Factors Affecting Local Governments’ Public–Private Partnership Adoption in Urban China

1

Hang Lung Center for Real Estate and Department of Construction Management, Tsinghua University, Beijing 100084, China

2

School of Public Economics and Administration, Shanghai University of Finance and Economics, Shanghai 200433, China

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(23), 6831; https://doi.org/10.3390/su11236831

Submission received: 1 October 2019

/

Revised: 7 November 2019

/

Accepted: 29 November 2019

/

Published: 2 December 2019

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:Local governments around mainland China initiated over 14,000 public–private partnership (PPP) projects with a total investment of 18 billion RMB in recent years, but nearly half have been withdrawn since the end of 2017, which raised wide concerns about whether PPP can contribute to the sustainable infrastructure development in urban China. In this study, we empirically investigated major factors affecting local governments’ PPP adoption, especially factors that led local governments to initiate inappropriate PPP projects. Based on a unique panel dataset of 286 Chinese cities between 2014 and 2017, the empirical findings suggested that local governments’ financial pressure was the most important factor and cities with higher off-budgetary debts or lower budgetary deficits tended to initiate more PPP projects. PPP projects initiated under off-budgetary burdens were more likely to be inappropriate and subsequently withdrawn. Based on the empirical results, we provide policy suggestions to promote sustainable PPP developments in China.

1. Introduction

A public–private partnership (PPP) refers to an arrangement between public and private sectors to share both risks and benefits in planning, financing, constructing, and operating public projects [1]. PPP is widely adopted around the world as a long-term cooperation between public and private sectors in infrastructure investment and public service delivery [2]. Local governments in mainland China, in particular, have been extremely enthusiastic in initiating PPP projects since 2014 under the promotion of the central government [3,4]. According to the statistics published by the Ministry of Finance of China, local governments around China initiated over 14,000 PPP projects between 2014 and 2017, which substantially outpaced not only the total number of PPP projects initiated in the rest of the world during the same period, but also the aggregated number of PPP projects in China in the previous three decades.

This unprecedented increase within a short period naturally led to the question as to whether PPP had been over-adopted or even abused and whether it was helpful for the sustainable infrastructure development in urban China [5]. Although PPP, in general, is perceived to be more efficient than most traditional infrastructure procurement processes [6], literature points out that not all infrastructure projects are suitable for PPP [7,8]. In particular, due to high pre-contract negotiation costs and high financing costs for the private sector, many studies suggested that private participation in infrastructure may also increase the cost of delivery of public services and PPP is only suitable for projects with a clear output, large market demand, and certain profitability [9,10,11]. Therefore, the local governments should fully pre-evaluate the appropriateness before initiating a PPP project. In the Chinese context, many projects initiated by local governments were proven unsuitable for PPP. Notably, after the Chinese central government issued a stricter regulation policy at the end of 2017, the local governments withdrew over 40% of the 14,000 PPP projects, which not only substantially wasted social resources, but also undermined local governments’ credibility as a reliable partner.

In this study, we constructed a unique panel dataset on the volume and types of PPP projects initiated by all 286 cities in China between 2014 and 2017. Based on this dataset, we empirically investigated the effect of major factors on local governments’ PPP adoption. We used the withdrawn project data to investigate which factors led to the initiation of inappropriate PPP projects by local governments. Most of the literature focuses on how microlevel factors, such as contract design, affect the performance of PPP projects [12,13], while only a small number of empirical studies investigate the impact of macrolevel factors on PPP development, especially whether local governments choose to adopt PPP in local infrastructure development. To the best of our knowledge, we provide one of the first empirical insights into local governments’ PPP adoption. Considering the key role of local governments in PPP development, the results and associated policy suggestions can contribute to the sustainable development of PPP in both China and other emerging economies.

2. PPP Development in China

The development of PPP in China can be traced back to more than 30 years. With the change in China’s macro-economic environment, PPP has undergone several phases. Cheng et al. [3] divided the PPP development process into four phases: exploration (1984–2002), stable expansion (2003–2008), development with fluctuations (2009–2013), and new boom (2014–present). Since 2014, China’s central government has issued a large number of regulations to promote the application of PPP and to standardize the implementation of PPP projects. According to these regulations, PPP is applicable to infrastructure and public service projects with a large investment scale, long-term stable demand, flexible price adjustment mechanism, and high degree of marketization.

Furthermore, any project must pass the value-for-money (VFM) evaluation and fiscal affordability assessment before initiated as a PPP project by the local government. VFM analyzes whether the cost of infrastructure and public service projects provided by the PPP mode is lower than that provided by the traditional mode, which is widely used as a principle for the adoption of PPP projects [14,15]. Fiscal affordability assessment is a method used to judge whether local governments have sufficient financial budgetary resources to implement PPP projects. According to the relevant regulations of China’s central government on fiscal affordability assessment, local governments must complete life-cycle budgetary expenditure responsibility calculations for each PPP project initiated and summarize budgetary expenditure of all PPP projects implemented and planned to be implemented in that year. The central government regulates that the budgetary expenditure of all PPP projects cannot exceed 10% of the general public budget expenditure. Fiscal affordability assessment can effectively prevent and control financial risks and help achieve the sustainable development of PPP projects.

Currently in China, the whole life of a typical PPP project mainly includes four stages, namely, initiation, bidding, implementation, and transfer. A PPP project can enter into the implementation stage only when the private partner is selected through the bidding process. During the implementation process, which might last for up to 30 years, the funding structure is crucial to the PPP project’s performance. Since local governments are responsible for infrastructure delivery in China, China’s central government has no obligation to directly fund PPP projects. Therefore, the main funding sources of PPP projects are from local governments and the private partners, while the investment share typically depends on the payment mechanism. According to the data by the Ministry of Finance (MOF) of China, 35.4% of the PPP projects in China were mainly funded by local governments, 32.1% were mainly funded by the private sectors, with the rest 32.5% jointly funded by both the local governments and private partners under the so-called “viability gap funding” mechanism.

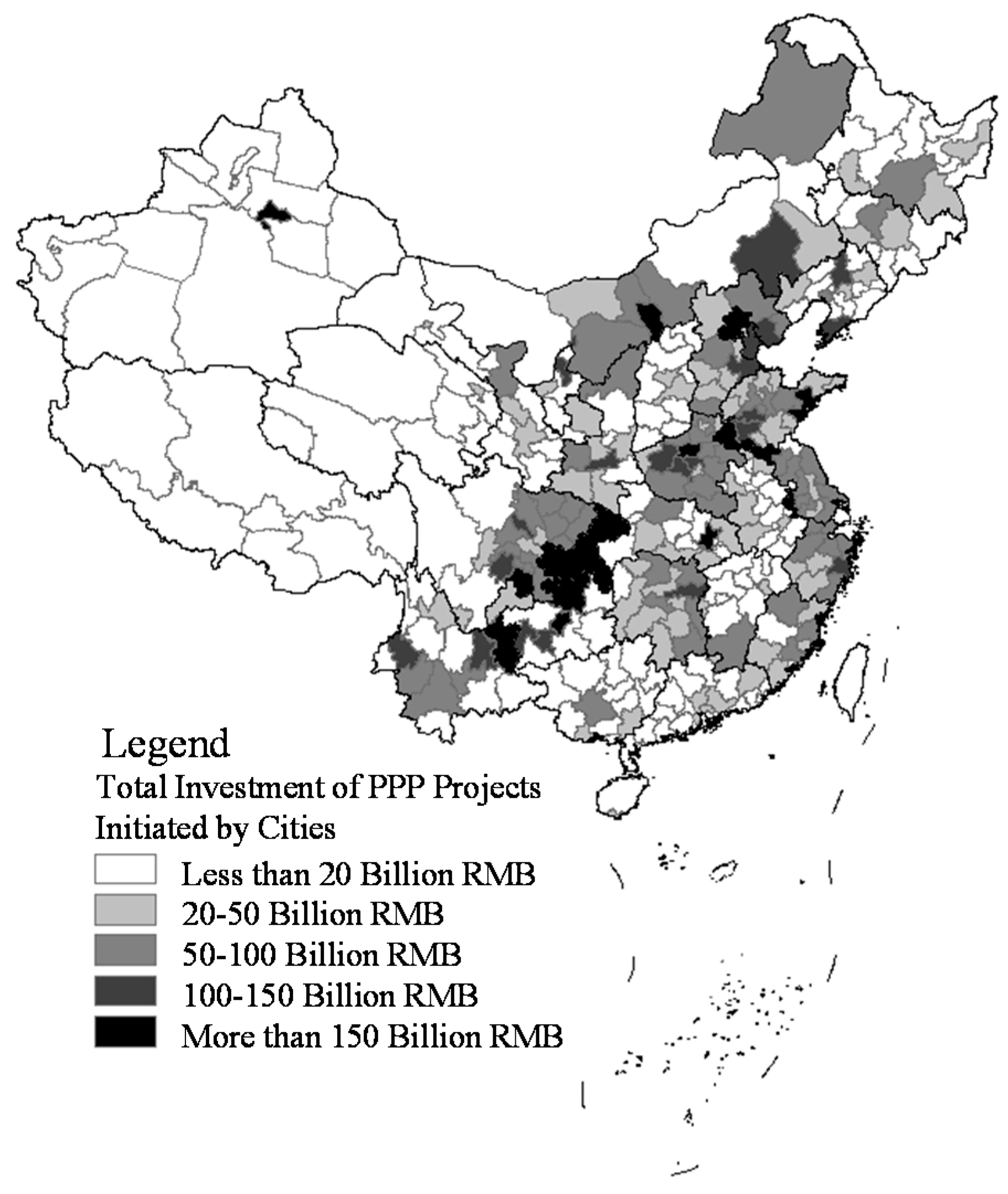

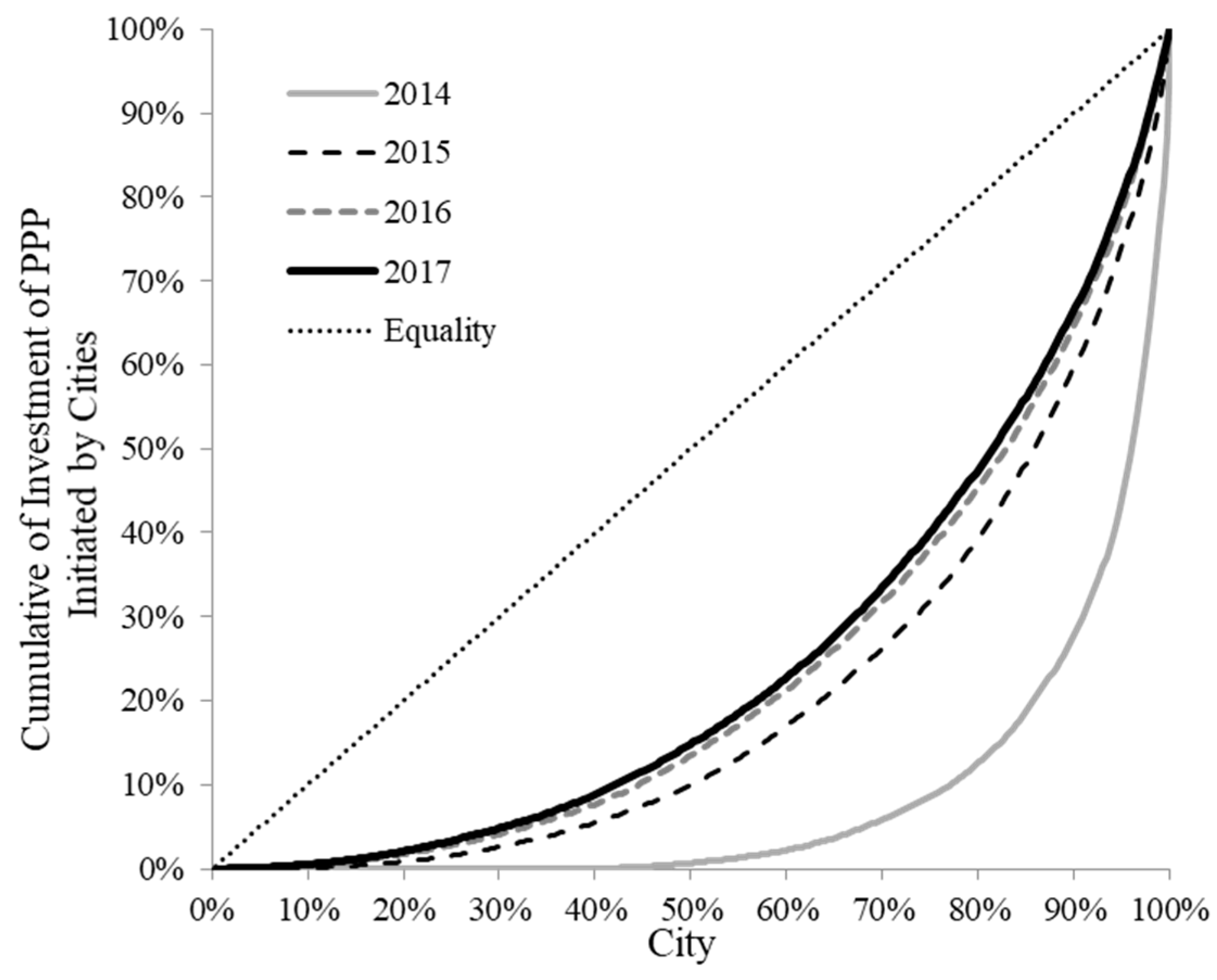

To standardize the operation process of PPP and improve the transparency of the whole life of PPP project, MOF developed the National PPP Integrated Information Platform and stipulated that PPP projects not included in this information platform (i.e., database) cannot receive financial budgetary support (MOF (2015) No. 166), which is the main source of most PPP projects’ income. The above stipulation ensures all PPP projects initiated by local governments are included in the database. The total investment in PPP projects in the database reflects the willingness of local governments to adopt PPP. From 2014 to 2017, 14,016 PPP projects with a total investment of nearly 18 billion RMB were initiated. In terms of geographic distribution, the PPP projects have been substantially dispersed geographically, but the spatial imbalance in PPP projects is still severe. As shown in Figure 1, the investments in PPP projects are imbalanced in space and show no obvious correlation between local governments’ willingness to adopt PPP and the local economic development level. Referring to the income inequality indicator, we plotted the Lorenz curves of cumulative investment in PPP projects by city to reveal the imbalance in PPP adoption (Figure 2). The straight line in the figure shows that the number of PPP projects initiated by each city is the same, and the closer the diagonal line, the stronger the balance. The imbalance has been alleviated since 2014, but remained at a high level until 2017. As of the end of 2017, 20% of the cities invested almost 50% of the total in PPP projects.

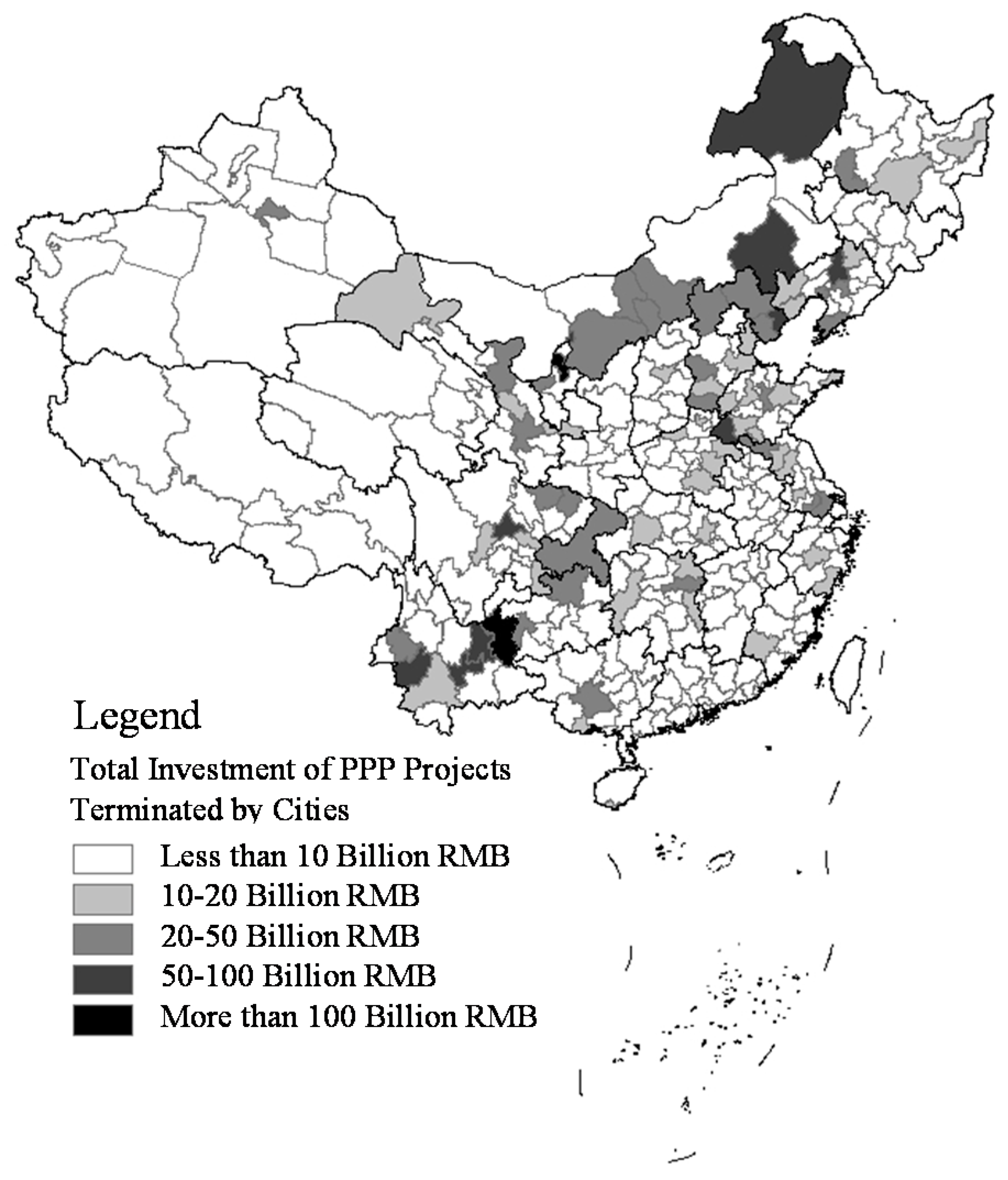

With the rapid development of PPP, many local governments rely excessively on PPP for infrastructure development, resulting in the abuse of PPP. PPP is not suitable for every kind of infrastructure construction project, such as those with a small investment, vague output, or insufficient market demand [9]; however, many projects unsuitable for PPP were initiated by local governments. The abuse of PPP application may increase the financial risk of local governments, and thus undermine the efficiency of infrastructure investment. Therefore, the Ministry of Finance issued the Notice on Regulating the Operation of the Management Database of the PPP Integrated Information Platform (MOF (2017) No. 92) at the end of 2017, which is considered the strictest regulation on PPP development. In accordance with the requirements of this regulation, local governments should review the PPP projects and withdraw inappropriate projects, including: (i) projects without strict economic feasibility evaluation according to the regulations (MOF (2014) No. 113), (ii) projects that neither belong to public service projects nor include operation process, and (iii) other situations that are unsuitable for the PPP mode. In the same regulation, the Ministry of Finance also explicitly urged the local governments to carefully review each previously initiated PPP project and withdraw all of the inappropriate PPP projects. We matched all the PPP projects included in the database at the end of 2017 with those at the end of August 2018 and found that 5943 projects had been withdrawn, accounting for 43.5% of all projects initiated by local governments at the end of 2017. Figure 3 depicts the spatial distribution of the investment in withdrawn PPP projects. The scale of withdrawn PPP projects reflects the scale of the inappropriate PPP projects initiated by local governments. This provided a valuable opportunity to directly investigate why local governments initiate inappropriate PPP projects.

3. Theoretical Analysis and Hypothesis

3.1. Theoretical Analysis

Some studies have examined the key factors that influence PPP development from the macro-economic perspective [6]. Yehoue et al. [16] found that countries with heavy debt burdens, a large market size, or a high institutional quality tend to encourage PPP development. Albalate et al. [17] found that private sector is more willing to participate in PPP in the regions with higher possibility of recovering investment costs. Girth [18] concluded that cities with a higher level of political–administrative autonomy and greater economic stability are more likely to adopt PPP. Wang and Zhao [19] identified traffic demand, fiscal pressure, and PPP legislation as the main drivers of PPP adoption in highway tolling projects. Tan and Zhao [5] reviewed the development of PPP in China and indicated that PPP plays an important role in delivering infrastructure and reducing financial pressure.

Among the studies investigating different factors influencing PPP development, only Yang et al. [20] developed a generic framework to explain the adoption of PPP. The framework is composed of three aspects: the market, the government, and the operating environment. We further developed the framework of Yang et al. [20] and propose an empirical analysis framework to explore the determinants of local governments’ PPP adoption. The market factor indicates the profitability in undertaking PPP projects. The gap between infrastructure demand and supply affects the amount of PPP project usage, and further affects the return level of the private sector partner in PPP projects. The government factor refers to the credibility or capacity of the government. For PPP projects, the credibility or capacity of the government mainly refers to the government’s ability to pay and the corresponding default risk, which is mainly affected by the government’s financial pressure. The operating environment is mainly the institutional environment [21]. Thus, we propose that the factors influencing government PPP adoption can be divided into three categories: infrastructure shortage, financial pressure, and institutional environment.

3.2. Hypotheses

Firstly, since 1978, China’s urbanization rate has been rising rapidly by nearly one percentage point per year, which brings a huge infrastructure demand [22]. Infrastructure investment in China has even become a major driver of economic growth [23]. Governments, however, struggle to deliver the infrastructure by themselves to meet infrastructure demand [8]. The participation of private sectors can improve the efficiency and effectiveness of public service delivery and achieve the goal of sustainable development [24,25]. Thus, we have:

Hypothesis 1 (H1).

Local governments with larger infrastructure shortages are more likely to initiate more PPP projects.

Secondly, financial pressure is an important factor influencing government innovation in infrastructure delivery [26]. Since PPP is an innovative tool for infrastructure investment and financing, the influence of financial pressure is reflected mainly in two aspects: (i) PPP can smooth financial expenditure and provide an off-balance-sheet financing option to the governments [27], which would reduce local governments’ financial pressure; and (ii) Glasser [28] found that countries with lesser financial resources are more inclined to encourage private sectors to participate in public investment. In response to the 2008 global financial crisis, China’s central government started to implement the 4 trillion RMB stimulus plan. As a result, local governments’ debt rose steeply, accounting for 22% of gross domestic product (GDP) in 2013, which had only been 5.8% in 2006 [29]. To control the risk of local governments’ debt, China’s central government proposed that the private sector should be allowed to participate in infrastructure investment and public services delivery at the end of 2013. Thus, we have:

Hypothesis 2 (H2).

Local governments with higher financial pressure tend to have stronger incentives to adopt PPP mode.

Thirdly, some researchers implied that the institutional environment is one of the major determinants of PPP development [30,31,32]. A PPP, as a long-term infrastructure contract involving many actors, faces considerable uncertainty in the implementation process [33]. Brewer and Hayllar [34] implied that good partnerships between the public and private are easy to build and sustain in a sound institutional environment. Sanghi et al. [35] concluded that regions with a higher level of management by the governments are more likely to promote PPP development. China’s legal and institutional environment is still relatively unstable. For example, as the leader of the local government, local chiefs have been rotated at high frequency, which might increase political risks [36]. Thus, we have:

Hypothesis 3 (H3).

Local governments with better institutional environment tend to initiate more PPP projects.

4. Data and Method

4.1. Data and Variables

We manually collected information about all the PPP projects included in the National PPP Integrated Information Platform (i.e., database) developed by the Ministry of Finance. As the most important data in the empirical analysis, the data structure of the dependent variables was a panel dataset, which was constructed on the investment of PPP projects initiated by 286 cities in China between 2014 and 2017. The total sample size of this panel dataset was 1144, which equaled 286 cities multiplied by 4 years (from 2014 to 2017).

The key dependent variable, the scale of local governments’ PPP adoption (INVEST_PPP), was measured by the total investment volume in all PPP projects initiated by the local governments in the city-year, normalized by the permanent urban population at the end of the year. In addition to the total volume of all PPP projects, we also grouped the projects from two perspectives. Firstly, from the perspective of economic and social impacts, PPP projects were divided into two major categories: economic infrastructure (INVEST_ECO) and social infrastructure (INVEST_SOC) [37,38,39]. Economic infrastructure, including energy, technology, and transportation, aims to promote short-term economic growth; social infrastructure, including education, medical care, environmental hygiene, and social security, aims to improve the overall welfare of the society. Secondly, according to whether the projects were withdrawn or not after the Ministry of Finance issued the strict regulation in 2017, all the PPP projects in the sample were divided into two categories: PPP projects withdrawn by its initiators (WITHDRAW) and PPP projects not withdrawn by its initiators by the end of 2018 (NWITHDRAW). The withdrawn projects were then further divided into economic infrastructure (WITHDRAW_ECO) and social infrastructure (WITHDRAW_SOC).

As mentioned in the theoretical analysis, we mainly focused on three categories of variables as explanatories. Firstly, infrastructure shortage refers to the gap between the aggregate demand and the stock supply of infrastructure. The aggregate demand for infrastructure was measured by per capita GDP (GDPPC) and the growth rate of annual per capita GDP (D_GDPPC) [16]. Per capita GDP reflects the level of economic development. A higher level of economic development means a higher infrastructure demand. The growth rate of annual per capita GDP reflects the potential for economic growth. The greater the potential for economic growth, the greater the growth of the demand for infrastructure. Although no direct indicator exists for infrastructure stock, cities with higher infrastructure stock level have higher maintenance costs. Therefore, the infrastructure supply was measured by the ratio of the fiscal expenditure for maintenance and management of public service to GDP (INFRA_STOCK). We expected that cities with a higher demand for infrastructure or lower infrastructure stock would initiate more PPP projects.

The financial pressure can be decomposed into three indicators according to the different sources of financial revenues. In China, the three main sources of local government revenue for infrastructure investment are budgetary fiscal revenue, land-grant premiums, and funds borrowed through local governments’ financing vehicles (LGFVs) [40,41]. Due to the different regulations from the central government for each revenue source, different types of financial pressure have different impacts on PPP adoption. Firstly, budgetary fiscal revenue is strictly supervised by the central government [42]. As mentioned in Section 2, when initiating PPP projects, local governments should abide by the fiscal affordability assessment requirement. In the empirical analysis, budgetary fiscal deficit (BUDGET_DEFICIT) was adopted to reflect the influence of budgetary fiscal revenue. Budgetary fiscal deficit (BUDGET_DEFICIT) is the gap between fiscal revenue and fiscal expenditure divided by fiscal expenditure. We expected that cities with a higher budgetary fiscal deficit would initiate fewer PPP projects. Secondly, land-grant premiums have become one of the major local governments’ revenue sources to finance infrastructure investment [43,44]. We adopted the ratio between land-grant premiums and fiscal revenue (LAND_REVENUE) as the proxy, with the assumption that local governments would rely less on PPP if they have a higher revenue from the land market. Finally, LGFVs are established for the explicit purpose of borrowing and spending on behalf of local governments [45], and funds borrowed by LGFVs constitute the most important part of local governments’ debt [41]. Due to concern about increasing local government debt, the central government revised the budget law in 2015, further strengthening the administration of local government debts, making cities with higher debts face greater financial constraints and initiating more PPP projects to relieve the financial pressure on local governments. We estimated the total outstanding volume of LGFVs debt at the beginning of the year, normalized by the GDP at the same time point (DEBT). More specifically, we obtained the list of all LGFVs authorized to issue bonds from the China Banking Regulatory Commission and collected the balance sheet data for these entities from the Wind database. Finally, we added the total outstanding debt of all LGFVs for each city-year. Cities with a higher debt stock have a lower financing capacity, which reduces the government’s ability to invest in infrastructure. We expected that cities with a higher debt stock would be more dependent on PPP.

Institutional environment is a comprehensive concept that reflects the basic rules of politics, society, and law. PPP development is mainly affected by the degree of marketization, the level of private sector development, and the management capacity of government. In the empirical analysis, the effects of the institutional environment were captured by three indicators from different aspects. The first variable was the marketization index (MARKETIZATION), which is widely used to measure the quality of an institution [46,47]. It is measured by the provincial index compiled by the National Economic Research Institute, and comprehensively captures the regional market development conditions [48]. The latest data of the marketization index are from 2014, and only these cross-sectional data can be used to reflect the differences among provinces. The second variable was the ratio of private sector employees to the total working population (PRIVATERATIO). Cities with a more developed private sector will initiate more PPP projects. The third variable was the government integrity index (INTEGRITY), compiled by the Renmin University of China, to measure the management capacity of the government.

In addition to the above factors, we included the logarithmic form of the permanent urban population at end of the year (POP_UR) as the control variable. We also controlled for provincial and year fixed effects to eliminate the potential omitted variable problem. Table 1 lists the definitions and descriptive statistics of all the variables.

4.2. Empirical Method

We employed a regression model to investigate the effects of the aforementioned infrastructure shortage (IS), financial pressure (FP), and institutional environment (IE) on the investment in PPP projects initiated by local governments (INVEST_PPPit). Notably, the investment in PPP projects initiated by the city government was fixed to zero and the observation of INVEST_PPPit was zero, even if the value should be negative according to the macro-economic environment. As 17% of the 1144 observations of INVEST_PPPit were zero, employing the ordinary least squares (OLS) model would lead inconsistent regression coefficient. The Tobit model was adopted to address this problem in the empirical analysis [49], the basic regression model is (Equations (1)–(3)):

where INVEST_PPPit* is the latent dependent variable; INVEST_PPPit is the per GDP total investment in PPP projects initiated by local governments by city-year, which can be observed directly; the explanatory variables include vectors of IS, FP, and IE, as described in detail in the previous section; α is a constant; β1, β2, and β3 are vectors of coefficients; and εit is the error term.

INVEST_PPPit* = α + β1ISit + β2FPit + β3IEit + εit,

INVEST_PPPit = INVEST_PPPit* if INVEST_PPPit* > 0,

INVEST_PPPit = 0 if INVEST_PPPit* ≤ 0

5. Empirical Results

5.1. Impact of Factors on PPP Projects Initiated by Local Governments

The purpose of this part of the study was to examine the impact of factors on PPP projects initiated by local governments. The empirical results are reported in column (1) of Table 2.

Among the variables of infrastructure shortage, the effects of per capita GDP (GDPPC), the growth rate of per capita GDP (D_GDPPC), and the stock of infrastructure (INFRA_STOCK) were not significant, indicating that infrastructure shortage was not the main factor considered, when local governments initiated PPP projects. A lack in demand-oriented project planning will undermine the efficiency of PPP development and the original intention of the central government to support infrastructure investment.

From the perspective of financial pressure, the most important finding was that budgetary deficits and off-budgetary debts differently influenced the adoption of PPP. The coefficient of BUDGET_DEFICIT was significantly negative at the 1% level, suggesting that local governments complied with the requirement of fiscal affordability assessment and initiated PPP projects according to the budgetary deficit. As the debt of LGFVs (DEBT) was not within the local governments’ budget, the empirical results showed that the higher the level of debt, the greater the total investment volume in PPP projects initiated to reduce the financial pressure faced by the local governments. Most LGFVs used land revenues to support borrowing from either banks or other institutional investors, and this may lead to the insignificance of land revenue (LAND_REVENUE).

In terms of institutional environment, the development of private sectors (PRIVATERATIO) was significant, but the marketization index (MARKETIZATION) and the government integrity index (INTEGRITY) were not significant. From the perspective of specific impact, MARKETIZATION and INTEGRITY mainly affected the efficiency of PPP during implementation, whereas PRIVATERATIO may affect the probability of PPP projects being contracted with a private sector. The results showed that the adoption of PPP by local governments was influenced mainly by a short-term interest, but not infrastructure investment efficiency. Due to the high pre-contract PPP negotiation costs, local governments would initiate more PPP projects only when the probability of PPP projects contracted with private sector is higher.

According to the control variables, the total urban population was negatively significant due to the scale effect of infrastructure. Infrastructure is a non-exclusive product; thus, people can share services in a specific area. Therefore, central government should promote cooperation between regions to stimulate public service delivery, and a large-scale infrastructure should be built by the higher level government.

To compare the effects of different determinants, we computed the standardized coefficients of the significant variables. The standardized coefficient is equal to the marginal effect of each independent variable multiplied by the standard deviation of each independent variable and then divided by the dependent variable’s standard deviation. The result suggested that each additional standard deviation of BUDGET_DEFICIT, DEBT, or PRIVATERATIO would cause −0.130, 0.068, and 0.047 standard deviations of the dependent variable, respectively. Financial pressure was the most important determinant of local governments’ PPP adoption in China.

In columns (2) and (3) of Table 2, we examined and compared the determinants of the development of the economic infrastructure (INVEST_ECO) and the social infrastructure (INVEST_SOC), and concluded that the main difference was the impact of financial pressure. First, the impact of budgetary deficit (BUDGET_DEFICIT) on the economic infrastructure was larger than its impact on social infrastructure mainly because the investment in economic infrastructure was much larger than in social infrastructure. Second, cities with a larger urban investment bond issued by LGFVs (DEBT) initiated more PPP economic infrastructure projects, whereas the impacts on social infrastructure were not significant. These empirical results indicated that local governments are more willing to initiate PPP economic infrastructure projects when the off-budgetary debts are higher. The results suggested that the government’s purpose for adopting PPP is to enhance economic growth in the short term, which is consistent with the purpose of traditional infrastructure investment.

5.2. Factors Impacting the Withdrawal of PPP Projects

This part focuses on the question of what factors influenced the withdrawal of PPP projects initiated by local governments. The regression results are reported in Table 3.

In columns (1) and (2) of Table 3, we checked the factors influencing the amount of withdrawn (WITHDRAW) and not-withdrawn (NWITHDRAW) PPP projects, respectively. We drew conclusions from the empirical analysis as follows: among the variables of infrastructure shortage, the demand for infrastructure (D_GDPPC and GDPPC) and the infrastructure stock (INFRA_STOCK) were not significant in the two equations.

From the perspective of financial pressure, the impacts of BUDGET_DEFICIT were both negative and significant in columns (1) and (2), implying that the Ministry of Finance’s requirement for fiscal affordability assessments could play an important role in standardizing PPP management. The impacts of DEBT were different and significantly positive in column (2), suggesting that cities were more willing to adopt PPP when faced with higher off-budgetary pressure, which may have led to a higher level of inappropriate development of PPP.

In terms of institutional environment, the PRIVATERATIO was not significant in the withdrawn projects, but significantly positive in the active projects, which means that the higher the development level of the private sector, the higher the quality of PPP projects initiated by local governments.

In columns (3) and (4), we checked the factors influencing the amount of withdrawn economic and social infrastructure projects, respectively. The empirical results were similar and showed that local governments with lower budget deficits or higher off-budgetary debts initiated more PPP projects that were later withdrawn. According to the standardized coefficient, the impact of budget deficits and off-budgetary debts on economic infrastructure was greater than that on social infrastructure, which means that local governments, driven by fiscal pressure, were more willing to take risks in projects that could promote economic growth in the short term.

6. Conclusions and Policy Implications

Based on the unique data of all cities at the prefecture level or above in China from 2014 to 2017, we investigated the factors influencing PPP adoption by Chinese local governments. From the perspective of infrastructure shortages, the impacts of the demand for public services and infrastructure were not significant. In terms of financial resources, the empirical results emphasized the opposite influence of budgetary deficits and off-budgetary debts: cities with a higher budgetary deficit initiated fewer PPP projects according to the requirement for fiscal affordability assessment, but cities with a higher off-budgetary debt initiated more PPP projects. The empirical analysis also revealed the positive influence of the development of private sector on PPP adoption. We shed light on the impact of these factors on the type of PPP projects initiated by local governments. We found that cities with a higher off-budgetary debt and a lower budgetary deficit initiated more PPP projects later withdrawn by local governments.

This study provides a comprehensive review and reliable empirical analysis regarding the adoption of PPP by China’s local governments, yielding two main policy implications for further promoting the efficiency of PPP development.

First, local infrastructure shortage has little impact on the adoption of PPP, indicating that the purpose of local governments adopting PPP is not to improve the quantity of public service supply, which is contrary to the original intention of PPP development in theory. Local governments should further enhance the evaluation of infrastructure supply, while also improving and implementing the planning of public service facilities in accordance with the actual demands of local residents. When local governments initiate PPP projects, they should be consistent with the planning of public services to promote sustainable development.

Second, local governments with a higher off-budgetary debt will initiate more PPP projects, especially inappropriate PPP projects that are withdrawn later. Although PPP can alleviate local governments’ fiscal pressure through attracting private sectors to provide public services, many PPP projects will still require either government payment or subsidies in the future. Therefore, the abuse of PPP may increase the local governments’ potential debt, and the central government should strengthen the supervision of off-balance-sheet financing of local governments and both strictly and rationally control the scale of PPP investment. When completing fiscal affordability assessments, the central government should not only pay attention to the budgetary revenue and expenditure, but also consider the off-balance-sheet debt of local governments.

Although this study provides one of the first empirical analysis on the factors affecting local governments’ PPP adoption in China, there are still some limitations. First of all, due to the lag of macro-economic data update, we only analyzed the development of PPP from 2014 to 2017. A future study will analyze PPP development in China from a longer period, so as to better identify the mechanism of the factors. Secondly, due to the lack of direct indicator for the sustainability of PPP development, this study adopted the scale of PPP projects withdrawn by government as the proxy. Considering the complexity of definition for sustainability, other aspects of sustainability of PPP development will be analyzed, such as the performance of PPP projects.

Author Contributions

The authors equally contributed to the development of this research. Specially, B.Z. and J.W. conceived the study; B.Z. conducted data analysis and prepared the first draft; and L.Z., J.W., and S.W. proposed the research idea, developed the theoretical model, provided financial support, and revised it critically. All authors reviewed and approved the final manuscript.

Funding

This study is financially supported by the National Natural Science Foundation of China (71874093, 71772098, 71572089, and 91546113).

Acknowledgments

All authors acknowledge with gratitude all reviewers.

Conflicts of Interest

The authors have no conflicts of interests with any parties.

References

- Hodge, G.A.; Greve, C. Public–private partnerships: An international performance review. Public Admin. Rev. 2007, 67, 545–558. [Google Scholar] [CrossRef]

- Ke, Y.; Wang, S.; Chan, A.; Lam, P.T. Preferred risk allocation in China’s public–private partnership (PPP) projects. Int. J. Proj. Manag. 2010, 28, 482–492. [Google Scholar] [CrossRef]

- Cheng, Z.; Ke, Y.; Lin, J.; Yang, Z.; Cai, J. Spatio-temporal dynamics of public private partnership projects in China. Int. J. Proj. Manag. 2016, 34, 1242–1251. [Google Scholar] [CrossRef]

- Chen, C.; Li, D.; Man, C. Toward Sustainable Development? A Bibliometric Analysis of PPP-Related Policies in China between 1980 and 2017. Sustainability 2019, 11, 142. [Google Scholar] [CrossRef]

- Tan, J.; Zhao, J.Z. The Rise of Public–Private Partnerships in China: An Effective Financing Approach for Infrastructure Investment? Public Admin. Rev. 2019. [Google Scholar] [CrossRef]

- Wang, H.M.; Xiong, W.; Wu, G.D.; Zhu, D.J. Public-private partnership in Public Administration discipline: A literature review. Public Manag. Rev. 2018, 20, 293–316. [Google Scholar] [CrossRef]

- Zheng, S.; Xu, K.; He, Q.; Fang, S.; Zhang, L. Investigating the sustainability performance of ppp-type infrastructure projects: A case of China. Sustainability 2018, 10, 4162. [Google Scholar] [CrossRef]

- Ross, T.W.; Yan, J. Comparing Public–Private Partnerships and Traditional Public Procurement: Efficiency vs. Flexibility. J. Comp. Policy Anal. Res. Pract. 2015, 17, 448–466. [Google Scholar] [CrossRef]

- Fernandes, C.; Ferreira, M.; Moura, F. PPPs—True Financial Costs and Hidden Returns. Transp. Rev. 2016, 36, 207–227. [Google Scholar] [CrossRef]

- Slavov, S.N. Public Versus Private Provision of Public Goods. J. Public Econ. 2014, 16, 222–258. [Google Scholar] [CrossRef]

- Biondi, Y. Cost of capital, discounting and relational contracting: Endogenous optimal return and duration for joint investment projects. Appl. Econ. 2011, 43, 4847–4864. [Google Scholar] [CrossRef]

- Wang, G.; Xue, Y.; Skibniewski, M.; Song, J.; Lu, H. Analysis of Private Investors Conduct Strategies by Governments Supervising Public-Private Partnership Projects in the New Media Era. Sustainability 2018, 10, 4723. [Google Scholar] [CrossRef]

- Chou, J.S.; Pramudawardhani, D. Cross-country comparisons of key drivers, critical success factors and risk allocation for public-private partnership projects. Int. J. Proj. Manag. 2015, 33, 1136–1150. [Google Scholar] [CrossRef]

- Heald, D. Value for money tests and accounting treatment in PFI schemes. Account. Audit. Account. J. 2003, 16, 342–371. [Google Scholar] [CrossRef]

- Odoemena, A.T.; Horita, M.A. Strategic analysis of contract termination in public–private partnerships: Implications from cases in sub-Saharan Africa. Constr. Manag. Econ. 2018, 36, 96–108. [Google Scholar] [CrossRef]

- Yehoue, M.E.B.; Hammami, M.; Ruhashyankiko, J.F. Determinants of Public-Private Partnerships in Infrastructure; International Monetary Fund: Washington, DC, USA, 2006. [Google Scholar]

- Albalate, D.; Bel, G.; Geddes, R.R. Recovery risk and labor costs in public–private partnerships: Contractual choice in the US water industry. Local Gov. Stud. 2013, 39, 332–351. [Google Scholar] [CrossRef]

- Girth, A.M. What Drives the Partnership Decision? Examining Structural Factors Influencing Public-Private Partnerships for Municipal Wireless Broadband. Int. Public Manag. J. 2014, 17, 344–364. [Google Scholar] [CrossRef]

- Wang, Y.; Zhao, Z.J. Motivations, obstacles, and resources: Determinants of public-private partnership in state toll road financing. Public Perform. Manag. Rev. 2014, 37, 679–704. [Google Scholar] [CrossRef]

- Yang, Y.; Hou, Y.; Wang, Y. On the Development of Public–Private Partnerships in Transitional Economies: An Explanatory Framework. Public Admin. Rev. 2013, 73, 301–310. [Google Scholar] [CrossRef]

- Scott, W.R. Organizations and Organizing: Rational, Natural and Open Systems Perspectives; Routledge: Abingdon upon Thames, UK, 2015. [Google Scholar]

- Shen, L.; Tam, V.W.; Gan, L.; Ye, K.; Zhao, Z. Improving sustainability performance for public-private-partnership (PPP) projects. Sustainability 2016, 8, 289. [Google Scholar] [CrossRef]

- Démurger, S. Infrastructure development and economic growth: An explanation for regional disparities in China? J. Comp. Econ. 2001, 29, 95–117. [Google Scholar] [CrossRef]

- Cong, X.; Ma, L. Performance evaluation of public-private partnership projects from the perspective of efficiency, economic, effectiveness, and equity: A study of residential renovation projects in China. Sustainability 2018, 10, 1951. [Google Scholar] [CrossRef]

- Cui, C.; Liu, Y.; Hope, A.; Wang, J. Review of studies on the public–private partnerships (PPP) for infrastructure projects. Int. J. Proj. Manag. 2018, 36, 773–794. [Google Scholar] [CrossRef]

- Berry, F.S.; Berry, W.D. State lottery adoptions as policy innovations: An event history analysis. Am. Polit. Sci. Rev. 1990, 84, 395–415. [Google Scholar] [CrossRef]

- English, L.M.; Guthrie, J. Driving privately financed projects in Australia: What makes them tick? Account. Audit. Account. J. 2003, 16, 493–511. [Google Scholar] [CrossRef]

- Glasser, B.L. Economic Development and Political Reform: The Impact of External Capital on the Middle East; Edward Elgar Publishing: Trotterham, UK, 2001. [Google Scholar]

- Liang, Y.; Shi, K.; Wang, L.; Xu, J. Local Government Debt and Firm Leverage: Evidence from China. Asian Econ. Policy R. 2017, 12, 210–232. [Google Scholar] [CrossRef]

- Panayides, P.M.; Parola, F.; Lam, J.S.L. The effect of institutional factors on public–private partnership success in ports. Transp. Res. Part A Policy Pract. 2015, 71, 110–127. [Google Scholar] [CrossRef]

- Zhang, S.; Gao, Y.; Feng, Z.; Sun, W. PPP Application in Infrastructure Development in China: Institutional Analysis and Implications. Int. J. Proj. Manag. 2015, 33, 497–509. [Google Scholar] [CrossRef]

- Henisz, W.J. The institutional environment for economic growth. Econ. Polit. 2000, 12, 1–31. [Google Scholar] [CrossRef]

- Van Ham, H.; Koppenjan, J. Building public-private partnerships: Assessing and managing risks in port development. Public Manag. Rev. 2001, 3, 593–616. [Google Scholar] [CrossRef]

- Brewer, B.; Hayllar, M.R. CAPAM Symposium on Networked Government: Building public trust through public–private partnerships. Int. Rev. Adm. Sci. 2005, 71, 475–492. [Google Scholar] [CrossRef]

- Sanghi, A.; Sundakov, A.; Hankinson, D. Designing and Using Public-Private Partnership Units in Infrastructure: Lessons from Case Studies around the World; PPIAF—GRIDLINES; World Bank: Washington, DC, USA, 2007; pp. 1–5. [Google Scholar]

- Xu, C. The Fundamental Institutions of China’s Reforms and Development. J. Econ. Lit. 2011, 49, 1076–1151. [Google Scholar] [CrossRef]

- Bucovetsky, S. Public input competition. J. Public Econ. 2005, 89, 1763–1787. [Google Scholar] [CrossRef]

- Cai, H.; Treisman, D. Does competition for capital discipline governments? Decentralization, globalization, and public policy. Am. Econ. Rev. 2005, 95, 817–830. [Google Scholar] [CrossRef]

- Keen, M.; Marchand, M. Fiscal competition and the pattern of public spending. J Public. Econ. 1997, 66, 33–53. [Google Scholar] [CrossRef]

- Bo, L.; Mear, F.C.; Huang, J. New Development: China’s Debt Transparency and the Case of Urban Construction Investment Bonds. Public Money Manag. 2017, 37, 225–230. [Google Scholar] [CrossRef]

- Bai, C.; Hsieh, C.; Zheng, M. The Long Shadow of a Fiscal Expansion; National Bureau of Economic Research: Cambridge, MA, USA, 2016. [Google Scholar]

- Jin, H.; Qian, Y.; Weingast, B.R. Regional decentralization and fiscal incentives: Federalism, Chinese style. J. Public Econ. 2005, 89, 1719–1742. [Google Scholar] [CrossRef]

- Tao, R.; Su, F.; Liu, M.; Cao, G. Land leasing and local public finance in China’s regional development: Evidence from prefecture-level cities. Urban Stud. 2010, 47, 2217–2236. [Google Scholar]

- Wu, Q.; Li, Y.; Yan, S. The incentives of China’s urban land finance. Land Use Policy 2015, 42, 432–442. [Google Scholar] [CrossRef]

- Azuma, Y.; Kurihara, J. Examining China’s Local Government Fiscal Dynamics: With a Special Emphasis on Local Investment Companies (LICs)’. Politico-Econ. Comment. 2011, 5, 121–140. [Google Scholar]

- Fan, J.P.; Rui, O.M.; Zhao, M. Public governance and corporate finance: Evidence from corruption cases. J. Comp. Econ. 2008, 36, 343–364. [Google Scholar] [CrossRef] [Green Version]

- Li, K.; Yue, H.; Zhao, L. Ownership, institutions, and capital structure: Evidence from China. J. Comp. Econ. 2009, 37, 471–490. [Google Scholar] [CrossRef]

- Fan, G.; Wang, X.; Zhu, H. NERI Index of Marketization of China’s Provinces; National Economic Research Institute: Beijing, China, 2003. [Google Scholar]

- McDonald, J.F.; Moffitt, R.A. The Uses of Tobit Analysis. Rev. Econ. Stat. 1980, 62, 318–321. [Google Scholar] [CrossRef]

Figure 1.

Distribution of public–private partnership (PPP) projects during 2014–2017.

Figure 2.

Cumulative proportion of PPP initiated by cities.

Figure 3.

Distribution of withdrawn PPP projects.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Definition and summary statistics of all the variables.

| Variable | Definition | N | Mean | SD | Min | Max |

|---|---|---|---|---|---|---|

| Dependent Variables | ||||||

| INVEST_PPP | Per capita investment in PPP initiated by local governments; in 104 RMB | 1144 | 0.308 | 0.609 | 0 | 9.296 |

| INVEST_ECO | Per capita investment in PPP for economic infrastructure initiated by local governments; in 104 RMB | 1144 | 0.268 | 0.548 | 0 | 7.456 |

| INVEST_SOC | Per capita investment in PPP for social infrastructure initiated by local governments; in 104 RMB | 1144 | 0.040 | 0.100 | 0 | 1.839 |

| WITHDRAW | Per capita investment in PPP for those projects that are withdrawn by their initiator; in 104 RMB | 1144 | 0.130 | 0.464 | 0 | 8.986 |

| NWITHDRAW | Per capita investment in PPP for those projects that are not withdrawn by their initiator; in 104 RMB | 1144 | 0.178 | 0.296 | 0 | 2.902 |

| WITHDRAW_ECO | Per capita investment in PPP for those economic projects that are withdrawn by their initiator; in 104 RMB | 1144 | 0.115 | 0.420 | 0 | 7.388 |

| WITHDRAW_SOC | Per capita investment in PPP for those economic projects that are withdrawn by their initiator; in 104 RMB | 1144 | 0.152 | 0.269 | 0 | 2.885 |

| Infrastructure Shortage (IS) | ||||||

| GDPPC | Per capita gross domestic product (GDP); in 104 RMB | 1144 | 6.175 | 3.608 | 0.413 | 43.932 |

| D_GDPPC | Growth rate in annual per capita GDP | 1144 | 0.073 | 0.449 | −0.903 | 9.511 |

| INFRA_STOCK | The ratio of fiscal expenditure for construction, maintenance, and management of public services to GDP | 1144 | 0.046 | 0.078 | 0.000 | 1.305 |

| Financial Pressure (FP) | ||||||

| BUDGET_DEFICIT | Gap between fiscal revenue and fiscal expenditure accounts for the proportion of fiscal expenditure | 1144 | 0.514 | 0.231 | −1.107 | 0.925 |

| LAND_REVENUE | Ratio of land grant premiums to fiscal revenue | 1144 | 0.538 | 0.388 | 0.009 | 3.495 |

| DEBT | Ratio of total local government financial vehicle (LGFV) debts to GDP | 1144 | 0.177 | 0.218 | 0 | 1.521 |

| Institution Environment (IE) | ||||||

| MARKETIZATION | Index of marketization for China’s provinces calculated by Fan and Wang (2014) to capture regional disparity | 1144 | 6.946 | 1.555 | 0.620 | 9.780 |

| PRIVATERATIO | Ratio of private sectors’ employees to the total working population | 1144 | 0.916 | 0.408 | 0.056 | 3.135 |

| INTEGRITY | The government integrity index compiled by the Renmin University of China based on the data of 2016, including two main aspects: the fiscal transparency and the level of anti-corruption | 1144 | 0.216 | 0.197 | 0.003 | 1.000 |

| Control variable | ||||||

| lnPOP_UR | Logarithmic form of the permanent urban population at end of the year; in 104 RMB | 1144 | 5.260 | 0.781 | 3.213 | 7.838 |

Table 2.

Empirical results of the impact of factors on public–private partnership (PPP) projects initiated by local governments.

Table 2.

Empirical results of the impact of factors on public–private partnership (PPP) projects initiated by local governments.

| (1) | (2) | (3) | |

|---|---|---|---|

| Variable | INVEST_PPP | INVEST_ECO | INVEST_SOC |

| GDPPC | −0.002 | −0.002 | 0.000 |

| (−0.261) | (−0.367) | (0.431) | |

| D_GDPPC | 0.028 | 0.026 | 0.002 |

| (0.708) | (0.716) | (0.330) | |

| INFRA_STOCK | −0.278 | −0.270 | −0.008 |

| (−1.151) | (−1.227) | (−0.201) | |

| BUDGET_DEFICIT | −0.512 *** | −0.462 *** | −0.050 ** |

| (−4.080) | (−4.043) | (−2.360) | |

| LAND_REVENUE | 0.025 | 0.021 | 0.004 |

| (0.477) | (0.431) | (0.503) | |

| DEBT | 0.277 *** | 0.273 *** | 0.004 |

| (2.762) | (2.985) | (0.260) | |

| MARKETIZATION | −0.022 | −0.028 | 0.006 |

| (–0.272) | (–0.382) | (0.446) | |

| PRIVATERATIO | 0.102 ** | 0.088 ** | 0.014 * |

| (2.263) | (2.154) | (1.791) | |

| INTEGRITY | −0.004 | −0.004 | 0.000 |

| (−0.985) | (−1.083) | (0.009) | |

| lnPOP_UR | −0.144 *** | −0.122 *** | −0.023 *** |

| (−4.897) | (−4.531) | (−4.570) | |

| Constant | 1.219 ** | 1.124 ** | 0.095 |

| (2.233) | (2.261) | (1.028) | |

| 0.520 *** | 0.474 *** | 0.088 *** | |

| (47.833) | (47.833) | (47.833) | |

| PRO FE | Yes | Yes | Yes |

| YEAR FE | Yes | Yes | Yes |

| Observations (N) | 1144 | 1144 | 1144 |

| Log-likelihood | −875.416 | −768.361 | 1160.349 |

| χ2 | 424.947 | 384.642 | 335.123 |

Notes: z-statistics are in parentheses; *** p < 0.01; ** p < 0.05; * p < 0.1.

Table 3.

Empirical results of the factors impacting the withdrawal of PPP projects.

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variable | NWITHDRAW | WITHDRAW | WITHDRAW_ECO | WITHDRAW_SOC |

| GDPPC | −0.003 | 0.001 | 0.002 | −0.001 |

| (−0.748) | (0.255) | (0.397) | (−0.844) | |

| D_GDPPC | 0.035 | −0.007 | −0.008 | 0.001 |

| (1.597) | (−0.243) | (−0.303) | (0.209) | |

| INFRA_STOCK | −0.048 | −0.222 | −0.213 | −0.011 |

| (−0.349) | (−1.154) | (−1.232) | (−0.416) | |

| BUDGET_DEFICIT | −0.209 *** | −0.297 *** | −0.268 *** | −0.030 ** |

| (−2.945) | (−2.966) | (−2.973) | (−2.204) | |

| LAND_REVENUE | −0.018 | 0.042 | 0.040 | 0.003 |

| (−0.587) | (1.008) | (1.050) | (0.463) | |

| DEBT | 0.055 | 0.221 *** | 0.198 *** | 0.023 ** |

| (0.969) | (2.713) | (2.711) | (2.085) | |

| MARKETIZATION | −0.012 | −0.010 | −0.010 | 0.001 |

| (−0.261) | (−0.145) | (−0.178) | (0.092) | |

| PRIVATERATIO | 0.060 ** | 0.041 | 0.034 | 0.008 |

| (2.341) | (1.114) | (1.025) | (1.524) | |

| INTEGRITY | −0.002 | −0.002 | −0.002 | −0.000 |

| (−0.804) | (−0.648) | (−0.712) | (−0.080) | |

| lnPOP_UR | −0.055 *** | −0.089 *** | −0.080 *** | −0.010 *** |

| (−3.284) | (−3.717) | (−3.707) | (−2.928) | |

| Constant | 0.520 * | 0.691 | 0.638 | 0.055 |

| (1.680) | (1.552) | (1.600) | (0.913) | |

| 0.295 *** | 0.396 *** | 0.361 *** | 0.056 *** | |

| (47.833) | (41.404) | (41.402) | (41.410) | |

| PRO FE | Yes | Yes | Yes | Yes |

| YEAR FE | Yes | Yes | Yes | Yes |

| Observations (N) | 1144 | 1144 | 1144 | 1144 |

| Log-likelihood | −225.475 | −584.461 | −473.505 | 1670.281 |

| χ2 | 515.654 | 184.915 | 184.956 | 142.667 |

Notes: z-statistics are in parentheses; *** p < 0.01; ** p < 0.05; * p < 0.1.

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Zhang, B.; Zhang, L.; Wu, J.; Wang, S. Factors Affecting Local Governments’ Public–Private Partnership Adoption in Urban China. Sustainability 2019, 11, 6831. https://doi.org/10.3390/su11236831

AMA Style

Zhang B, Zhang L, Wu J, Wang S. Factors Affecting Local Governments’ Public–Private Partnership Adoption in Urban China. Sustainability. 2019; 11(23):6831. https://doi.org/10.3390/su11236831

Chicago/Turabian StyleZhang, Bo, Li Zhang, Jing Wu, and Shouqing Wang. 2019. "Factors Affecting Local Governments’ Public–Private Partnership Adoption in Urban China" Sustainability 11, no. 23: 6831. https://doi.org/10.3390/su11236831

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.