the network, not only from traditional generators but also eventually from VPPs, large customers, aggregators, and storage. All these operation services require a minimum but homogeneous power (POS-D) for all participants that is dictated by the size of the system. Agents need to fulfil these requirements to compete in equal conditions. Thus, the DSO is able to provide economic payments in exchange for operation services to generators, VPPs, aggregators, storage systems, and consumers connected to the distribution network. On the other hand, since the beneficiaries of the safe and secure operation of the distribution grid are consumers connected to the distribution, they pay for the maintenance of the DSO via fees.

3.9. Distributor

This agent is in charge of carrying the electricity at the final stage of the delivery, between the transmission grid and the final consumers connected to distribution.

Traditionally, the only objective of this agent was to provide the physical infrastructure between the transport grid and the final consumers. However, its activities are now larger due to the amount of information that they manage generated by smart meters. Therefore, it became an information provider too, since it manages all the telemetry and metering infrastructure. This agent as traditionally highly regulated since it was considered a natural monopoly [

54]. Nevertheless, efforts to make the sector more competitive are arising [

58].

A new critical activity for the distributor is as the “information provider”, being responsible for gathering measurements and other information of the rest of the agents so that they may evaluate the response. For doing so, the distribution agent owns a large number of physical assets. Among them are medium- and low-voltage grids, transformers, and consumer’s telemetry equipment; the distributor also owns a large advanced metering infrastructure (AMI) that collects large quantities of information. After this, thanks to a measured data management (MDM) system, all this information is filtered, processed, and organized in order to obtain valuable information for the correct functioning of the system.

The entities in charge of this agent have to maintain, monitor, and improve the physical assets and provide the collected information. Therefore, the only transactions of this agent are received fees from generators, storage, and consumers. The users of the distribution system bear the costs of its maintenance and modernization via taxes.

3.10. Wholesale Market Operator

This agent is an entity that provides a service, whereby the offers to sell electricity are matched with bids to buy electricity, ensuring the balance between them [

59,

60].

The main objective is to ensure the correct and transparent functioning of the economic transactions associated with the power sector, as well as organizing the different electricity markets, including wholesale, future markets, and the collection of all the bilateral contracts over the counter (OTC) that have an impact on the system. This information has to be provided to the TSO to ensure the correct functioning of the system.

The WMO is an independent actor in liberalized frameworks, strictly regulated. The WMO is characterized by a trading platform that it controls in order to manage all the bids to buy and sell products. One of its main tasks is to couple the market by matching the sell and buy offers.

Regarding transactions among agents, the generators, storage, and the consumers bear the costs associated with the WMO, paying the fees directly or via a third party. Regarding energy transactions, a minimum level for buying (EW-B) and selling (EW-S) electricity in this market is established depending on its size. Generators and VPPs offer electricity in the market and are compensated with cash flows. These come from the retailers and consumers that participate in the market. Storage has the capacity to buy and sell electricity to obtain benefits. Thus, cash flows between storage and the WMO are bidirectional.

3.11. Local Market Operator

Currently, local electricity markets (LEMs) are probably the least developed component of smart grids. The implementation of electricity markets in the last 20 years did not result in a significant reduction in the price ties of the energy or the increment of opportunities for most of the final consumers. Local markets are being designed to bring competitive advantages to these consumers, by implementing local trading (peer-to-peer) either directly or through aggregators and VPPs [

43].

LEMs need to be reliably established to enhance the fair trading for customer-owned renewable generation and flexible resources.

This requires the development and implementation of dynamic and automatic trading platforms, for the negotiation of energy for short periods of time (shorter than the ones applied to wholesale markets) and probably closing a minute before delivery. LME platforms have to offer consumers, aggregators, and VPPs the chance to virtually trade energy services in a geographically constrained area [

61]. These markets complement wholesale markets and bilateral contracts that do not have the capability to react in real time to the myriad of small demand resources and distributed generation [

62]. The LMO manages and operates the LEM from an independent perspective, enabling a more dynamic trading of electricity.

Its main activity is to promote the diversity and competitiveness of the market, while ensuring the correct functioning of it by matching buying and selling bids. Furthermore, they have to monitor all the energy transactions to communicate them to the DSO to ensure a reliable operation under the technical limits. This information is provided according to the geographic control area of the DSO associated with the LEM.

The main components that characterize the LMO are the trading platforms that it controls to manage all the bids to buy and sell products. All these agents have to be in a local area and interconnected in a distribution grid. This allows a fast negotiation process and a dynamic response to prices.

Due to its role of market operator, the LMO receives payments from all the agents participating in this market. The local market manages payments among the participating agents; to do so, a minimum level for buying (EL-B) and selling (EL-S) electricity in these markets is established depending on its size. While generators and VPP agents receive payments for the energy traded, consumers and retailers pay for it. As in other markets, the storage has bidirectional energy flows, having the capacity to buy and sell electricity. Finally, consumers, storage, and generators pay an established fee for participating in the market directly or throughout a third party.

3.12. Retailer

Electricity retailers are entities that bridge the gap between consumers and the wholesale markets [

60]. The activities of this agent do not change significantly from the traditional one. They buy the electricity in the market and sell it to their customers. Nevertheless, in the proposed model, the self-generation becomes a common possibility for small customers, being the interaction for these customers directly handled by retailers. These interactions translate in contracts with consumers to absorb the self-generation excess and economically compensate them afterward.

The retailers do not have specific components on their assets. They play a role of intermediary, thus owning strong communication and prediction systems for optimizing their performance.

This agent needs to interact for energy trading with wholesale and local markets. They can also sign these transactions through bilateral contracts with generators and VPPs. For these reasons, they need reliable and secure communication and information channels. Moreover, according to the proposed architecture, retailers are also allowed to interact with customers and aggregators for portfolio balancing purposes, needing for that the capability to interact through dynamic pricing (not control capabilities) with the customers. They are also responsible for implementing the self-consumption or net balance contracting, needing for that information about the customer buying and selling electricity. Retailers are also responsible for paying the fees in representation of consumers to the different market operators. In sum, interactions between retailers are with customers, aggregators, VPPs, generators, and market operators.

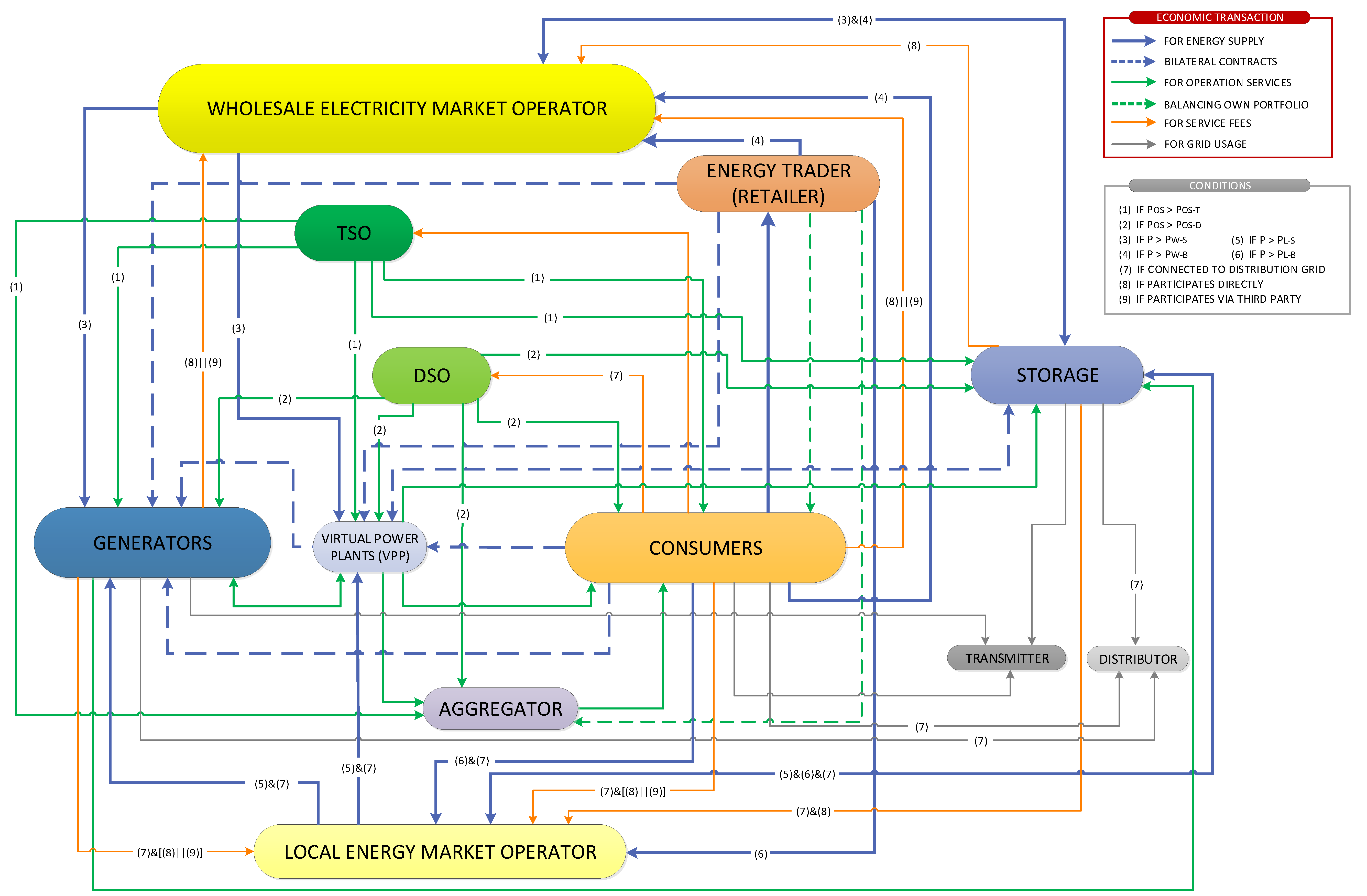

3.13. Conceptual Architecture and Interactions among Agents

The above-described agents establish a series of relationships among them as summarized in

Table 2. More specifically, the figures below map the different interactions that take place in the newly proposed conceptual architecture. Thus, these figures explicitly depict each of the transactions above explained.

Figure 6 shows the transactions among agents associated with the physical commodity (electricity), which can be due to power, operation services, or balancing requirements. The blue arrows show transactions among agents related to energy; for instance, generators can supply power to the grid if they are connected to generation. In contrast, if they are connected to the distribution grid, they can supply its energy to the grid or through a VPP if their capacity is small. Another example can be storage, which has the capability to provide or purchase electricity from the grid. Depending on which grid (transmission or distribution) it is connected to, the energy fluxes will vary. The green arrows represent the operation service transactions. These are related to frequency and voltage control, energy imbalance, or system protection [

21]. It can be seen that these transactions are applied to the transmission or distribution grid, depending on which grid the resources are connected to. Afterward, these operation resources at the distribution level can be managed at higher levels by the TSO thanks to the communication between DSO and TSO.

Figure 7 shows the economic transactions among agents, differentiated depending on if they are associated with an energy supply, bilateral contracts, operation services, balancing of own assets, fees, and grid usage transactions. Thus, blue arrows refer to an economic payment associated with a power exchange, dashed blue arrows show energy bilateral contracts, green arrows represent payments related with operation services, green dashed arrows represent payments for balancing portfolios or demands, orange arrows represent fees, and gray arrows represent taxes for the usage of the grid. For instance, aggregators receive payments for operation services from the DSO, TSO, and VPP, but they pay these operation services to consumers. Retailers buy energy from wholesale and local markets and bilateral contracts with VPPs and generators. Afterward, this energy is sold to consumers that pay for it. On the other hand, the transmitter agent and the distributor agent only receive payments associated with taxes, which are only paid by consumers, storage, and generators, the agents that are considered the final users of the infrastructure. Specifically, only agents connected to the distribution grid pay to the distributor.

Finally, some agents associated with energy services can also balance their own portfolio to optimize their performance in the market. These last arrows can be seen as green dashed lines.

4. Conclusions

This paper presented a novel conceptual architecture for the development of the next-generation electricity markets. The architecture helps unlock all the hidden potential of flexible and distributed energy resources, taking into special consideration the potential benefits for active consumers. The novel architecture was proposed based on the analysis of the shortcomings of the existing models that can be found in the literature. This model provides a path that policy-makers can follow to eliminate barriers to integrate DER in a competitive way at the distribution level.

In this new paradigm with a massive integration of renewables, the need for electricity storage and for enhancing the value of demand response resources forces agents’ services and transactions to appear. The proposed new architecture focuses on agents who enable flexible resources to be exploited such as storage, virtual power plants, and aggregators. These agents are already operating in some systems and emerging in others. However, the model includes the transactions among them based on an ontological analysis. Furthermore, the transactions among the presented agents are separated in energy, operating services, and economic transactions, which were clearly analyzed and described regarding the offered services, taking into account the technical restrictions. This results in a clear proposal of how the future electricity markets could be implemented.

This architecture also presents and characterizes the flexible resources available in the next-generation electricity markets, paving the way for its transactions. This flexibility can be available for two functions: to provide operation services, and the fast and dynamic balancing of electricity consumption and generation at different network levels. Three types of flexibility were shown in the proposed conceptual architecture. Similar to traditional generators, intermittent renewables with batteries are also able to provide flexibility. Consumers with self-generation and batteries can also become a flexible resource for the systems. This also helps them optimize their electricity cost by unlocking resources and allowing them to use their flexibility with an economic purpose. Finally, electric vehicles will also become a major source of flexibility in the system. Even though they are a concrete application, the massive electrification of transport gives as an opportunity to provide flexibility to the system. EVs can be described as consumers with self-generation and batteries if vehicle-to-grid chargers are implemented, or just as flexible consumers if only grid-to-vehicle chargers are installed.

Another novel element is the inclusion of local electricity markets in the conceptual architecture. Currently, these markets are gaining importance and interest due to their capability of reacting to the novel scenario of larger intermittency and decentralized generation at the distribution level. However, their relationships with other agents of the system were not previously studied from an ontological perspective. These relationships were carefully studied and stated. LEMs represent a valuable tool to exchange energy locally in a more dynamic and cost-efficient way for the power system (grid loss reduction). Furthermore, they also present an opportunity for decentralization and enhancement of competition in real time. It is important to highlight the need to have a fast and reliable communication channel between the local market operator and the DSO. The latter provides the technical restrictions that determine under what limits energy can be traded in these LEMs.

Finally, future work should assess the implementation of a case study with the proposed architecture to assess how the model enhances a more competitive electricity market and how agents are integrated in existing systems. It is also necessary to develop a clear cost–benefit analysis of the implemented model to gain knowledge of it. Moreover, simulations of the market behavior under different time domains also remain as a future objective.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}