CSR and Firm Value: Evidence from China

1

School of Economics and Management, Tongji University, Shanghai 200092, China

2

School of Management, Fujian University of Technology, Fuzhou 350118, China

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(12), 4597; https://doi.org/10.3390/su10124597

Submission received: 6 November 2018

/

Revised: 30 November 2018

/

Accepted: 3 December 2018

/

Published: 5 December 2018

(This article belongs to the Special Issue Sustainability in Asian Emerging Markets)

Abstract

:This study attempts to investigate the influence of corporate social responsibility (CSR) on firm value. Drawing upon stakeholder theory and a resource-based view, we argue that corporate social responsibility is expected to positively affect firm value because it helps firms gain positive stakeholder responses. Based on longitudinal data of Chinese manufacturing firms listed at Shanghai and Shenzhen Stock Exchange between 2010 and 2015, we use multiple linear regression to find that corporate social responsibility has a positive relationship with firm value and that the relationship between CSR and firm value is weakened for firms with higher advertising intensity, as CSR by these firms gains negative stakeholder responses. State-owned firms were shown to benefit more from CSR, as CSR by these firms gains positive stakeholder responses for such firms.

1. Introduction

Recently, corporate social responsibility (CSR)—firm behavior that improves the value of stakeholders or society [1,2]—has become a new metric of corporate financial performance. In fact, the percentage of Fortune Global 250 firms dedicating a section of their annual reports and CSR reporting to CSR activities increased from 44% in 2011 to 78% in 2017 (KPMG, 2011, 2017), demonstrating the importance they attach to these activities. However, do these activities create more benefits for shareholders, or do they focus too much on other stakeholders, thereby reducing the value of the company? So far, many scholars across business disciplines such as accounting, finance, management, and marketing have studied this issue from different perspectives, including cost perspective, agency theory, stakeholder theory, resource-based perspective (RBV), and reputation theory [3,4,5,6,7,8,9,10,11]. Some argue that corporate social responsibility should not only be used to improve corporate image, but also as a major competitive strategy. The purpose of corporate strategy is to obtain a sustainable competitive advantage to enable enterprises to achieve sustainable development [12]. Corporate social responsibility can make enterprises gain competitive advantages of low cost or differentiation by obtaining the support of stakeholders, establishing a good image in society, etc. Finally, the corporate social responsibility called corporate sustainability could be an integral part of a firm’s sustainable development strategy, and in turn achieves the joint sustainable development of the corporation, society, and the environment [1,13]. A large number of studies in the past have analyzed the direct link between corporate social responsibility and corporate financial performance. Despite these efforts, whether and how corporate social responsibility is related to corporate financial performance remains a point of contention and debate among strategic management scholars [14,15,16,17]. On the contrary, other scholars believe that CSR activities have a negative net impact on corporate financial performance, because it may represent a pure corporate expenditure in an area unrelated to operation, which reduces the efficiency of the use of corporate resources [9]. In addition, many companies lack the expertise to invest effectively in social undertakings, and top managers may use corporate social responsibility to enhance their personal reputation and promote their career [18,19]. Therefore, companies should make better use of these resources to improve operational efficiency, rather than transfer corporate resources to corporate social responsibility activities [9]. Despite many studies on the topic that have offered both positive and negative accounts of CSR, few firm conclusions can be drawn, except that the literature is divided. To date, research on the relationship between corporate social responsibility and corporate financial performance (CFP) is still largely inconclusive. In this study, we hypothesize that the biggest corporate social responsibility is to realize sustainable development which requires corporations to consider the satisfaction of other stakeholders as well as to be responsible to their shareholders. They should pursue the maximization of the common benefits to stakeholders [20]. In addition, as an important way for enterprises to achieve sustainable development, most research into CSR has been conducted in developed market economies, especially those of America and Europe. As we all know, despite the differences in politics, economy, culture and environment, and ethics as the basis of social and economic development across various regions, there are some similarities. Therefore, we can say that the theoretical and practical development of corporate social responsibility is a continuous process of spreading from the West to the East, from developed countries to developing countries, absorbing various philosophies, theories, and views of different countries, different societies, and different enterprises. However, environmental and ethical concerns have increased significantly in emerging markets, especially in Asia. In China, a series of accidents caused by bad operations have caused the public to think deeply about the social responsibility of Chinese enterprises. Corporate social responsibility (CSR) has become a research topic and hotspot discussed in business and theoretical circles in recent years. Chinese enterprises have gradually attached great importance to corporate social responsibility, and began to instill it into the practice of strategic decision-making [3]. Hence, the sustainability of these countries needs to be further studied [3,18,21].

As mentioned above, the effect of corporate social responsibility on corporate financial performance (CFP) has been debated for decades. Scholars have identified a number of reasons for the failure to reach a consensus on the relationship between CSR and CFP. On the theoretical side, there are several facts such as stakeholder mismatching, theoretical defects, and insufficient definition of key concepts [22,23,24]. More importantly, perhaps there is a lack of understanding of the process of how CSR affects CFP. Most theoretical models assume that there is a direct connection between CSR and CFP. In this paper, we propose an indirect link. In particular, we proceed based on Barnett’s view that the impact of corporate social responsibility on CFP depends on the impact of corporate stakeholders [24]. We are concerned about the role of stakeholders in CSR and firm value. Meanwhile, some methodological problems are attributed to hybrid discovery, such as maneuverability, methodological differences, and model misspecification [25]. For example, they can fail to control for other important variables that are considered to have a direct impact on corporate performance, such as risk, market development, assets, age, R&D investment, and advertising expenditure [26]. In addition, the relationship between CSR and firm value is unclear partly because of institutional concerns. According to a meta-analysis of 119 studies on CSR and CFP [27], few studies have explored the relationship between CSR and firm value in transition economies in emerging markets. As a transition economy in emerging markets, China is different from developed markets in terms of institutional conditions, so it provides a new context for examining the universality of conclusions developed in Western contexts [28,29]. Although CSR topics continue to gain momentum in strategic research [30,31,32], the questions of how and when CSR efforts affect firm value in the context of China are still a major research gap. Hence, there is a high need to penetrate the black box linking CSR and firm value and gain a better understanding of its underlying mechanisms.

To fill in this gap, we ask two research questions: (1) Does CSR positively affect firm value in China? If so, (2) what circumstances can change the influence of the relationship between CSR and firm value. It is said that the continuing controversy has hindered research and further progress. Recognizing that firms benefit differently from CSR contributions, one way to alleviate this uncertainty is to seek boundary conditions that affect the relationship between corporate social responsibility and corporate value, such as key social and political factors. We draw on stakeholder theory and a resource-based view (RBV) as a theoretical starting point for answering these two questions. Accordingly, CSR not only helps firms obtain social and political resources, but also enables them to establish trustworthy stakeholder relationships, trigger positive stakeholder responses, and obtain a positive impact on firm value. In particular, applying the resource dependence theory, we argue that state-owned enterprises will exceed the expectations of stakeholders and get positive responses from stakeholders based on having more political resources, which are more likely to benefit from corporate social responsibility [32,33]. However, opportunistic behavior such as advertising investment may lead stakeholders to reduce or even reverse their positive evaluation of corporate social responsibility, which may harm firm value [8]. In addition, these ideas have been tested in the context of emerging markets—China—while previous studies have mostly been conducted in the context of developed markets, such as the United States and Europe. Although the theoretical arguments discussed in this study are quite general, China has provided a useful socio-political background to expand these arguments and test them in a profound and meticulous way. Due to the uniqueness of China’s market and institutional environment, we may find that some specific factors that may be related to the relationship between corporate social responsibility and corporate value here are quite different to those elsewhere [3]. Besides this, although China is undergoing economic transformation, enterprises in China still rely heavily on the government. For example, government resources, as a strategic resource for firms, may be especially important because formal institutions can lead firms to rely more on informal mechanisms [34,35,36].

In this paper, we use a fixed-effect model with panel data to solve the problem of model misspecification and examine whether and under what conditions CSR will affect firm value. More specifically, we study whether CSR activities are more valuable when they are carried out by companies that invest heavily in advertising and are controlled by the government. In particular, we provide theoretical and managerial contributions. Theoretically speaking, this paper discusses the role of corporate social responsibility in corporate strategy. Based on the general idea that corporate social responsibility contributes to the acquisition of social and political resources, we have identified two mechanisms, namely, influencing the response of stakeholders and obtaining political support. These two mechanisms form the basis of the relationship between corporate social responsibility and firm value. These findings help us to establish a stronger theoretical basis for the relationship between corporate social responsibility and firm value. Secondly, we find that corporate social responsibility improves the value of a company in some cases, but in other cases, it may undermine the value, indicating that some companies adhere to the shareholder model while others may consider broader objectives [8]. Managerially, there has been debate as to whether firms should engage in CSR activities [3,4]. We believe that CSR not only conforms to traditional Chinese values, but also helps Chinese firms to obtain scarce resources and political support from the government. This shows that Chinese managers’ input in corporate social responsibility is helpful. However, we further prove that Chinese firms do not all benefit from corporate social responsibility as well. Stakeholders respond more negatively when they realize that companies do too much advertising in addition to participating in social responsibility. In addition, managers of state-owned enterprises (SOEs) should actively participate in corporate social responsibility because they not only have the innate advantage of obtaining more political resources, but also have greater marginal effects than non-state-owned enterprises in terms of obtaining positive stakeholder responses.

This paper proceeds as follows. In the second section, we describe the theoretical model and develop hypotheses for empirical testing. Section 3 describes our data collection procedure and variable construction and outlines the empirical method used to investigate the hypotheses. The fourth section gives the results of the empirical analysis. The final section concludes and discusses interesting implications and the limitations of the findings.

2. Theory and Hypotheses

2.1. CSR and Firm Value

A growing body of studies has examined the relationship between CSR and firm value and showed mixed results [5,37,38,39,40,41,42,43,44,45,46,47,48,49,50,51,52,53]. The early scholars, in the spirit of shareholder theory [9] and neoclassical economic theory, view CSR as a “donation” from shareholders to stakeholders and a competitive disadvantage compared to their unresponsive peers that results in lower profits [53]. Similarly, CSR may be the outcome of an agency conflict between shareholders and managers [54]. Managers’ own best interests may drive CSR. However, other scholars based on the stakeholder theory propose that CSR positively affects firm value [7,8,9]. Some argue that there is no relationship between CSR and financial performance [26] or, if there is one, that it is too complex to be found [6,23]. Due to the limitation of space, Table 1 presents a selected list of empirical studies on the relationship between CSR and firm value.

Yet, there are reasons to believe that CSR is positively related to firm value. In this study, firm value mainly refers to the corporate market value. According to the broad definition proposed by the World Business Council for Sustainable Development (WBCSD 2004), we adopt a definition of CSR from the perspective of stakeholder theory and argue that “CSR is the commitment of a business to contribute to sustainable economic development, working with employees, their families, the local community and society at large to improve their quality of life.” From the perspective of stakeholders, some scholars propose that a firm tries to reduce its implicit costs (e.g., product quality costs, environmental costs) of irresponsible social behavior, which result in higher explicit costs to bondholders and ultimately in a competitive disadvantage. In this vein, CSR positively affects corporate market value as measured by Tobin’s Q [20]. In addition, some researchers link the resource-based view to stakeholder theory. Based on those two theories, researchers insist that a firm can obtain some intangible resources, such as human resources [55] and organizational culture [56], which enable the firm to acquire a competitive advantage over its competitors [57] by having a close relationship with key stakeholders. More recently, strategy scholars have linked CSR to firm value on the basis of corporate reputation theory [10,11,58]. They propose that strong reputations for CSR will be able to help preserve firm value. In short, there is generally a positive correlation between corporate social responsibility and corporate value when examined from stakeholder theory, RBV, and reputation theory. Different from the traditional view, they focus on not only the economic but also the social and political consequences of firm behavior [59].

In China, the economy is undergoing a transformation from centralization to marketization, and the institutional conditions are not well established [6]. In this case, political connections play a very important role and can be critical to their sustainability and success [6,60]. Some propose that CSR is a signal to the government that corporations are sincere in dealing with the related stakeholders, which may enable Chinese firms to obtain government support and favorable policies to achieve their financial goals while helping to deal with such political uncertainty [61]. The government can reward firms that make such contributions with tax benefits, access to bank loans, easier project approval, and higher recognition and status for the owners [62,63]. Furthermore, CSR may also generate some future government policy decisions favorable to the firm [63]. When governments do not have enough resources to engage in social welfare projects, CSR is more especially appreciated, because those contributions help lighten their burdens [64].

In addition to obtaining political support, Chinese firms are more influenced by their stakeholders [65,66]. As we all know, Chinese are deeply influenced by traditional Chinese philosophy such as Buddhism, Daoism, and Confucianism. Buddhists emphasize that compassion is the main virtue of life [3,67]. Taoism emphasizes that people should be aware of the needs of others. In Confucianism, people who spread bounty or save people are considered saints. These traditional Chinese philosophies shape China’s social values and have a far-reaching impact on Chinese enterprises. This is consistent with the latest research in stakeholder theory and related literature on corporate social responsibility, which shows that corporate social responsibility can be used as a strategic method for stakeholders to manage their impact on overall objectives [10,68,69]. In this vein, companies can build better relationships with their major stakeholders [70] and then generate positive responses through CSR [19,68]. Corporate social responsibility can not only promote employees’ perception of organizational identity, but also improve the company’s image and reputation, increase the value of its “moral capital”, and even extend to other aspects of business operations such as improving product quality and customer satisfaction [71].

In short, influenced by traditional Chinese values and modern social and political factors, all stakeholders of firms take a positive attitude towards corporate participation in social responsibility and respond to CSR with greater cooperation and support. In addition, the Chinese government and local authorities are more willing to recognize these companies by seeing them actively engage in social welfare activities and providing them with key resources when they need them [64,72]. Finally, we predict that the overall relationship is a positive one. We therefore hypothesize the following:

Hypothesis 1.

Corporate social responsibility positively affects corporate market value.

2.2. The Relationship between CSR and Firm Value in China: Some Contingencies

As mentioned above, CSR can help firms gain social and political support which is then positively related to firm value, but the impact of CSR on firm value is still not universal. The main purpose of this paper is to examine under what kind of circumstances the relationship between corporate social responsibility and corporate value will be affected. We focus on the above mechanisms—stakeholder responses—to propose that different business environments and firm characteristics may contribute to those differences. In this study, we examine the potential moderator variables—advertising intensity and state ownership—on the relationship between corporate social responsibility and firm value.

Advertising intensity. Some recent research has shown that CSR functions as a differentiating mechanism that can take the place of advertising. In China especially, many people hold that CSR could be a way of advertising and greenwashing for companies. Drawing on this logic, some researchers found that advertising negatively affects the relationship between corporate social performance and corporate financial performance [73]. As mentioned above, the mechanism of stakeholder responses illustrates the effect of CSR on firm value. That is, when a firm undertakes social responsibility and advertises heavily, such advertisements will be regarded as a redundant means and corporate social responsibility activities as a kind of cover up for their improper behavior, which may elicit a negative stakeholder response. Intuitively, stakeholders should know more about a company and the information related to CSR activities in order to respond correctly in order to gain more benefits from CSR. However, this is not applicable in China’s manufacturing industry. Because external stakeholders such as suppliers and customers are not direct beneficiaries, they may simply be unaware of the true extent of CSR activities [29]. When the advertising intensity is too high and stakeholders react negatively, enterprises will not be able to benefit from participating in corporate social responsibility. Obviously, intensive advertising has attracted more attention from existing and potential customers as well as potential employees [74]. However, all reactions are negative when the reaction of stakeholders is negative. Then, companies that do more advertising are likely to reduce the impact of CSR. These arguments apply to more and more Chinese firms that regard advertising as greenwashing.

In this vein, we suggest that the influence of CSR on firm value will become weaker when firms have higher advertising intensity. Therefore, we propose the following:

Hypothesis 2.

The positive relationship between CSR and corporate market value is moderated by advertising intensity. Specifically, this relationship becomes weaker when firms have higher advertising intensity.

State ownership. Although non-state-owned firms have exploded since the 1980s in China, as a centralized country, state ownership still has an overwhelming advantage. In the case of the immature market economy, political support is still an important factor that Chinese enterprises must consider when maintaining sustainable development [72]. State ownership has eased this problem to a certain extent. Resource dependence theory emphasizes that the survival of an organization requires it to absorb resources from its surroundings, and it needs interdependence and interaction with the surroundings to achieve its goal. In this vein, firms can improve their long-term financial performance by using the relationship with the government to reduce the risks and uncertainties associated with changes in government policies and regulations [32,60,74]. Because of the preferential treatment in terms of inputs and access to product and capital markets [75], the managers of firms with state ownership generally do not need to worry about political access as much as the managers of non-state-owned firms do. For example, Kaufmann (2003) concluded that state-owned firms have more secure property, greater contractual rights, and closer government relations while non-state-owned firms have less secure property and contractual rights [76]. As a result, state-owned firms obtain significant advantages and show better development. On the other hand, state ownership can also generate positive stakeholder responses. In China, state ownership is a natural signal that stakeholders will spontaneously take to mean that these firms have political advantages, which, in turn, will attract more attention from stakeholders. Generally speaking, non-state-owned firms are usually considered to participate in more CSR activities in order to alleviate their disadvantages and obtain public favor and government support to reduce their uncertain risks by CSR, while in the case of state ownership, rare resources are acquired by political access. In addition to the inherent advantages of having more political resources, if state-owned firms participate more in CSR, it will exceed the original expectations of stakeholders and bring more positive stakeholder responses, such as providing more cooperation and support which tend to improve the value of the company.

The above argument suggests that the firm value will be higher for state-owned firms than for non-state-owned ones. We therefore hypothesize the following:

Hypothesis 3.

The positive relationship between CSR and corporate market value is moderated by state ownership. Specifically, this relationship becomes stronger for state-owned firms than for non-state-owned ones.

3. Methodology

3.1. Data and Sample

Our initial sample included the listed manufacturing firms from the Shenzhen and Shanghai stock exchange over the period between 2010 and 2015, obtaining 1720 listed manufacturing firms. There are several reasons for choosing manufacturing. First, a sample within the same industry can ensure that the external environment faced by the sample is consistent, which can more accurately measure the internal factors on company strategic decision-making. Second, according to the industry classification indicators of 2012, manufacturing firms accounted for 60% of listed firms in China, showing the important position of manufacturing firms in China. Finally, the CSR of manufacturing firms is easy to measure. In addition, the reasons why we chose data for 2010–2015 are as follows: First, CSR activities of Chinese enterprises began to rise after the Sichuan earthquake in 2008, and empirical data on CSR began to be disclosed after 2009. Therefore, we chose 2010 as the starting point of our research. Secondly, considering the lag of the impact of CSR on firm value, our firm value data lags behind CSR data by at least one year, and corporate financial data has not yet been disclosed for after 2017, so we finally selected 2010–2015 as the time window for our study.

We employed three databases as follows: the China Stock Market and Accounting Research Database (CSMAR), comprising the financial data used for our moderators, dependent variable, and control variables; the website of Hexun.com, providing the CSR scores of listed firms as our independent variable; and the National Economic Research Institute (NERI), where we obtained the indices of market development as one of our control variables. A total of 7899 observations were finally obtained after removing the outliers and missing values.

A lag often exists between CSR activities and their impact on firm value, so the main effect of CSR on firm value was evaluated using Tobin’s Q for the year in which CSR activities were implemented.

3.2. Measures

Dependent Variable

Tobin’s Q is commonly used as the proxy for firm value accounting for companies’ market-based financial performance. Referring to the measurement by Kaplan and Zingales (1997), we employed Tobin’s Q as our dependent variable, calculated by adopting the market value of equity added to total liability and subtracting deferred tax expense, then dividing by total assets [77]. This measurement is also theoretically and empirically equivalent to other two indicators—return on asset (ROA) and market-to-book ratio—by their reflection on the firms’ financial performance [78,79].

Independent Variable

We took CSR as our independent variable. Based on the annual reports of listed enterprises in China and corporate social responsibility reports published by official websites, Hexun.com has a professional corporate social responsibility evaluation system that has been regarded as the latest and most authoritative database with an adequate rating data towards CSR [80,81]. Our research also adopted the comprehensive score of CSR published by Hexun.com, ranging from 0 to 100.

Moderating Variables

Advertising intensity and state ownership were selected as moderators to explore the boundary conditions of the main effect of CSR on firm value.

Advertising intensity. The extent to which enterprises promote their image might affect the way people think of their motivation and thus has an impact on the process of how CSR might influence their firm value. For this reason, we described the willingness of a firm to spend on marketing and selling behaviors, then employed advertising intensity as a moderator in our model which was calculated as the ratio of SG&A (Selling, General, and Administrative) to sales [26,68,82].

State ownership. Although the reform and opening-up policy have led to partial privatization of some state-owned firms, state ownership is an important figure to characterize economic performance in China [83]. Our research adopted state ownership as a dummy variable to explore whether it has a moderating effect on the relationship between CSR and firm value. We coded it 1 if the ultimate owner of a firm was the Chinese state and agencies; otherwise, we coded it 0 [75].

Control Variables

At the organizational level, firm size, firm profit, age, capital output, ownership concentration, abundance of cash flow, and slack resource were controlled for. At the level of external environment, we included market development and the subdivision of manufacturing industries in our model.

Firm size, playing a significant role in the relationship between a firm’s social and financial behaviors [4], was measured by total assets at the end of the fiscal year to reduce the impact of the deviation of companies with extreme scales, taking the natural logarithm.

Firm profit, measured as the net profit at the end of fiscal year, taking the natural logarithm, was also an important indicator of the scale of a firm. Both firm profit and firm size were relevant to our models since tiny enterprises might not behave overtly to respond to society as large enterprises might [84]; thus, they would pay less attention to their stakeholders and, finally, would earn less.

Firm age was defined as the number of years since the firm’s initial public offering (IPO). With the effect of organizational inertia, firm age might be thought to affect their performance [12].

Capital output, measured as the firm capital expenditure at the end of the fiscal year, taking the natural logarithm, reveals a firm’s capital structure. There is a close relationship between capital expenditures and company value, reflecting the success of R&D that can bring future benefits to the company, and the portion of R&D that cannot form future benefits [85,86,87].

Jensen and Meckling (1976) believe that an effective way to reduce agency costs is to let managers hold shares, and managers’ shareholdings are positively related to corporate value [54]. Fama and Jensen (1983) believe that the higher the degree of equity incentives, the lower a company’s performance will be [88]. In this case, we employed the concentration of firm’s ownership as one of the control variables, which was related to the managerial discretion of CEOs, measured as the sum of the ratio of shares held by the top ten shareholders.

Abundance of cash flow was measured as the ratio of net operating cash flow to total operating revenue, indicating the firm’s operating capability. The literature has showed that in the real capital market, a firm always faces different financing constraints, and the existence of free cash flow can alleviate the problem of financing constraints. As free cash flow continues to increase, resources that management can arbitrarily increase will rise [89].

Slack resource was calculated as the ratio of cash flow to total assets of the firm, which has been regarded as a vital factor in the enterprises [90]. According to the slack resource theory, McGuire (1990) proposed that better social behavior would result from the allocation of available slack resources into the social domains and thus raise financial outcomes [91].

Market development was measured by the marketization indices from NERI which capture the process of institutional development in all of the Chinese provinces [92].

The subdivision of manufacturing industries of a certain firm was defined as a series of dummy variables to eliminate the effect of specific subdivided industrial character, referring to the Guidelines for the Industry Classification of Listed Companies (2012 Revision).

Table 2 presents the measures of all variables.

3.3. Model Estimation

Multiple linear regression was used in our research to explore the main effect of CSR on the firm value of the listed Chinese manufacturing enterprises. Table 1 shows the definition of related variables. All our models were estimated using the STATA 15 statistical package.

Formula (1) reveals the general proposal of our research. The dependent variable, Tobin Qi,t+1, was measured with one-year lag due to the mechanism of how CSR affects firm value, as our hypotheses mentioned above. , defined as the coefficient of the independent variable CSR, was expected to be significantly positive. State ownership () and advertising intensity () were the moderators. According to the literature mentioned before, we predicted the sign of the interaction term of centralized CSR and advertising intensity () to be negative, while the sign of the other interaction term () was predicted to be positive. , defined as a set of dummy variables describing the subdivision of the manufacturing industry, was added to the formula to control the industrial effect. was the vector of our remaining control variables, composed of market development (), firm size (), net profit (), firm age (), capital structure (), ownership concentration (), abundance of cash flow(), and slack resources ().

4. Results

4.1. Descriptive Statistics and Correlation Analysis

Table 3 presents the descriptive statistics and correlations for the variables in our study. For the 7899 samples, the average CSR score (Mean = 25.763) for the period from 2010 to 2015 was lower than 26, revealing the poor performance of listed Chinese enterprises in terms of CSR. A high level of standard deviation for CSR (SD = 18.84) showed the strong volatility of the social behaviors of firms. The results of correlations were not particularly high, indicating the links between firm value and the remaining variables we adopted and also excluding the collinearity among the dependent variable and control variables.

4.2. Hypothesis Testing

Main Effect

Table 4 reveals the multiple linear regression models estimating the impact of CSR on firm value. The effect of subdivision in the manufacturing industry was controlled throughout the analysis.

Our baseline regression was aimed at exploring the main effect of CSR on firm value. Model 1 included all the control and moderating variables. The coefficients on state ownership (p < 0.001), advertising intensity (p < 0.05), firm size (p < 0.01), capital structure (p < 0.001), and slack resources (p < 0.05) were significantly negative. The coefficients on market development (p < 0.05), firm age (p < 0.001), the concentration of ownership by the top ten shareholders (p < 0.001), and the abundance of cash flow (p < 0.001) were positive and significant. The results above showed that lower advertising intensity, higher level of market development, smaller firm size, older age, lower expenditure of capital, higher concentration of ownership, richer abundance of cash flow, less slack resources, and private enterprises might be attached to a greater financial performance.

Model 2 tested the main effect of the key independent variable, CSR. The coefficient was positive and significant (p < 0.001). This finding supported our hypothesis above, stating that CSR predicted firm value. The relationship was consistent in all of the models. CSR would positively affect firm value.

Moderating Effect

Models 3, 4, and 5 showed the results of the moderating effect of advertising intensity and state ownership on the relationship between CSR and firm value. To avoid possible collinearity toward the interaction terms, we mean-centered the variables involved in the interaction terms by subtracting the mean from each value.

Model 3 tested the interaction between CSR and advertising intensity and supported Hypothesis 2, showing that advertising intensity would weaken the relationship between CSR and firm value. Model 4 examined the moderating effect of state ownership on the main effect. As the regression result suggested, the coefficient on the interaction term CSR*SOE was significantly positive (p < 0.05). Model 5 was the full model including all the interaction terms, showing that the effects of the control and moderating variables were generally consistent across the different models in our research. The coefficients on the key independent variable (CSR) and the interaction term CSR*SOE remained significantly positive, while the sign of the coefficients on SOE, AD, and the interaction term CSR*AD remained significant and negative. This full model did not display the phenomenon of the significance of the variables changing from significant to nonsignificant or vice versa, showing that including all the variables mentioned in our research did not lead to high correlations among the covariates, so the conclusions might be relatively credible.

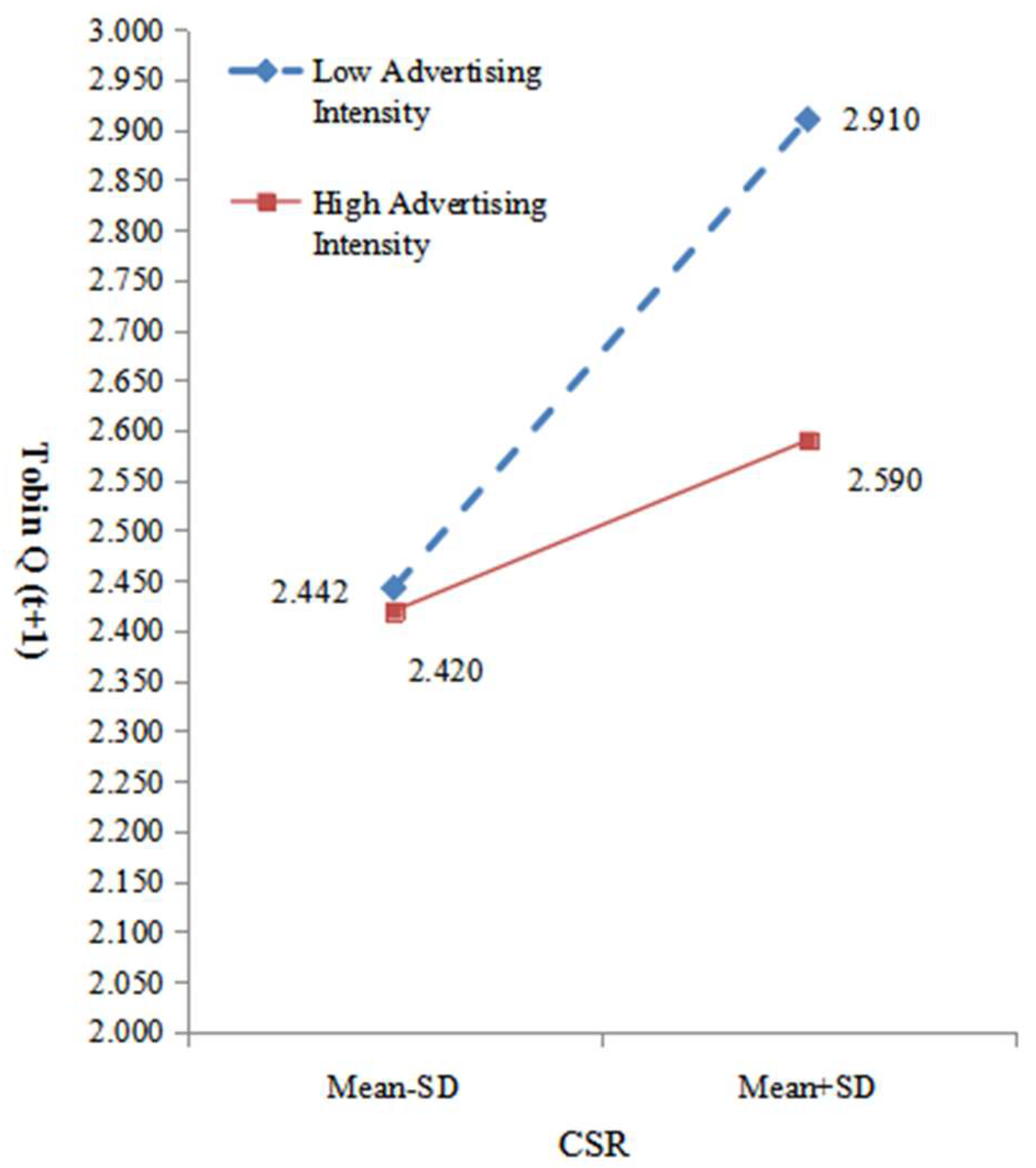

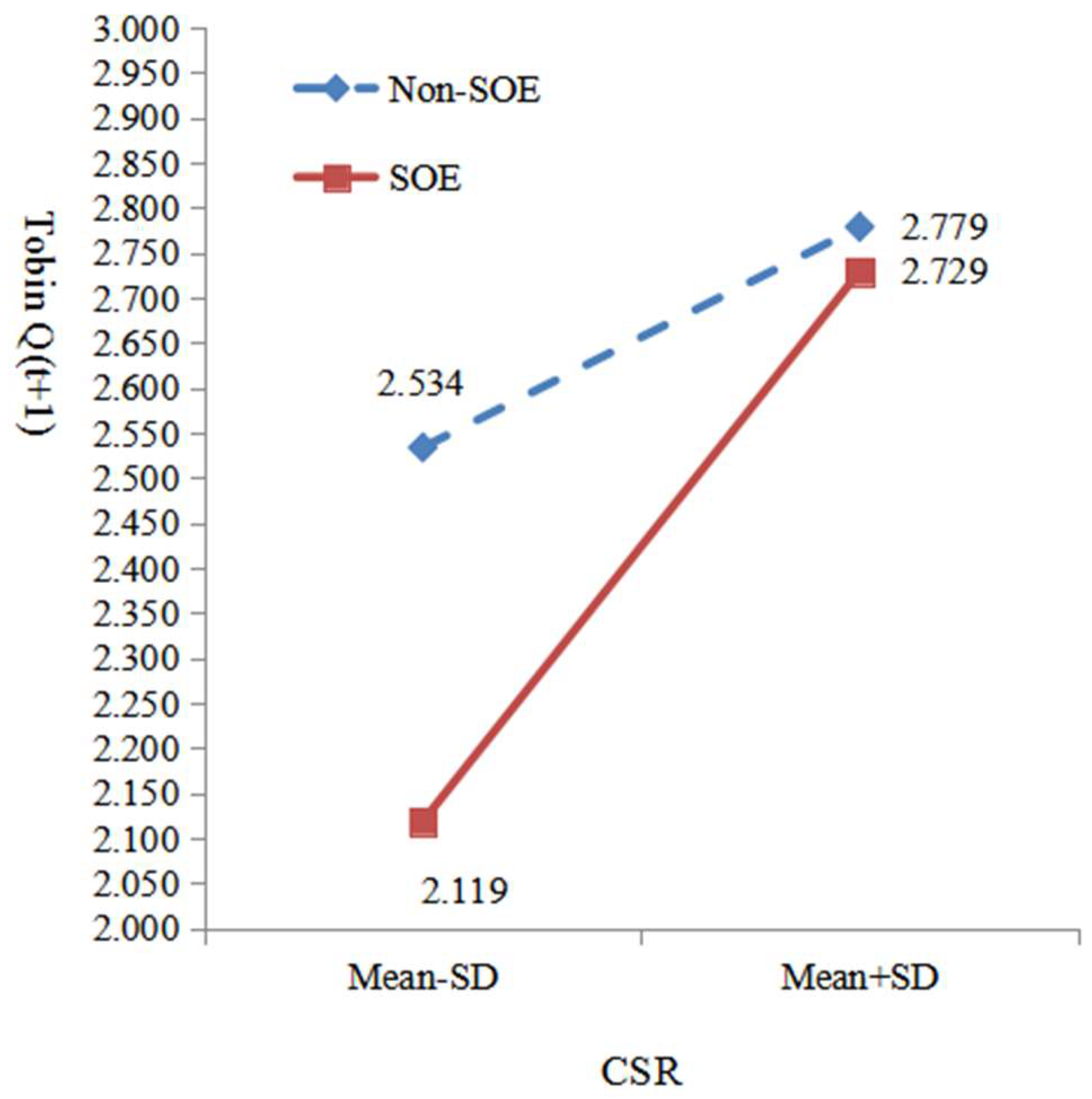

Following Aiken and West (1991), we drew Figure 1 and Figure 2 to illustrate the patterns of the significant interaction effects that supported the hypotheses by using one standard deviation above and below the mean to represent high and low levels of the moderators [93]. Figure 1 showed that the firm value increased much more slowly if a firm’s advertising expenditure was at a high level, proving that the advertising intensity had a negative moderating effect on the relationship between CSR and firm value. Figure 2 suggested that the firm value increased significantly faster when a firm was state owned. In other words, state ownership would positively moderate the main effect of CSR on firm value.

5. Discussion

Corporate social responsibility (CSR) is an important way for enterprises to achieve long-term survival and the joint sustainable development of the corporation, society, and the environment [2]. It conforms to the reasonable expectations of the whole society and can improve the competitiveness and reputation of enterprises. However, most studies on sustainability are conducted in developed market economies, especially in the United States and Europe. Therefore, there is still a limited understanding of prosocial behavior and sustainable development in emerging markets. For several decades, it has been a common wish for scholars to prove whether the financial feedback of a for-profit enterprise would be affected by its engagement in CSR [5]. In China, a relative idea has also been broadly accepted by enterprises that it is necessary for them to both grow quickly and develop sustainably. Meanwhile, how CSR would affect the financial performance of a firm much more efficiently has been paid great attention as well. Plenty of studies in the literature examine the relationship between CSR and a series of outcomes at the firm level. Specifically, the impact of CSR on firms’ financial performance has been causing continuous discussion, though few academics have focused on this relationship in a Chinese context, and studies related to the moderation of this effect are fewer. Our research noticed that defect and designed the study above in response. In this study, we focused on the relationship between CSR and firm value, studying the consequences of CSR, and used advertising intensity and firm ownership as moderators to explore the relationship between CSR and firm value.

In this study, we believe that corporate social responsibility affects corporate value through the mechanisms of stakeholder responses. For instance, when a firm’s employees perceive CSR as virtuous, they will identify strongly with the firm [94], which can promote prosocial behavior [95]. Moreover, companies engaged in CSR practices are likely to promote a good public image which may extend to other aspects of business practice, such as high-quality products and customer service (Adams and Hardwick, 1998, p. 642) which will help gain customer support in turn. In addition, CSR activities may help firms gain political resources that can be critical to their sustainable development and financial success [1,20,71]. In addition, we believe that the positive correlation between corporate social responsibility and corporate value has boundary conditions. The practice of corporate social responsibility should be actively dealt with according to the response of stakeholders and the degree of political support. Using the listed Chinese manufacturing companies on both the Shanghai and Shenzhen stock exchanges from 2010 to 2015, our research explored the relationship between CSR and firm value. As the empirical results showed above, CSR could positively affect firm value, ceteris paribus. Further, the relationship was weakened for high advertising intensity and stronger for firms with state ownership. Both of these results were consistent with our expectation. Feeling that the firms with more kindness were bound to receive greater reward toward their firm value, our research supported this virtuous thought of scholars. Firms with higher advertising intensity might be suspected by the public to promote themselves via different methods including CSR issues, so their CSR behaviors would probably be treated as one of their promotional methods and thus decrease their support from stakeholders. In the case of state ownership, firms with state ownership have certainty of legal status while non-state-owned firms find it more difficult to attain critical factors and capital resources such as debt financing [72]. In addition, state-owned firms will exceed the expectation of stakeholders when they engage in more CSR practices and will elicit positive stakeholder responses. As a result, state-owned firms not only obtain significant advantages and show better development, but can also generate positive stakeholder responses.

As mentioned in the introduction, our research provided some theoretical and practical implications. Few studies in the literature have focused on the theoretical impact of CSR on firm value in a Chinese context, while our research explored it as one of the studies related to this topic. An emphasis on the moderating effect of state ownership and advertising intensity also revealed new findings on specific moderators of the relationship between CSR and firm value in terms of listed manufacturing firms on both the Shanghai and Shenzhen stock exchange markets in China. We propose that advertising is not a way to increase visibility but a method of greenwashing, in contrast with Wang and Qian [24]. They suggested that advertising, as a form of public visibility, positively affects the relationship between corporate philanthropy and corporate financial performance.

Besides this, our study also responds to Nguyen and Johnson’s call for more research into sustainability in emerging markets [96]. In this paper, we focus on the relationship between CSR and firm value based on the role of stakeholder response. This study hopes to become an important stepping stone to further understand the relationship between corporate social responsibility and corporate value. This is also an important supplement to the literature on stakeholder theory. In fact, the debate on whether or not an enterprise should engage in corporate social responsibility has been ongoing for many years [97,98]. We insist that corporate social responsibility not only conforms to Chinese traditional values and generates positive responses from stakeholders, but also helps Chinese enterprises to gain political support. At the same time, we further find that Chinese manufacturing enterprises do not all benefit from corporate social responsibility. When they see too many advertisements from companies engaging in CSR, stakeholders will react negatively, weakening the positive response to CSR. In addition, the marginal utility of state-owned enterprises gained from a unit of extra input such as one point of increase to its overall CSR score might be larger than that of a non-state-owned firm since the strengthening effect on a state-owned firm’s resource advantages could lead to stronger support by its stakeholders at a pretty high level. Therefore, managers of SOEs should take an active part in CSR activities.

We noted several limitations as well. First, we had to shrink the sample size due to the incompleteness of data. Those enterprises with missing information about annual firm value were deleted from the sample set once we found a Tobin’s Q to be missing for any particular year; firms with severe omissions or outliers were also deleted from that same year. Because of this, our conclusions might not be applicable to firms with incomplete financial information across the analysis period. Expanding the sample set from Chinese listed manufacturing enterprises to all of industry in China might also be used to check our results and see whether they are supported or rejected. Although we controlled the subdivision of the manufacturing industry as a set of dummy variables, it did not imply to us whether or how contextual factors of those firms would affect the relationship between CSR and firm value exactly. Since most of the events concerning CSR were highly context-specific, we expected that additional control variables related to the firms’ business, social, and political atmosphere would have significant coefficients [26]. In other words, our conclusions in this research might be overestimated or underestimated but still have some practical implication toward managerial operations. In addition, some vital but unobservable variables might possibly be omitted by our studies to examine both the main effect and moderating effects, which could to some extent affect our conclusions.

Further research could be applied to improve our studies. Generally, the method of estimating the dependent and independent variable could be modified or diversified to enrich our discoveries. The dependent variable, Tobin’s Q, was used as a market-based measure of firm value. However, there is also a consensus that Tobin’s Q might be replaced by the return on asset, ROA, as an accounting-based measure of firm value. Whether our conclusion could remain or be reversed by this replacement might lead to another interesting topic. The strategies of using overall and specific CSR to affect firm value might vary across different enterprises and their operational plans. Comparing the similarities or discrepancies among different estimating methods of our key variables might also provide some unexpected insights from the managerial aspect in the near future. In addition, the sample set of the manufacturing industry could be expanded to many more industries to generalize or modify these conclusions, which could be regarded as a robustness check for our studies. Moreover, the mechanism of the impact of CSR on enterprises’ financial performance could be further explored, especially in a direction that might deal with the endogeneity problem more successfully.

Author Contributions

S.C. contributed to study design. Y.S. and S.G. contributed to data collection and interpretation of the findings. Y.H. contributed to drafting the manuscript. All authors read, revised, and approved the final manuscript.

Funding

This research was funded by Humanities and Social Science Foundation of Ministry of Education of China (Grant No. 13YJA630008).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Korschun, D.; Bhattacharya, C.B.; Swain, S.D. Corporate social responsibility, customer orientation, and the job performance of frontline employees. J. Mark. 2014, 78, 20–37. [Google Scholar] [CrossRef]

- Kotler, P.; Lee, N. Best of breed: When it comes to gaining a market edge while supporting a social cause, “corporate social marketing” leads the pack. Q. Soc. Mark. 2005, 11, 91–103. [Google Scholar] [CrossRef]

- Griffin, J.J.; Mahon, J.F. The corporate social performance and corporate financial performance debate: Twenty-five years of incomparable research. Bus. Soc. 1997, 36, 5–31. [Google Scholar] [CrossRef]

- Orlitzky, M. Does firm size comfound the relationship between corporate social performance and firm financial performance? J. Bus. Ethics 2001, 33, 167–180. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A. meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Trudel, R.; Cotte, J. Does it pay to be good? MIT Sloan Manag. Rev. 2009, 50, 61. [Google Scholar]

- Servaes, H.; Tamayo, A. The impact of corporate social responsibility on firm value: The role of customer awareness. Manag. Sci. 2013, 59, 1045–1061. [Google Scholar] [CrossRef]

- Friedman, M. A theoretical framework for monetary analysis. J. Political Econ. 1970, 78, 193–238. [Google Scholar] [CrossRef]

- Godfrey, P.C.; Merrill, C.B.; Hansen, J.M. The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strateg. Manag. J. 2009, 30, 425–445. [Google Scholar] [CrossRef]

- Muller, A.; Kräussl, R. The value of corporate philanthropy during times of crisis: The sensegiving effect of employee involvement. J. Bus. Ethics 2011, 103, 203. [Google Scholar] [CrossRef]

- Boubaker, S.; Cumming, D.; Nguyen, D.K. Introduction to the Research Handbook of Finance and Sustainability. In Research Handbook of Finance and Sustainability; Edward Elgar Publishing: Cheltenham, UK, 2018. [Google Scholar]

- Wood, D.J. Corporate Social Performance Revisited. Acad. Manag. Rev. 1991, 16, 691–718. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Beyond dichotomy: The curvilinear relationship between social responsibility and financial performance. Strateg. Manag. J. 2006, 27, 1101–1122. [Google Scholar] [CrossRef]

- Ramchander, S.; Schwebach, R.G.; Staking, K.I.M. The informational relevance of corporate social responsibility: Evidence from DS400 index reconstitutions. Strateg. Manag. J. 2012, 33, 303–314. [Google Scholar] [CrossRef]

- Lu, W.; Chau, K.W.; Wang, H.; Pan, W. A decade’s debate on the nexus between corporate social and corporate financial performance: A critical review of empirical studies 2002–2011. J. Clean. Prod. 2014, 79, 195–206. [Google Scholar] [CrossRef] [Green Version]

- Wang, Z.; Sarkis, J. Corporate social responsibility governance, outcomes, and financial performance. J. Clean. Prod. 2017, 162, 1607–1616. [Google Scholar] [CrossRef]

- Galaskiewicz, J. An urban grants economy revisited: Corporate charitable contributions in the Twin Cities, 1979–81, 1987–89. Adm. Sci. Q. 1997, 42, 445–471. [Google Scholar] [CrossRef]

- Haley, U.C.V. Corporate contributions as managerial masques: Reframing corporate contributions as strategies to influence society. J. Manag. Stud. 1991, 28, 485–510. [Google Scholar] [CrossRef]

- Hou, S.; Li, L. Reasoning and differences between CSR theory and practice in China, the United States and Europe. J. Int. Bus. Ethics 2014, 7, 19–30. [Google Scholar]

- Park, J.; Park, H.Y.; Lee, H.Y. The Effect of Social Ties between Outside and Inside Directors on the Association between Corporate Social Responsibility and Firm Value. Sustainability 2018, 10, 3840. [Google Scholar] [CrossRef]

- Wood, D.J.; Jones, R.E. Stakeholder mismatching: A theoretical problem in empirical research on corporate social performance. Int. J. Organ. Anal. 1995, 3, 229–267. [Google Scholar] [CrossRef]

- Ullmann, A.A. Data in search of a theory: A critical examination of the relationships among social performance, social disclosure, and economic performance of US firms. Acad. Manag. Rev. 1985, 10, 540–557. [Google Scholar]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. People and Profits?: The Search for a Link between a Company’s Social and Financial Performance; Psychology Press: London, UK, 2001. [Google Scholar]

- McWilliams, A.; Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strateg. Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Wang, Q.; Dou, J.; Jia, S. A meta-analytic review of corporate social responsibility and corporate financial performance: The moderating effect of contextual factors. Bus. Soc. 2016, 55, 1083–1121. [Google Scholar] [CrossRef]

- Wright, M.; Filatotchev, I.; Hoskisson, R.E.; Peng, M.W. Strategy research in emerging economies: Challenging the conventional wisdom. J. Manag. Stud. 2005, 42, 1–33. [Google Scholar] [CrossRef]

- Wang, H.; Qian, C. Corporate philanthropy and corporate financial performance: The roles of stakeholder response and political access. Acad. Manag. J. 2011, 54, 1159–1181. [Google Scholar] [CrossRef]

- Habel, J.; Schons, L.M.; Alavi, S.; Wieseke, J. Warm glow or extra charge? The ambivalent effect of corporate social responsibility activities on customers’ perceived price fairness. J. Mark. 2016, 80, 84–105. [Google Scholar] [CrossRef]

- Hult, G.T.M.; Mena, J.A.; Ferrell, O.C.; Ferrell, L. Stakeholder marketing: A definition and conceptual framework. AMS Rev. 2011, 1, 44–65. [Google Scholar] [CrossRef]

- Pfeffer, J.; Salancik, G.R. The External Control of Organizations: A Resource Dependence Perspective; Stanford University Press: Palo Alto, CA, USA, 2003. [Google Scholar]

- Meznar, M.B.; Nigh, D. Buffer or bridge? Environmental and organizational determinants of public affairs activities in American firms. Acad. Manag. J. 1995, 38, 975–996. [Google Scholar]

- Hillman, A.J. Politicians on the board of directors: Do connections affect the bottom line? J. Manag. 2005, 31, 464–481. [Google Scholar] [CrossRef]

- Li, H.; Zhang, Y. The role of managers’ political networking and functional experience in new venture performance: Evidence from China’s transition economy. Strateg. Manag. J. 2007, 28, 791–804. [Google Scholar] [CrossRef]

- Marquis, C.; Qian, C. Corporate social responsibility reporting in China: Symbol or substance? Organ. Sci. 2013, 25, 127–148. [Google Scholar] [CrossRef]

- Crisóstomo, V.L.; de Souza Freire, F.; de Vasconcellos, F.C. Corporate social responsibility, firm value and financial performance in Brazil. Soc. Responsib. J. 2011, 7, 295–309. [Google Scholar] [CrossRef]

- Makni, R.; Francoeur, C.; Bellavance, F. Causality between corporate social performance and financial performance: Evidence from Canadian firms. J. Bus. Ethics 2009, 9, 409. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. Corporate governance and firm value: The impact of corporate social responsibility. J. Bus. Ethics 2011, 103, 351–383. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. The causal effect of corporate governance on corporate social responsibility. J. Bus. Ethics 2012, 106, 53–72. [Google Scholar] [CrossRef]

- Guenster, N.; Bauer, R.; Derwall, J.; Koedijk, K. The economic value of corporate ecoefficiency. Eur. Financ. Manag. 2010, 17, 679–704. [Google Scholar] [CrossRef]

- Jiao, Y. Stakeholder welfare and firm value. J. Bank. Financ. 2010, 34, 2549–2561. [Google Scholar] [CrossRef]

- Cui, J.; Jo, H.; Na, H. Does corporate social responsibility affect information asymmetry? J. Bus. Ethics 2018, 148, 549–572. [Google Scholar] [CrossRef]

- Cespa, G.; Cestone, G. Corporate social responsibility and managerial entrenchment. J. Econ. Manag. Strateg. 2007, 16, 741–771. [Google Scholar] [CrossRef]

- Chen, H.; Wang, X. Corporate social responsibility and corporate financial performance in China: An empirical research from Chinese firms. Corp. Gov. Intern. J. Bus. Soc. 2011, 11, 361–370. [Google Scholar] [CrossRef]

- Barnea, A.; Rubin, A. Corporate social responsibility as a conflict between shareholders. J. Bus. Ethics 2010.97, 71–86. [CrossRef]

- Brammer, S.; Brooks, C.; Pavelin, S. Corporate social performance and stock returns: UK evidence from disaggregate measures. Financ. Manag. 2006, 35, 97–116. [Google Scholar] [CrossRef]

- Nelling, E.; Webb, E. Corporate social responsibility and financial performance: The “virtuous circle” revisited. Rev. Quant. Financ. Acc. 2009, 32, 197–209. [Google Scholar] [CrossRef]

- Bird, R.; Hall, A.D.; Momentè, F.; Reggiani, F. What corporate social responsibility activities are valued by the market? J. Bus. Ethics 2007, 76, 189–206. [Google Scholar] [CrossRef]

- Hillman, A.J.; Keim, G.D. Shareholder value, stakeholder management, and social issues: what’s the bottom line? Strateg. Manag. J. 2001, 22, 125–139. [Google Scholar] [CrossRef]

- Harjoto, M.A.; Jo, H. Legal vs. normative CSR: Differential impact on analyst dispersion, stock return volatility, cost of capital, and firm value. J. Bus. Ethics 2015, 128, 1–20. [Google Scholar] [CrossRef]

- Buchanan, B.; Cao, C.X.; Chen, C. Corporate social responsibility, firm value, and influential institutional ownership. J. Corp. Financ. 2018, 52, 73–95. [Google Scholar] [CrossRef]

- Aupperle, K.E.; Carroll, A.B.; Hatfield, J.D. An empirical examination of the relationship between corporate social responsibility and profitability. Acad. Manag. J. 1985, 28, 446–463. [Google Scholar]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef] [Green Version]

- Russo, M.V.; Harrison, N.S. Organizational design and environmental performance: Clues from the electronics industry. Acad. Manag. J. 2005, 48, 582–593. [Google Scholar] [CrossRef]

- Howard-Grenville, J.A.; Hoffman, A.J. The importance of cultural framing to the success of social initiatives in business. Acad. Manag. Pers. 2003, 17, 70–84. [Google Scholar] [CrossRef]

- Surroca, J.; Tribó, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strateg. Manag. J. 2010, 31, 463–490. [Google Scholar] [CrossRef] [Green Version]

- Godfrey, P.C. The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Acad. Manag. Rev. 2005, 30, 777–798. [Google Scholar] [CrossRef]

- Rosen, S.; Simon, J.; Vincent, J.R.; MacLeod, W.; Fox, M.; Thea, D.M. AIDS is your business. Harv. Bus. Rev. 2003, 81, 80–87. [Google Scholar]

- Ferris, G.R.; Treadway, D.C.; Kolodinsky, R.W.; Hochwarter, W.A.; Kacmar, C.J.; Douglas, C.; Frink, D.D. Development and validation of the political skill inventory. J. Manag. 2005, 31, 126–152. [Google Scholar] [CrossRef]

- Bai, C.E.; Lu, J.; Tao, Z. Property rights protection and access to bank loans: Evidence from private enterprises in China. Econ. Trans. 2006, 14, 611–628. [Google Scholar] [CrossRef] [Green Version]

- Berry, L.L.; Shankar, V.; Parish, J.T.; Cadwallader, S.; Dotzel, T. Creating new markets through service innovation. MIT Sloan Manag. Rev. 2006, 47, 56. [Google Scholar]

- Neiheisel, S.R. Corporate Strategy and the Politics of Goodwill; Peter Lang: New York, NY, USA, 1994. [Google Scholar]

- Dickson, M.W.; Den Hartog, D.N.; Mitchelson, J.K. Research on leadership in a cross-cultural context: Making progress, and raising new questions. Q. Leadersh. 2003, 14, 729–768. [Google Scholar] [CrossRef]

- Fornes, G.; López Vázquez, B.; Blanch, J. CSR and S&E engagement in emerging economies. Analysis of a case study based in China. Acad. Manag. Proc. 2018, 11089. [Google Scholar] [CrossRef]

- Tian, Z.; Wang, R.; Yang, W. Consumer responses to corporate social responsibility (CSR) in China. J. Bus. Ethics 2011, 101, 197–212. [Google Scholar] [CrossRef]

- Wang, L.; Juslin, H. The impact of Chinese culture on corporate social responsibility: The harmony approach. J. Bus. Ethics 2009, 88, 433–451. [Google Scholar] [CrossRef]

- Berman, S.L.; Wicks, A.C.; Kotha, S.; Jones, T.M. Does stakeholder orientation matter? The relationship between stakeholder management models and firm financial performance. Acad. Manag. J. 1999, 42, 488–506. [Google Scholar]

- Porter, M.E.; Kramer, M.R. The competitive advantage of corporate philanthropy. Harv. Bus. Rev. 2002, 80, 56–68. [Google Scholar]

- Saiia, D.H.; Carroll, A.B.; Buchholtz, A.K. Philanthropy as strategy: When corporate charity “begins at home”. Bus. Soc. 2003, 42, 169–201. [Google Scholar] [CrossRef]

- Adams, M.; Hardwick, P. An analysis of corporate donations: United Kingdom evidence. J. Manag. Stud. 1998, 35, 641–654. [Google Scholar] [CrossRef]

- Nee, V. Organizational dynamics of market transition: Hybrid forms, property rights, and mixed economy in China. Adm. Sci Q. 1992, 37, 1–27. [Google Scholar] [CrossRef]

- Hull, C.E.; Rothenberg, S. Firm performance: The interactions of corporate social performance with innovation and industry differentiation. Strateg. Manag. J. 2008, 29, 781–789. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. Corporate reputation and philanthropy: An empirical analysis. J. Bus. Ethics 2005, 61, 29–44. [Google Scholar] [CrossRef]

- Wang, Q.; Wong, T.J.; Xia, L. State ownership, the institutional environment, and auditor choice: Evidence from China. J. Account. Econ. 2008, 46, 112–134. [Google Scholar] [CrossRef]

- Kaufmann, D.; Kraay, A. Governance and Growth: Causality Which Way? Evidence for the World, in Brief; World Bank: Washington, DC, USA, February 2003. [Google Scholar]

- Kaplan, S.N.; Zingales, L. Do investment-cash flow sensitivities provide useful measures of financing constraints? Q. J. Econ. 1997, 112, 169–215. [Google Scholar] [CrossRef]

- Chung, K.H.; Pruitt, S.W. A simple approximation of Tobin’s q. Financ. Manag. 1994, 23, 70–74. [Google Scholar] [CrossRef]

- Tien, C.; Chen, C.N.; Chuang, C.M.A. study of CEO power, pay structure, and firm performance. J. Manag. Stud. Organ. 2013, 19, 424–453. [Google Scholar] [CrossRef]

- Song, M.L.; Fisher, R.; Wang, J.L.; Cui, L.B. Environmental performance evaluation with big data: Theories and methods. Ann. Oper. Res. 2018, 270, 459–472. [Google Scholar] [CrossRef]

- Hu, Y.; Chen, S.; Wang, J. Managerial Humanistic Attention and CSR: Do Firm Characteristics Matter? Sustainability 2018, 10, 4029. [Google Scholar] [CrossRef]

- Hambrick, D.C. High profit strategies in mature capital goods industries: A contingency approach. Acad. Manag. J. 1983, 26, 687–707. [Google Scholar]

- Sun, Q.; Tong, W.H.S. China share issue privatization: The extent of its success. J. Financ. Econ. 2003, 70, 183–222. [Google Scholar] [CrossRef]

- Burke, J.; Rhoades, S.A. Profits and “contestability” in highly concentrated banking markets. Rev. Ind. Organ. 1986, 3, 82–98. [Google Scholar] [CrossRef]

- Ahmed, K.; Falk, H. The value relevance of management’s research and development reporting choice: Evidence from Australia. J. Account. Public Policy 2006, 25, 231–264. [Google Scholar] [CrossRef]

- Han, B.H.; Manry, D. The value-relevance of R&D and advertising expenditures: Evidence from Korea. Int. J. Account. 2004, 39, 155–173. [Google Scholar]

- Shah, S.Z.A.; Liang, S.; Akbar, S. International Financial Reporting Standards and the value relevance of R&D expenditures: Pre and post IFRS analysis. Int. Rev. Financ. Anal. 2013, 30, 158–169. [Google Scholar]

- Fama, E.F.; Jensen, M.C. Separation of ownership and control. J. Law Econ. 1983, 26, 301–325. [Google Scholar] [CrossRef]

- Cleary, S. The relationship between firm investment and financial status. J. Financ. 1999, 54, 673–692. [Google Scholar] [CrossRef]

- Seifert, B.; Morris, S.A.; Bartkus, B.R. Having, giving, and getting: Slack resources, corporate philanthropy, and firm financial performance. Bus. Soc. 2004, 43, 135–161. [Google Scholar] [CrossRef]

- McGuire, J.B.; Schneeweis, T.; Branch, B. Perceptions of firm quality: A cause or result of firm performance. J. Manag. Stud. 1990, 16, 167–180. [Google Scholar] [CrossRef]

- Fan, G.; Wang, X.; Zhu, H. NERI Index of Marketization of China’s Provinces; National Economic Research Institute: Beijing, China, 2003. [Google Scholar]

- Aiken, L.S.; West, S.G.; Reno, R.R. Multiple Regression: Testing and Interpreting Interactions; Sage: Newcastle upon Tyne, UK, 1991. [Google Scholar]

- Dutton, J.E.; Dukerich, J.M.; Harquail, C.V. Organizational images and member identifications. Adm. Sci. Q. 1994, 39, 239–263. [Google Scholar] [CrossRef]

- Kramer, R.M. Intergroup relations and organizational dilemmas: The role of categorization processes. In Research in Organizational Behavior; Cummings, L.L., Staw, B.M., Eds.; JAI: Greenwich, CT, USA, 1991; Volume 13, pp. 191–228. [Google Scholar]

- Chung, C.; Jung, S.; Young, J. Do CSR Activities Increase Firm Value? Evidence from the Korean Market. Sustainability 2018, 10, 3164. [Google Scholar] [CrossRef]

- Nguyen, T.N.; Phan, T.T.H.; Cao, T.K.; Nguyen, H.V. Green purchase behavior: Mitigating barriers in developing countries. Strateg. Dir. 2017, 33, 4–6. [Google Scholar] [CrossRef]

- Nguyen, T.N.; Lobo, A.; Greenland, S. The influence of cultural values on green purchase behaviour. Mark. Int. Plan. 2017, 35, 377–396. [Google Scholar] [CrossRef]

Figure 1.

Moderating effect of advertising intensity.

Figure 2.

Moderating effect of SOE.

{kind=link}

{kind=link}

Table 1.

A list of empirical studies on the relationship between corporate social responsibility (CSR) and firm value.

Table 1.

A list of empirical studies on the relationship between corporate social responsibility (CSR) and firm value.

| Author(s) (Year) | Measures | CSR → Firm Value |

|---|---|---|

| Brammer et al. (2006) | CSR: EIRIS scores Firm value: stock returns | Scores on a composite social performance indicator are negatively related to stock returns |

| Crisóstomo et al. (2011) | CSR: index adopted in this study is based on IBase’s information Firm value: stock returns | CSR is value-destroying in Brazil as indicated by a significant negative correlation between CSR and firm value |

| Servaes & Tamayo (2013) | CSR: KLD scores Firm value: Tobin’s Q | CSR activities can add value to the firm but only under certain conditions. |

| Deng et al. (2013) | CSR: KLD scores Firm value: Tobin’s Q | High CSR acquirers realize higher merger announcement returns, higher announcement returns on the value-weighted portfolio of the acquirer and the target, and larger increases in post-merger long-term operating performance. Mergers by high CSR acquirers take less time to complete and are less likely to fail than mergers by low CSR acquirers. |

| Harjoto & Jo (2015) | CSR: KLD scores Firm value: Tobin’s Q | Overall CSR intensities reduce analyst dispersion of earnings forecast, volatility of stock return, and cost of capital (COC), and increase firm value. Its impact is reduced for firms with better accounting and disclosure quality |

| Krüger (2015) | CSR: KLD scores Firm value: Daily CARs. | Investors do value “offsetting CSR”. CSR news with stronger legal and economic information content generates a more pronounced investor reaction. |

| Mishra & Modi (2016) | CSR: KLD scores Firm value: Stock response modeling to assess unanticipated stock return | An analysis indicates that the effects of overall CSR efforts on stock returns and idiosyncratic risk are not significant on their own but only become so in the presence of marketing capability. |

| El et al. (2017) | CSR: environmental and social performance scores in ASSET4T Firm value: Tobin’s Q | The value of CSR initiatives is greater in countries with weaker market institutions because firms can adopt CSR activities to fill institutional voids. |

| Harjoto & Laksmana (2018) | CSR: KLD scores Firm value: Tobin’s Q | Stronger CSR performance is associated with smaller deviations from optimal risk-taking levels. CSR performance is positively associated with firm value |

| Sheikh, (2018) | CSR: The difference between total CSR strengths and total CSR concerns in five dimensions (community, diversity, employees, product, and environment). Firm value: adjusted Tobin’s Q | CSR is positively associated with market value. This relation is influenced by product market competition and product fluidity. Furthermore, results show that the effect of CSR is driven by CSR strengths as CSR concerns have no effect on firm value. |

Note: EIRIS is the Ethical Investment Research Service which specializes in the measurement of corporate social performance against an objective set of criteria, principally for use by institutional investors. KLD score is obtained from the Kinder, Lydenberg, and Domini (KLD) database, which is a social choice investment advisory firm that relies on independent rating experts to assess how well companies address the needs of their stakeholders based on multiple data sources including annual questionnaires sent to companies’ investor relations offices, firms’ financial statements, annual and quarterly reports, general press releases, government surveys, and academic publications. CAR is cumulative abnormal return.

Table 2.

Measurement of main variables.

| Variable | Symbol | Measurement |

|---|---|---|

| Dependent Variable | ||

| Firm value | Tobin Q | The value of Tobin Q, lagged by one year (t + 1), the numerator is the market value of stock, the denominator is the total asset amount at the end of fiscal year |

| Independent variable | ||

| Corporate Social Responsibility | CSR | The comprehensive score of Hexun CSR index, range from 0 to 100 |

| Moderator | ||

| State Ownership | SOE | SOE = 1 if the firm is a state-owned enterprise (SOE); SOE = 0 otherwise |

| Advertising Intensity | AD | The ratio of Selling, General, and Administrative (SG&A) to sales |

| Control variable | ||

| Market Development | MI | GDP of a province, divided by the provincial government’s budget |

| Firm Size | Size | The total asset at the end of fiscal year, taking the natural logarithm |

| Net Profit | Profit | The net profit at the end of fiscal year, taking the natural logarithm |

| Firm Age | Age | |

| Capital Structure | Outcap | The firm capital expenditure at the end of fiscal year, taking the natural logarithm |

| Ownership Concentration | SHR | The sum of the ratio of shares held by the top ten shareholders |

| Abundance of Cash Flow | ACF | The ratio of net operating cash flow to total operating revenue |

| Slack Resource | Slack | The ratio of cash flow to total assets of the firm |

| Subindustry | ID | The subindustry of a certain manufacturing firm |

Table 3.

Means, standard deviations, and correlations.

| Mean | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Tobin Q | 2.953 | 4.285 | 1 | |||||||||||

| 2. CSR | 25.763 | 18.840 | 0.095 ** | 1 | ||||||||||

| 3. SOE | 0.134 | 0.341 | −0.055 ** | 0.042 ** | 1 | |||||||||

| 4. AD | 0.057 | 0.228 | −0.004 | −0.024 * | 0.006 | 1 | ||||||||

| 5. MI | 9.146 | 2.084 | 0.002 | 0.039 ** | −0.158 ** | 0.025 * | 1 | |||||||

| 6. Size | 21.798 | 1.194 | −0.323 ** | 0.334 ** | 0.153 ** | −0.013 | −0.082 ** | 1 | ||||||

| 7. Profit | 16.625 | 5.878 | −0.100 ** | 0.438 ** | −0.048 ** | −0.005 | 0.106 ** | 0.189 ** | 1 | |||||

| 8. Age | 9.842 | 6.085 | 0.037 ** | 0.008 | 0.246 ** | 0.022 * | −0.244 ** | 0.302 ** | −0.157 ** | 1 | ||||

| 9. Outcap | 18.533 | 1.842 | −0.368 ** | 0.302 ** | 0.054 ** | −0.019 | 0.023 * | 0.708 ** | 0.247 ** | 0.004 | 1 | |||

| 10. SHR | 57.534 | 15.941 | −0.050 ** | 0.152 ** | −0.036 ** | −0.013 | 0.174 ** | 0.040 ** | 0.199 ** | −0.547 ** | 0.169 ** | 1 | ||

| 11. ACF | −0.115 | 20.586 | 0.001 | 0.013 | 0.003 | −0.001 | 0.014 | 0.053 ** | 0.035 ** | −0.010 | 0.036 ** | 0.011 | 1 | |

| 12. Slack | 7.476 | 241.123 | −0.004 | −0.004 | −0.007 | −0.004 | −0.009 | −0.022 * | 0.006 | 0.005 | −0.008 | 0.003 | 0.000 | 1 |

Note: * p < 0.05, ** p < 0.01.

Table 4.

Empirical results of multiple linear regression

| Firm Value (Tobin Q, Year = t + 1) | |||||

|---|---|---|---|---|---|

| Variable | (1) | (2) | (3) | (4) | (5) |

| MI | 0.0278 * | 0.0254 * | 0.0253 * | 0.0237 | 0.0237 |

| (2.33) | (2.07) | (2.06) | (1.93) | (1.92) | |

| Size | −0.9950 ** | −1.0310 *** | −1.0320 *** | −1.0280 *** | −1.0290 *** |

| (−3.16) | (−3.40) | (−3.41) | (−3.39) | (−3.40) | |

| Profit | −0.0047 | −0.0159 | −0.0159 | −0.0161 | −0.0160 |

| (−0.48) | (−1.64) | (−1.63) | (−1.68) | (−1.67) | |

| Age | 0.1090 *** | 0.1090 *** | 0.1090 *** | 0.1080 *** | 0.1080 *** |

| (4.43) | (4.29) | (4.30) | (4.28) | (4.30) | |

| Outcap | −0.4240 *** | −0.4280 *** | −0.4280 *** | −0.4280 *** | −0.4280 *** |

| (−4.57) | (−4.63) | (−4.63) | (−4.63) | (−4.63) | |

| SHR | 0.0220 *** | 0.0211 *** | 0.0212 *** | 0.0210 *** | 0.0210 *** |

| (7.05) | (6.50) | (6.52) | (6.49) | (6.50) | |

| ACF | 0.0055 *** | 0.0056 *** | 0.0056 *** | 0.0056 *** | 0.0056 *** |

| (5.94) | (6.04) | (6.05) | (6.07) | (6.07) | |

| Slack | −0.0002 * | −0.0002 * | −0.0002 * | −0.0002 * | −0.0002 * |

| (−2.35) | (−2.30) | (−2.31) | (−2.32) | (−2.32) | |

| SOE | −0.7150 *** | −0.7320 *** | −0.7470 *** | −0.7470 *** | −0.7320 *** |

| (−3.56) | (−3.58) | (−3.82) | (−3.81) | (−3.57) | |

| AD | −0.2160 * | −0.2010 | −0.4190 * | −0.2000 | −0.4090 * |

| (−2.07) | (−1.94) | (−2.43) | (−1.95) | (−2.42) | |

| CSR | 0.0097 *** | 0.0096 *** | 0.0079 *** | 0.0078 *** | |

| (5.79) | (5.72) | (3.99) | (3.92) | ||

| CSR*SOE | 0.0098 * | 0.0097 * | |||

| (2.41) | (2.40) | ||||

| CSR*AD | −0.0150 ** | ||||

| (0.01) | |||||

| Constants | 29.7100 *** | 30.5700 *** | 30.6000 *** | 30.5900 *** | 30.6200 *** |

| (4.52) | (4.83) | (4.83) | (4.83) | (4.83) | |

| Industry | yes | yes | yes | yes | yes |

| N | 7899 | 7899 | 7899 | 7899 | 7899 |

| R2 | 0.1766 | 0.1779 | 0.1780 | 0.1782 | 0.1782 |

| △R2 | 0.1857 | 0.1899 | 0.1900 | 0.1901 | 0.1902 |

| Χ2 | 1685.86 *** | 1700.71 *** | 1701.13 *** | 1703.65 *** | 1704.01 *** |

Note: * p < 0.05, ** p < 0.01, *** p < 0.001; Standard errors in parentheses.

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Hu, Y.; Chen, S.; Shao, Y.; Gao, S. CSR and Firm Value: Evidence from China. Sustainability 2018, 10, 4597. https://doi.org/10.3390/su10124597

AMA Style

Hu Y, Chen S, Shao Y, Gao S. CSR and Firm Value: Evidence from China. Sustainability. 2018; 10(12):4597. https://doi.org/10.3390/su10124597

Chicago/Turabian StyleHu, Yuanyuan, Shouming Chen, Yuexin Shao, and Su Gao. 2018. "CSR and Firm Value: Evidence from China" Sustainability 10, no. 12: 4597. https://doi.org/10.3390/su10124597

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.