Financial Technology and Its Impact on Digital Literacy in India: Using Poverty as a Moderating Variable

,

,  , ,

, ,

Abstract

:1. Introduction

2. Literature Review and Hypotheses Formulation

2.1. FinTech and Financial Inclusion

2.2. FinTech and Digital Literacy

2.3. FinTech, Digital Literacy, and Poverty

3. Data and Methodology

3.1. Data Sourcing for the Study

3.2. Methodology Employed for the Study

3.3. Descriptive Statistics and Correlation Matrix

4. Regression Analysis

4.1. Static Panel Data Regression Analysis

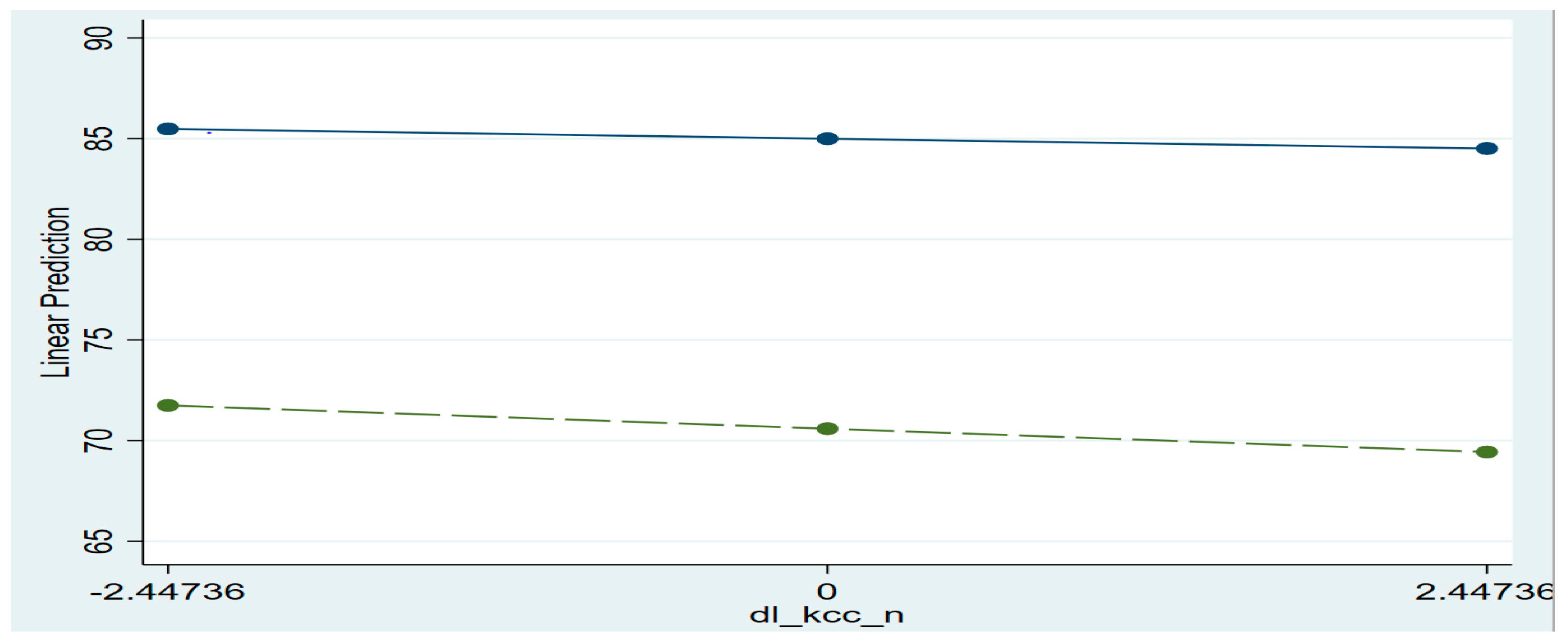

4.2. Interaction Graphs

4.3. Robustness of the Regression ResultsRobustness Tests Determine How Specific Core

Regression coefficients behave when the regression specification changes by adding or removing Regressors. If the estimated regression coefficients’ signs and magnitudes are also plausible, it is commonly assumed that the estimated regression coefficients can be reliably interpreted as the true causal effects of the associated regressors

4.4. Test Results for Endogeneity

5. Discussion

6. Conclusions and Future Scope

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Anagnostopoulos, Ioannis. 2018. Fintech and regtech: Impact on regulators and banks. Journal of Economics and Business 100: 7–25. [Google Scholar] [CrossRef]

- Anand, S. Kodan, and Kuldip S. Chhikara. 2013. A theoretical and quantitative analysis of financial inclusion and economic growth. Management and Labour Studies 38: 103–33. [Google Scholar]

- Arner, Douglas W., Janos Barberis, and Ross P. Buckley. 2015. The evolution of Fintech: A new post-crisis paradigm. Geo. J. Int’l L 47: 1271. [Google Scholar] [CrossRef] [Green Version]

- Babcock, Lee H. 2015. Mobile Payments: How Digital Finance Is Transforming Agriculture. Value Chains and Trade Series; Wageningen. Available online: https://cgspace.cgiar.org/handle/10568/75499 (accessed on 3 January 2022).

- Baltagi, Badi Hani. 2008. Econometric Analysis of Panel Data. Chichester: John Wiley & Sons, West Sussex England, Available online: http://www.spss-pasw.ir/upload/images/3ax38cld271xe0bx00z.pdf (accessed on 12 December 2021).

- Bank, N. R. 2020. Financial Literacy Framework. Available online: http://archive.nrb.org.np/finlit/cms_uploads/Financial%20Literacy%20Framework_20770114.pdf (accessed on 15 February 2022).

- Bazalgette, Cary. 1988. They changed the picture in the middle of the fight: New kinds of literacy. Language and Literacy in the Primary School, 211–23. [Google Scholar]

- Buckingham, David. 1993. Changing Literacies: Media Education and Modern Culture. London: Tufnell Press. [Google Scholar]

- Cahyani, Yutisa Tri, Lukman Santoso, and Tunjung Genarsih. 2021. Financial Technology Literacy (Fintech) in Ponorogo: Perception and Attitude. In Paper presensted at the ICIS 2020: Proceedings of the 2nd International Conference on Islamic Studies, ICIS 2020, Ponorogo, Indonesia, October 27–28; p. 203. [Google Scholar]

- Dixit, Radhika, and Munmun Ghosh. 2013. Financial inclusion for inclusive growth of India-A study of Indian states. International Journal of Business Management & Research 3: 147–56. [Google Scholar]

- Goswami, Himakshi. 2016. Opportunities and challenges of digital India programme. International Education and Research Journal 2: 78–79. [Google Scholar]

- Gozgor, Giray, Chi Keung Marco Lau, and Zhou Lu. 2018. Energy consumption and economic growth: New evidence from the OECD countries. Energy 153: 27–34. [Google Scholar] [CrossRef] [Green Version]

- Gupta, Pallavi, and Bharti Singh. 2013. Role of literacy level in financial inclusion in India: Empirical evidence. Europe 1: 272–76. Available online: http://www.joebm.com/papers/59-X10007.pdf (accessed on 4 December 2021). [CrossRef] [Green Version]

- Hsiao, Cheng. 2007. Panel data analysis—Advantages and challenges. Test 16: 1–22. [Google Scholar] [CrossRef] [Green Version]

- Kollinal, Reji K., John S. Moolakkattu, and Varghese Paul. 2019. Digital India-the Great Dream. International Journal of Computer Engineering and Technology 10: 87–93. [Google Scholar] [CrossRef]

- Kuknor, Sunaina, and Shailesh Rastogi. 2021. Determinants of Profitability in Indian Banks: A Panel Data Analysis. International Journal of Modern Agriculture 10: 978–86. [Google Scholar]

- Kumar, Ashwani, and Hariom Gupta. 2019. Financial Inclusion and Farmers: Association between Status and Demographic Variables. International Journal of Recent Technology and Engineering (IJRTE) 8: 5868–79. [Google Scholar] [CrossRef]

- Lee, In, and Yong Jae Shin. 2018. Fintech: Ecosystem, business models, investment decisions, and challenges. Business Horizons 61: 35–46. [Google Scholar] [CrossRef]

- Liew, Teo-Piaw, Pei-Wen Lim, and Yew-Chui Liu. 2020. Digital financial literacy: A case study of farmers from rural areas in Sarawak. International Journal of Education and Pedagogy 2: 245–51. [Google Scholar]

- Lu, Xun, and Halbert White. 2014. Robustness checks and robustness tests in applied economics. Journal of Econometrics 178: 194–206. [Google Scholar] [CrossRef]

- Lumenta, Ulrigh Z., and Frederik G. Worang. 2019. The Influence of Financial Inclusion on The Performance of Micro Small and Medium Enterprises in North Sulawesi. Jurnal EMBA: Jurnal Riset Ekonomi, Manajemen, Bisnis dan Akuntansi 7: 2910–8. [Google Scholar]

- Maripally, Anurag, and Larry Bridwell. 2017. The future of financial inclusion and its impact on poverty reduction in India. American Society for Competitiveness 15: 329–35. [Google Scholar]

- Martin, Allan. 2006. A European framework for digital literacy. Nordic Journal of Digital Literacy 1: 151–61. [Google Scholar] [CrossRef]

- Martin, Allan, and Jan Grudziecki. 2006. DigEuLit: Concepts and tools for digital literacy development. Innovation in Teaching and Learning in Information and Computer Sciences 5: 249–67. [Google Scholar] [CrossRef]

- McAuley, D. 2015. What is FinTech? Available online: https://www.whartonfintech.org/ (accessed on 22 October 2015).

- Morgan, Peter J., Bihong Huang, and Long Q. Trinh. 2019. The Need to Promote Digital Financial Literacy for the Digital Age. In Realizing Education for All in The Digital Age. Tokyo: Asian Development Bank Institute, pp. 40–46. [Google Scholar]

- Nedungadi, Prema P., Rajani Menon, Georg Gutjahr, Lynnea Erickson, and Raghu Raman. 2018. Towards an inclusive digital literacy framework for digital India. Education+ Training 60: 516–28. [Google Scholar] [CrossRef]

- OECD. 2018. G20/OECD INFE Policy Guidance on Digitalisation and Financial Literacy. The Secretary-General of the OECD, Australi. Paris: OECD. [Google Scholar]

- Pangrazio, Luciana. 2016. Reconceptualizing critical digital literacy. Discourse: Studies in the Cultural Politics of Education 37: 163–74. [Google Scholar]

- Panos, Georgios A., and John O. S. Wilson. 2020. Financial Literacy and responsible finance in the FinTechEra: Capabilities and Challenges. The European Journal of Finance 26: 297–301. [Google Scholar] [CrossRef] [Green Version]

- Potrich, Ani Caroline Grigion, Kelmara Mendes Vieira, and Guilherme Kirch. 2015. Determinants of Financial Literacy: Analysis of The Influence of Socioeconomic and Demographic Variables. Revista Contabilidade & Finanças 26: 362–77. [Google Scholar]

- Prasad, Hanuman, Devendra Meghwal, and Vijay Dayama. 2017. Digital Financial Literacy: A Study of Households of Udaipur. Global Journal of Advanced Research 4: 201–9. [Google Scholar]

- Prasad, Hanuman, Devendra Meghwal, and Vijay Dayama. 2018. Digital financial literacy: A study of households of Udaipur. Journal of Business and Management 5: 23–32. [Google Scholar]

- Rastogi, Shailesh, Arpita Sharma, Chetan Panse, and Venkata Mrudula Bhimavarapu. 2021. Unified Payment Interface (UPI): A Digital Innovation and Its Impact on Financial Inclusion and Economic Development. Universal Journal of Accounting and Finance 9: 518–30. [Google Scholar] [CrossRef]

- Rastogi, Shailesh, Vidya Suresh, and David Leonard. 2017. Financial Inclusion and Demonetization: An Empirical Study Using Exploratory Factor Analysis. Indian Journal of Commerce & Management Studies 8: 38–46. [Google Scholar]

- RBI (Reserve Bank of India-State Wise and Region Wise Deployment of ATMs). 2019. Available online: https://rbi.org.in/Scripts/StateRegionATMView.aspx (accessed on 12 July 2021).

- RBI (Reserve Bank of India-Publications). 2020. Available online: https://www.rbi.org.in/scripts/PublicationsView.aspx?id=20275 (accessed on 12 July 2021).

- Senyo, Prince Kwame, Ellis LC Osabutey, and Konan A. Seny Kan. 2020. Pathways to improving financial inclusion through mobile money: A fuzzy set qualitative comparative analysis. Information Technology and People 34: 1997–2017. [Google Scholar] [CrossRef]

- Sharma, Arpita, Shailesh Rastogi, and Nishu Gupta. 2020. Financial Efficiency of Non–Banking Financial Companies-Microfinance Institutions: A Data Envelopment Analysis. Test Engineering and Management 83: 9080–91. [Google Scholar]

- Shen, Yan, Wenxiu Hu, and C. James Hueng. 2018. The effects of financial literacy, digital financial product usage and internet usage on financial inclusion in China. Paper presented at the MATEC Web of Conferences, Lisbon, Portugal, September 23–25; vol. 228, p. 05012. [Google Scholar]

- Singh, Charan, and Gopal Naik. 2018. Financial inclusion after PMJDY: A case study of Gubbi Taluk, Tumkur. IIM Bangalore Research Paper, 1–64. [Google Scholar] [CrossRef]

- Suryono, Ryan Randy, Indra Budi, and Betty Purwandari. 2020. Challenges and trends of financial technology (Fintech): A systematic literature review. Information 11: 590. [Google Scholar] [CrossRef]

- Sushma, S. J., and S. P. Kumar. 2019. A novel approach to jointly address localization and classification of breast cancer using bio-inspired approach. International Journal of Electrical and Computer Engineering 9: 992. [Google Scholar]

- Tripathi, Meenal, and Monica Dungarwal. 2020. Digital India: Role in development. International Journal of Home Science 6: 388–92. Available online: https://www.homesciencejournal.com/archives/2020/vol6issue2/PartG/6-2-72-511.pdf (accessed on 14 June 2022).

- Tyner, Kathleen. 1998. Literacy in a Digital World. Mahwah: Erlbaum. [Google Scholar]

- Wooldridge, Jeffrey M. 2003. Introductory Econometrics: A Modern Approach, 2nd ed. Thomson: Mason. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Variable Name | Symbol | Description | Data Source |

|---|---|---|---|

| Literacy rate | lr | The literacy rate measures the percentage of people who are digitally literate about digital financial services. | www.timesnownews.com. Accessed on 16 October 2021 |

| Number of ATMs | l_atm | The natural logarithm of the number of ATMs considered for the study is situated in 29 states and two union territories in India. | RBI (2019) report |

| Number of Kisan credit cards | l_KCC_n | Natural logarithm number of Kisan Credit Cards (KCCs) from 29 Indian states and two union territories. | RBI (2020) report |

| Amount of Kisan credit cards | l_KCC_amt | Natural logarithm of the amount of Kisan Credit Cards (KCCs) from 29 states and two union territories of India | RBI (2020) report |

| The interaction term of poverty score and number of ATMs | l_ps_atm | The interaction term is obtained by multiplying the natural logarithm of poverty score and ATMs. (l_ps*l_atm) | -- |

| The interaction term of poverty score and the number of Kisan credit cards | l_ps_KCC_n | The interaction term is obtained by multiplying natural logarithm of poverty score and number of Kisan credit cards (l_ps*l_KCC_n) | -- |

| The interaction term of poverty score and amount of Kisan credit cards | l_ps_KCC_amt | The interaction term is obtained by multiplying natural logarithm of poverty score and amount of Kisan credit cards (l_ps*l_KCC_amt) | -- |

| Descriptive Statistics | ||||

|---|---|---|---|---|

| Mean | SD | Min | Max | |

| lr | 78.016 | 7.9937 | 61.8 | 96.2 |

| l_atm | 9.3425 | 1.6526 | 6.1003 | 11.612 |

| l_KCC_n | 13.049 | 2.4474 | 8.2941 | 16.301 |

| l_KCC_amt | 12.851 | 2.6376 | 7.3524 | 16.241 |

| l_ps_atm | 13.396 | 1.6338 | 10.165 | 15.891 |

| l_ps_KCC_n | 17.103 | 2.4199 | 12.206 | 20.275 |

| l_ps_KCC_amt | 16.905 | 2.6141 | 11.444 | 20.335 |

| Correlation Matrix | |||||||

|---|---|---|---|---|---|---|---|

| lr | l_atm | l_KCC_n | l_KCC_amt | l_ps_atm | l_ps_KCC_n | l_ps_KCC_amt | |

| lr | 1 | ||||||

| l_atm | 0.9346 * (0.0000) | 1 | |||||

| l_KCC_n | 0.9356 * (0.0000) | 0.9165 * (0.0000) | 1 | ||||

| l_KCC_amt | 0.9258 * (0.0000) | 0.9471 * (0.0000) | 0.9717 * (0.0000) | 1 | |||

| l_ps_atm | 0.9120 * (0.0000) | 0.9927 * (0.0000) | 0.9054 * (0.0000) | 0.9391 * (0.0000) | 1 | ||

| l_ps_KCC_n | 0.9237 * (0.0000) | 0.9142 * (0.0000) | 0.9967 * (0.0000) | 0.9700 * (0.0000) | 0.9128 * (0.0000) | 1 | |

| l_ps_KCC_amt | 0.9133 * (0.0000) | 0.9439 * (0.0000) | 0.9670 * (0.0000) | 0.9972 * (0.0000) | 0.9449 * (0.0000) | 0.9713 * (0.0000) | 1 |

| LR. | Model 1 | Model 2 | ||||

|---|---|---|---|---|---|---|

| Coef. | Std. Err | p-Value | Coef. | Std. Err | p-Value | |

| constant | 91.88 * | 6.886 | 0.000 | 70.70 * | 1.929 | 0.000 |

| l_atm | −1.484 * | 0.7396 | 0.045 | -- | -- | -- |

| l_kcc_n | -- | -- | -- | 0.5608 * | 0.1478 | 0.001 |

| R-Square | 0.1505 | 0.2396 | ||||

| SE of Regression | 3.355 | 3.367 | ||||

| Note: No of observations (n) | 93 | 93 | ||||

| Degree of freedom | 61 | 61 | ||||

| F-test Fixed Effect | 13.11 * (0.0000) | 11.88 * (0.0000) | ||||

| Random Effect Test | 58.09 * (0.0000) | 52.31 * (0.0000) | ||||

| Hausman Test | 2.36 (0.1242) | 5.73 (0.0167) | ||||

| Wald test for Heteroscedasticity 1 | 24,678.60 * (0.0000) | 4.4 × 105 * (0.0000) | ||||

| Wooldridge Autocorrelation Test 2 AR (1) | 3.554 (0.0691) | 9.713 * (0.0040) | ||||

| LR. | Model 3 | Model 4 | ||||

|---|---|---|---|---|---|---|

| Coef. | Std. Err | p-Value | Coef. | Std. Err | p-Value | |

| Constant | 65.21 * | 4.376 | 0.000 | −31.64 | 45.10 | 0.488 |

| l_kcc_amt | 0.9962 * | 0.3405 | 0.006 | -- | -- | -- |

| l_ps_atm | -- | -- | -- | 8.186 * | 3.367 | 0.021 |

| R-Square | 0.2008 | 0.1164 | ||||

| SE of Regression | 3.367 | 2.920 | ||||

| Note: No of observations (n) | 93 | 93 | ||||

| Degree of freedom | 61 | 61 | ||||

| F-test Fixed Effect | 12.29 * (0.0000) | 18.88 * (0.0000) | ||||

| Random Effect Test | 55.85 * (0.0000) | 57.20 * (0.0000) | ||||

| Hausman Test | 3.02 (0.0823) | 19.67 * (0.0000) | ||||

| Wald test for Heteroscedasticity 1 | 3.8 × 105 * (0.0000) | 56,860.14 * (0.0000) | ||||

| Wooldridge Autocorrelation Test 2 AR (1) | 9.933 * (0.0037) | 2.466 (0.1268) | ||||

| LR. | Model 5 | Model 6 | ||||

|---|---|---|---|---|---|---|

| Coef. | Std. Err | p-Value | Coef. | Std. Err | p-Value | |

| Constant | 57.53 * | 0.5065 | 0.000 | 32.22 | 21.18 | 0.139 |

| l_ps_kcc_n | 1.198 * | 8.662 | 0.025 | -- | -- | -- |

| l_ps_kcc_amt | -- | -- | -- | 2.709 * | 1.252 | 0.039 |

| R-Square | 0.2119 | 0.1764 | ||||

| SE of Regression | 3.292 | 3.210 | ||||

| Note: No of observations (n) | 93 | 93 | ||||

| Degree of freedom | 61 | 61 | ||||

| F-test Fixed Effect | 13.11 * (0.0000) | 14.27 * (0.0000) | ||||

| Random Effect Test | 51.86 * (0.0000) | 55.18 * (0.0000) | ||||

| Hausman Test | 9.41 * (0.0022) | 10.50 * (0.0012) | ||||

| Wald test for Heteroscedasticity 1 | 2.7 × 105 * (0.0000) | 1.2 × 105 * (0.0000) | ||||

| Wooldridge Autocorrelation Test 2 AR (1) | 3.000 (0.0935) | 2.068 (0.1607) | ||||

| Core Variable | Max | Min | Mean | Avg STD | Perc Signi | Perc+ | Perc- | AvgT |

|---|---|---|---|---|---|---|---|---|

| l_atm | −1.4844 | −1.4844 | −1.4844 | 0.7632 | 0 | 0 | 1 | 1.9451 |

| l_kcc_n | −0.7905 | −0.7905 | −0.7905 | 0.4189 | 0 | 0 | 1 | 1.887 |

| l_kcc_amt | −0.9765 | −0.9765 | −0.9765 | 0.4471 | 1 | 0 | 1 | 2.1838 |

| l_ps_atm | 0.0762 | 0.0762 | 0.0762 | 0.8252 | 0 | 1 | 0 | 0.0923 |

| l_ps_kkc_n | −0.3921 | −0.3921 | −0.3921 | 0.4256 | 0 | 0 | 1 | 0.9215 |

| l_ps_kkc_amt | −0.5037 | −0.5037 | −0.5037 | 0.4664 | 0 | 0 | 1 | 1.0799 |

| Test | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 |

|---|---|---|---|---|---|---|

| Durbin Wu-Hausman chi2 test | 0.04792 (0.8267) | 0.084806 (0.7709) | 0.919438(0.3376) | 0.018272 (0.8925) | 0.122091 (0.7268) | 1.03308 (0.3094) |

| Durbin Wu-Hausman F- test | 0.043349 (0.8366) | 0.076809 (0.7837) | 0.855844 (0.3628) | 0.016514 (0.8987) | 0.110712 (0.7418) | 0.965276 (0.3343) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gautam, R.S.; Rastogi, S.; Rawal, A.; Bhimavarapu, V.M.; Kanoujiya, J.; Rastogi, S. Financial Technology and Its Impact on Digital Literacy in India: Using Poverty as a Moderating Variable. J. Risk Financial Manag. 2022, 15, 311. https://doi.org/10.3390/jrfm15070311

Gautam RS, Rastogi S, Rawal A, Bhimavarapu VM, Kanoujiya J, Rastogi S. Financial Technology and Its Impact on Digital Literacy in India: Using Poverty as a Moderating Variable. Journal of Risk and Financial Management. 2022; 15(7):311. https://doi.org/10.3390/jrfm15070311

Chicago/Turabian StyleGautam, Rahul Singh, Shailesh Rastogi, Aashi Rawal, Venkata Mrudula Bhimavarapu, Jagjeevan Kanoujiya, and Samaksh Rastogi. 2022. "Financial Technology and Its Impact on Digital Literacy in India: Using Poverty as a Moderating Variable" Journal of Risk and Financial Management 15, no. 7: 311. https://doi.org/10.3390/jrfm15070311