Heterogeneous Preferences for Selecting Attributes of Farmland Management Right Mortgages in Western China: A Demand Perspective

1

College of Economics, Sichuan Agricultural University, Chengdu 611130, China

2

Institute of Agricultural Economics and Development, Chinese Academy of Agricultural Sciences, Beijing 100081, China

*

Author to whom correspondence should be addressed.

Land 2022, 11(8), 1157; https://doi.org/10.3390/land11081157

Submission received: 23 June 2022

/

Revised: 20 July 2022

/

Accepted: 23 July 2022

/

Published: 26 July 2022

(This article belongs to the Section Land Socio-Economic and Political Issues)

Abstract

:Farmland management right mortgages (FMRMs) are emerging land financing products in China. However, the development of FMRMs and farmers’ demands for them are poorly understood. This study applied an in-the-field choice experiment of 1815 farmers, conducted in China, to examine farmers’ demands for FMRMs and explore their heterogeneous preferences regarding the attributes of FMRMs. Results from the random parameters logit model suggest that farmers are interest-rate sensitive and willing to pay for FMRM products that use farmland management rights as the sole collateral, enabling amortization, and without insurance and guarantee requirements. Results from the latent class model further suggest that guarantee takers strongly prefer lump-sum repayments and are more inclined to select insurance and guarantees relative to their counterparts, while guarantee averters strongly prefer to pay off loans with amortization and have positive propensities to purchase insurance. Moreover, female farmers with high education levels, entity identities, and loan experiences are more willing to pay off their loans at once and purchase insurance. Our findings provide insight into the roles of financial product attributes and borrowers’ characteristics in their demand for FMRMs. It may facilitate the design of optimal portfolios and adoption incentives for land mortgage products.

1. Introduction

Land financing policies have been increasingly recognized as some of the most critical measures used to address credit constraints in many developed and developing countries [1,2]. Developed countries, such as Germany and the U.S., have bolstered farmland mortgaging to support agriculture in financial markets and promote the development of rural finance [3]. This system has become relatively mature and popular in recent decades [4]. In the developing world, countries such as Thailand have also implemented land financing policies, e.g., land collateral to release the credit constraints [5]. However, credit constraints are particularly prevalent challenges for farmers in developing countries where farmers suffer from unstable incomes, insufficient credit collateral, high transaction costs, and underdeveloped financial markets [6,7]. In the transitioning economy of China, though it has issued several policies on land registration, land transactions, and mortgaging management rights for farmland (see Appendix A, Note 1) to relax the credit constraints for farmers, the effectiveness of these policies is still doubted due to the land ownership property and the insufficient property transaction market [8,9]. Among these, the farmland management right mortgage (FMRM) is the latest policy tool used with the aim to overcome insufficient credit collateral, thereby minimizing the high monitoring costs by reputation mechanisms. To date, the approved amounts and ratios of FMRMs are relatively low because of the low supply level. For instance, the study by Zhang et al. reported that only 6.27% of farmers’ demands for FMRMs have been met [10]; and about 61.47% of farmers have credits rationed when applying for FMRMs [11]. Therefore, whether farmers satisfy the requirements of FMRMs or they are willing to apply for FMRMs designed by financial institutions is worthy to investigate to successfully realize the effectiveness of FMRMs.

Since the FMRM, as a financial product, is characterized by a bundle of attributes, its importance among borrowers results in heterogeneous preferences for the attributes of FMRM. At present, most of the approved FMRM products in China have attributes that involve short-term high-interest rates, lump-up repayments, and low risks, such as the required use of agricultural insurance or a guarantor. However, these attributes are not all well-designed for farmers. From the borrowers’ perspective, a FMRM product with fewer transactional costs/requirements and low-interest rates that can be repaid monthly is more practical and effective for agricultural production. Farmers’ borrowing decisions are mainly determined by their production capacity and transaction costs [12]. Whereas, for the lenders, to minimize the cost and default probability, they would expect borrowers to take high-level interest rates and immediate pay-offs. Moreover, they would ask farmers to either provide guarantors to release the transaction risks due to the high information-asymmetric and small-scale operations and/or purchase the agriculture insurance to reduce the default probability arising from the agricultural operation risks. The discrepancy between supply and demand regarding FMRMs may increase the inefficient allocation of financial resources and lead to mortgage functional failure of the land endowment. To the best of our knowledge, no previous study has highlighted the gap between the supply of and demand for FMRMs that centers on the farmers’ preferred product attributes.

This study aimed to investigate farmers’ heterogeneous preferences for selecting FMRM product attributes, including interest rates, repayment types, agricultural insurance requirements, and guarantee requirements. Based on a discrete choice experiment (DCE) conducted in three provinces in China, we applied a random parameter logit (RPL) and a latent class model (LCM) to correct the bias that stems from the traditional logit model and accounts for the heterogeneity in consumer preferences.

The contributions of this study to the literature are three-fold. First, this study is the first to use in-the-field choice experiments to examine farmers’ heterogeneous FMRM attribute preferences and their willingness to pay for FMRM attributes in China. Second, we considered both the main and interaction effects among the attributes, revealing the main and simultaneous effects of FMRM attributes on rural households’ financing decisions. Third, we further investigated the heterogeneity in farmers’ preferences across individual and household characteristics, improving the present understanding of how farmers’ resource endowments determine their nominal demand preferences and financing behaviors. Our recommendations may assist policymakers in land reform and financial institutions in designing FMRM products and service strategies, thus improving farmers’ perceptions and establishing trust between borrowers and lenders.

The remainder of this paper is organized as follows. The following section reviews the evolution of farmland management rights and mortgages in China and presents the current state of FMRMs and related trends. We introduce the econometric framework in Section 3 and present the empirical results in Section 4. In Section 5, we present our conclusions and discuss our main findings.

2. Land Institutional and Background

2.1. The Evolution of Farmland Management Rights and Mortgages

Since the opening-up reform in the late 1970s, China’s rural land system has undergone a breakthrough transformation. China’s land system functions in accordance with three types of rights: ownership, contract, and management rights. The collective ownership of farmland is its fundamental and permanent institution. In 1978, the so-called “Household Responsibility System” (HRS) separated farmland contractual management rights from ownership rights. The HRS has contributed enormously to China’s agricultural development [13]. To further support land reforms, China has promoted farmland financing reforms since the 1990s. These reforms can be divided into two main stages: the exploratory stage (1988–2014) and the pilot trial stage (2015–present).

The exploratory stage started with the 1988 establishment of “land banks” in Meitan County, Guizhou. In these “land banks”, farmers could lend their contractual farmland management rights to banks, and the counterparty could borrow the land from the banks. Due to deficiencies in the “land banks” system and conflicts of interest among the central government, local government, and financial regulator, this reform was terminated after ten years. In the following period (from 2008 to 2014), a series of provisions and institutions were issued by different departments and ministries to accelerate land rentals and increase farm scales. However, the scale of land rentals was still small. Of these regulations, the implementation of land rights registration and the “Three Rights Separation” reform in 2013 were the most important because they linked farmland management rights to longer-term credit [14] and further promoted the exploration of FMRM programs.

The pilot trial stage started with the issuing of a document in 2015. It stipulated that farmers could use farmland management rights as collateral to access FMRMs in 232 pilot areas for two years (see Appendix A, Note 2). At the end of 2017, it was extended for one additional year. By 2019, the amendment to the rural land contract law was implemented, which advocated for the use of management rights to contracted farmland and leases as collateral to access loans from financial institutions. It was a milestone in China’s land reform and the FMRM businesses, their productivity, and scale developed rapidly since then.

2.2. The Current State of FMRMs

Following the implementation of FMRMs, different modes have been formed based on sharing the risks, including the typical “Direct Mortgage”, “Mortgage + Insurance”, “Mortgage + other Guarantee”, and “Mortgage + other Guarantee + Insurance” modes. In the final mode, farmland management rights are used as the primary collateral. By using the fundamental “Direct Mortgage” mode, many financial institutions have increased the collateral requirements to secure loans, such as agricultural insurance and other guarantees, to avoid the default risk. In this regard, insurance can be used as a form of effective collateral and to release operational and market risks [15]. Other guarantees also function as adequate collateral to reduce the default probability arising from information asymmetry. These guarantees mainly consist of acquaintance, joint, and property guarantees. These requirements are optional, but financial institutions will consider them as the essential factors to decide which farmers should be approved for a loan and its quantity. Meanwhile, the interest rate varies with these requirements.

The existing literature has mainly focused on the impact of FMRM supply and farmers’ demands for FMRMs. However, little is known about farmers’ preferences for FMRM attributes. For instance, lots of evidence suggests that the FMRM supply helps improve the accessibility of loans [2], the flow of farmland elements, investment, agriculture productivity, and rural economic growth [14,16]. In addition, some studies have indicated that farmers have huge potential demands for FMRMs [10] and many have applied for them. In fact, farmers’ nominal demands for FMRMs are far greater than the supply provided by financial institutions [10]. This gap between supply and demand may arise from asymmetric information between farmers and suppliers regarding product-specific attributes. Regardless, the land financing policy in China still faces barriers from land law, an underdeveloped market, and an inefficient risk management system due to the short implementation period. That could also lead to land-use deficiencies, low assignability, social conflicts, and land disputes, bringing high transaction risks to the lenders and affecting the supply of and demand for FMRMs.

3. Econometric and Framework

3.1. Theoretical Framework

The theoretical framework of our study is rooted in Lancaster’s [17] consumer theory and random utility theory [18]. According to the consumer theory, consumer preference is the choice of the bundled characteristics of goods. In our context, the good is a FMRM product with a collection of attributes, such as cost (interest rate), loan payment flexibility, and collateral requirements (agricultural insurance or guarantee). To better understand consumer preferences and the implicit prices of different attributes, it is appropriate to take consumer demand decisions as the components of a utility maximization problem under budget constraints [18]. Following Hanemann [19], consumer decisions can be separated into discrete and continuous choices.

A choice experiment (CE) is one practical approach used to closely simulate a real-world purchasing decision in which a consumer selects a product from a set of selections [20]. One distinguishing merit of the CE method is that individuals’ preferences for attributes of a product can be captured and the trade-off among these attributes and levels can be obtained when individuals rank the importance of different attributes [21]. Moreover, compared to contingent valuation, a CE overcomes the limitations of the one-dimensional assessment of valuation [22]. Furthermore, the evidence shows no statistically significant differences between the results obtained from choice experiment data (stated preference) and actual data (revealed preference) [23].

The utility consists of an observable certainty that depends on the attributes of an alternative and unobservable randomness. The choice experiment assumes that consumer obtains the utility [] from selecting the alternative from a finite set of alternatives in the choice set in situation . The utility consists of a deterministic segment [] and a stochastic segment []. Following Ortega et al. [20] and Davis et al. [24], the utility of alternative can be constructed as follows:

Consumer will select alternative if . The probability of the consumer selecting alternative is given as follows:

3.2. Econometric Strategies

Since consumers and their perceptions of multiple goods are usually heterogeneous, we employed the RPL and LCM to correct the bias that stems from using the traditional logit model and account for differences in consumer preferences (see [20]). Unlike the traditional logit model, the RPL is highly flexible. It can approximate any random utility model and relax the assumptions of consumer preference homogeneity. This homogeneity is independent of irrelevant alternatives (IIA) [25]. To capture the heterogeneity among respondents, we applied the LCM because it overcomes the disadvantage of arbitrary demarcation when using automatically estimated coefficients [17]. It is a relatively objective tool used to analyze inelastic product substitution and predict markets. Using LCMs to analyze random preference differences has become mainstream in the study of population segmentation [26].

In the RPL, the observable certainty of utility [] in the random utility model can be specified as

where is a vector of the consumer preference parameters and is a vector of the attributes for the th alternative. Following Train [27], the probability that consumer chooses alternative from a finite set of alternatives contained in a choice set in situation is given as follows:

If the heterogeneity in consumer preferences occurs discretely, the LCM is employed, which can sort individuals into latent classes. Each class includes homogeneous consumers [28]. is discrete in the LCM. The probability that consumer selects option in a given choice set in situation , unconditional on the class, is represented by

where is the parameter vector of class . is the probability that consumer falls into class and can be represented as follows:

where is a set of observable characteristics that affect the class membership for the th consumer. is the parameter vector for consumers in class .

The estimated parameters in both the RPL and LCM provide little economic information, given the non-cardinal nature of utility. Instead, we used the estimated parameters to measure the willingness to pay (WTP), which is calculated as the change in price to keep the same utility level after an attribute change. The WTP for the th attribute can be written as follows:

where is the estimated parameter of the th attribute and is the estimated coefficient of the price in the present context.

Since the attributes are qualitative variables and the price is the expense of the product, the negative ratio in Equation (7) is the tradeoff between the cost and gain of each attribute. Following Lusk et al. [29], the WTP calculation is multiplied by two when using effects coding. The WTP may be undefined or not amenable to interpretation because it is the ratio of two distributions. In our estimation of the RPL, we fixed the interest rate coefficient (i.e., it was homogeneous across observations) and typically allowed the coefficients of the other attributes to vary, a common assumption in many RPL applications [30]. Using a fixed interest rate coefficient allows the distribution of the WTP to be the same as the distribution of the random attribute coefficient, with the mean and variance scaled in accordance with the fixed interest rate coefficient to provide a meaningful interpretation [21].

3.3. Design of DCE and Data Description

3.3.1. Attributes

- Interest rate. It is the price of a FMRM and the critical determinant of farmers’ mortgage decisions. In China, the interest rate varies between financial institutions and loans. The lending interest rate is an essential factor for lending decisions, and it consists of two parts: the benchmark interest rate and the floating interest rate (see Appendix A, Note 3). Our DCE used interest rates of 5% and 8%, respectively.

- Repayment. Repayment types include lump sum and amortization. During a lump-sum repayment, the borrower pays the loan and accrued interest in a single payment at or before the end of the loan term. In the amortization process, the borrower repays the loan in equal payments with decreasing interest every month during the loan period.

- Insurance. A FMRM is a loan product issued according to the expected income of farmland fixtures and operating life. Due to the multiple and high risks in agriculture, in theory, agricultural insurance is recognized as an essential tool that disperses agricultural operation risk. It is also adequate collateral to lower the credit risk [15]. To reduce the default probability, financial institutions consider agricultural insurance to be an essential factor for approving a FMRM. While agricultural insurance can also increase farmers’ costs, particularly the transaction costs of FMRMs.

- Guarantee. The lack of adequate collateral is a common issue in rural China. Although farmland management rights have been used as collateral since 2009, the underdeveloped farmland transaction market prevents these rights from being fully exploited. Hence, whether borrowers have other guarantees is essential for financial institutions to approve FMRMs. In practice, it is difficult for farmers to find other guarantees. Table 1 presents the selected attributes and levels used in the DCE.

Given the attributes and levels in Table 1, a study with a full factorial experimental design would require the respondents to make (24)2 = 256 distinct choices, which would be tedious to do in the field. Hence, this study used a fractional factorial design. We employed the orthogonal to obtain 12 choice scenarios. Using a D-optional design, we estimated all primary and two-way interaction effects. Figure 1 presents one sample choice set.

3.3.2. Sampling and Data Collection

Following Shee et al. [15], the sample size required to assess the main effects depended on the number of choice tasks (), the number of alternatives (), and the number of analysis cells ():

In our context, each respondent needed to complete six choice tasks (), and each choice task presented alternatives (); equals the most significant number of levels for any attribute (). Thus, using Equation (8), we determined that the minimum sample size for this study was 56.

We collected the data used in this study with a questionnaire survey conducted with face-to-face interviews from 2019 to 2020 in the provinces of Ningxia, Chongqing, and Sichuan, China. We applied stratified sampling and used four stages to sample the respondents. First, we selected three provinces in western China. As mentioned previously, we designated 232 counties, referred to as districts, as pilot areas that allowed FMRMs. Of these pilots, about 10.77% were in Ningxia, Chongqing, and Sichuan. Second, we selected 12 districts in the three provinces by considering the implemented reforms to farmland property rights, geographical environment, and economic status. All these districts are in typical FMRM pilot areas. Third, we selected three to four representative towns with different levels of economic development from each district. Then, we selected three to four representative villages in each town based on the same principle. Fourth, we randomly selected 8 to 12 farmers in each village. In total, we surveyed 1900 rural households. After excluding observations with missing data or outliers, we obtained information from a total of 1815 farmers and used 32,670 combinations (1815 farmers × 3 choices × 6 cards) in our analysis.

Table 2 shows a summary of the respondents’ sociodemographic characteristics. Around 61% of the respondents were male with an average age of 55, and the majority had not attended high school (see Appendix A, Note 4). Over half thought that they had a middle or higher social status (see Appendix A, Note 5). A total of 20.7% were members of agribusiness entities, and 11.85% had FMRMs approved experience.

4. Results and Discussion

4.1. Heterogeneity in Farmers’ Preferences for Selecting FMRM Attributes

Table 3 presents the results of the RPL and LCM. The significance of the standard deviation (STDEV) coefficients of repayment, insurance, and guarantee reveals notable preference heterogeneity for all attributes, which justifies the use of RPL. All parameters have their expected signs.

As reported in column 1 in Table 3, first, the coefficient of the interest rate is less than one and negative, indicating that farmers are interest-rate sensitive and have rigid demands for FMRMs. It supports the previous studies that farmers have strong demands for FMRMs [15]. Second, farmers mostly preferred to repay the loan with amortization. This is consistent with the findings by Kong et al., i.e., farmers have a stronger preference for credit amortization over lump-sum payments [31]. In theory, amortization could alleviate financial stress because it offers relative flexibility and adaptability to the production cycle of agriculture. That is, it allows borrowers to have the scheduled repayments begin at a level lower than that of a comparable standard mortgage loan [32]. To most farmers, their agricultural income can be obtained at the end of the harvest seasons. It has clearly been effective in increasing access to agricultural investment for wealth-constrained farmers by shifting the burden of the loan to the later term [33]. Third, farmers preferred no insurance requirements when applying for FMRMs. The result is consistent with the findings by Liu and Zhong [34], i.e., farmers have a relatively low demand for agriculture insurance because of their little awareness of risk mitigation and low satisfaction from the agricultural insurance premium subsidies [35]. Fourth, farmers preferred no guarantee requirements when applying for FMRMs, as most of them do have difficulty in offering guarantees other than land. Additionally, regarding the interaction terms, this study noted that, unlike the monthly loan repayment takers, the lump-sum repayment takers preferred having no insurance and guarantee requirements. Moreover, the insurance takers preferred having no guarantee requirements, unlike the insurance averters. That is, insurance and guarantee requirements may significantly mitigate lump-sum repayment adoption. Likewise, guarantee requirements may significantly decrease the willingness of farmers to purchase insurance if the cost is higher than what these farmers can afford.

The preference heterogeneity found in the RPL created significant differences among the members of different classes in the LCM. As reported in columns 2 and 3 in Table 3, the probability that a randomly chosen respondent belongs to either the first or second class is 66.9% and 33.1%, respectively. In terms of absolute values, the second latent class in the LCM shows a relatively high guarantee coefficient value, indicating that a substantial proportion of farmers are guarantee takers. This class (33.1% of the population) represents a group of farmers who are willing to pay off their loans. Based on their FMRM preferences, we defined the farmers in this class as “guarantee takers” and those in the first class (66.9% of the population) as “guarantee averters”. Specifically, the guarantee takers strongly preferred lump-sum repayments and had a clear propensity to prefer insurance and guarantees relative to their counterparts. In contrast, the guarantee averters had relatively strong preferences to pay off the loans with amortization and positive propensities to purchase insurance. Farmers who know more about insurance and can pay for it may prefer this method, owing to the benefits of risk mitigation and enhanced credit. For instance, Mishra et al. [36] applied a randomized control trial in Ghana and found that insurance bundled loans were conducive to increasing the likelihood of receiving credit by 15%.

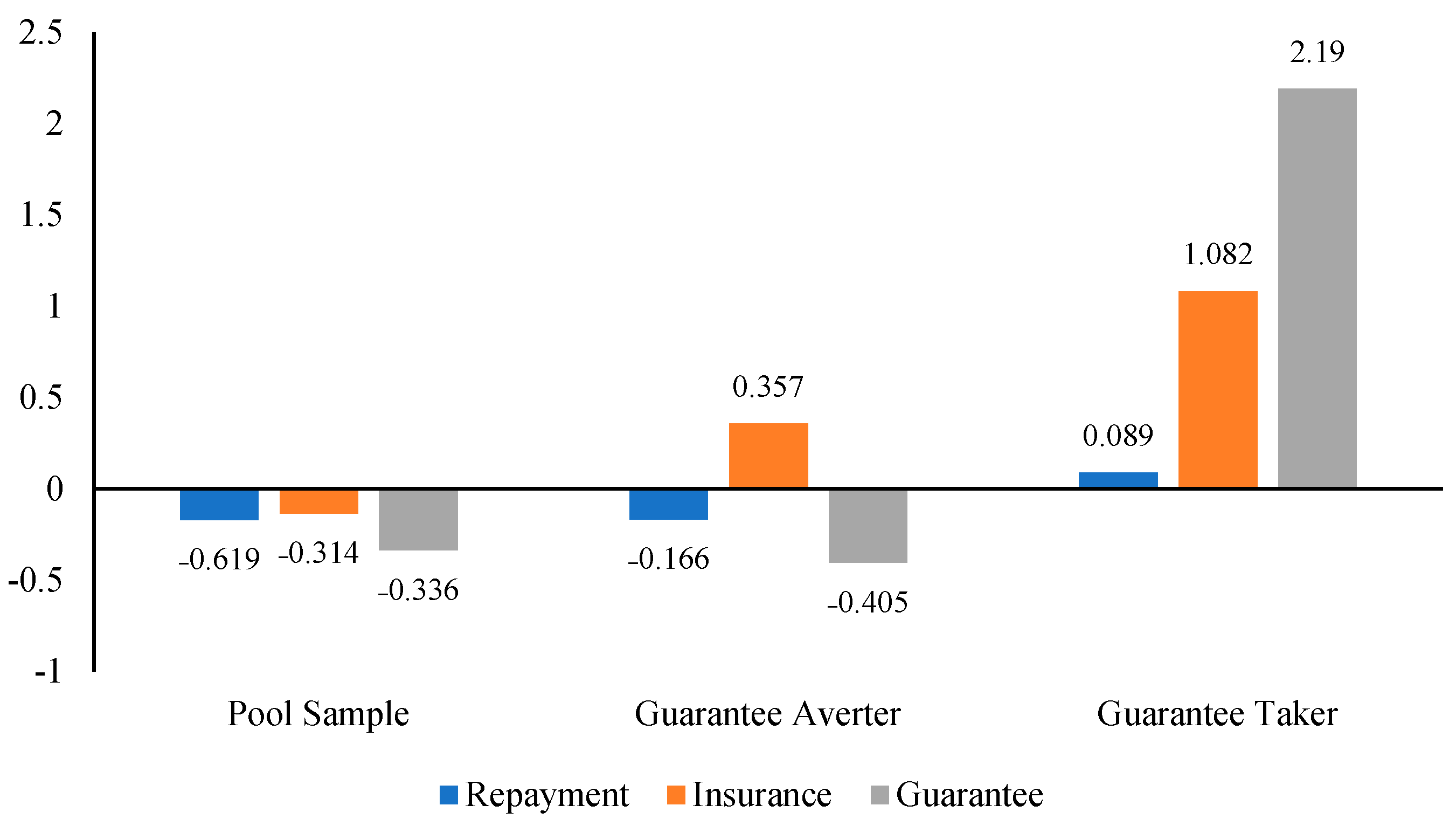

Figure 2 presents the estimated results of the mean WTP with 95% confidence intervals derived from the estimated RPL and LCM. For the sample pool, one farmer was willing to pay on average a 0.169% higher interest rate for a loan with monthly payments compared to a loan with a single payment. Moreover, they would pay on average 0.134% and 0.336% higher interest rates for loans without insurance and guarantee requirements, respectively. In other words, farmers prefer to pay for products that directly use farmland management rights as collateral, can be repaid using amortization, and lack insurance and guarantee requirements. Regarding the guarantee averters, they were willing to pay a 0.166% higher interest rate for loans with monthly payments than those with a single payment. In addition, they would accept a 0.357% higher interest rate for loans with insurance requirements and a 0.405% higher interest rate for those without guarantee requirements.

In contrast, the guarantee takers were willing to pay a 0.089% higher interest rate for loans that needed to be paid for at once rather than monthly. Likewise, they were willing to pay 1.082% and 2.190% higher interest rates for loans with insurance and guarantee requirements, respectively.

4.2. Heterogeneity in Farmers’ Preferences for Selecting FMRM Attributes by Farmers’ Characteristics

To further understand FMRM demand, we explored the heterogeneity in the farmers’ preferences for selecting FMRM attributes by considering their characteristics. Table 4 presents the estimated heterogeneity in the farmers’ preferences for selecting FMRM attributes across their characteristics.

Gender, education, agribusiness entity identity, loan experience, and social status all significantly affected the farmers’ preferences. The male farmers preferred monthly payments and were more likely to accept loans that had higher interest rates and no insurance and guarantee requirements than the female farmers. The farmers with higher education levels preferred loans that would be repaid in one payment and required insurance. While these farmers would accept higher interest rates, they avoided guarantee requirements. The entity farmers preferred loans that would be repaid in one payment with insurance and guarantee requirements, and they would accept higher interest rates. Similarly, the farmers with loan experiences preferred loans with insurance requirements that they could repay in one payment and would accept higher interest rates, but they also favored loans without guarantee requirements. Lastly, the farmers with higher social statuses showed significant preferences toward selecting loans with monthly payments and no insurance and guarantee requirements, and they would also accept higher interest rates. Additionally, female identity, low education, non-entity identity, non-experience, and low social status significantly reduced the probability of the lump-sum repayment takers accepting insurance requirements compared to the monthly loan takers. Moreover, these characteristics significantly reduced the probability that the insurance takers preferred no guarantee requirements compared to the insurance averters. Entity identity significantly increased the probability of the lump-sum repayment takers accepting the requirements for insurance at the 5% level.

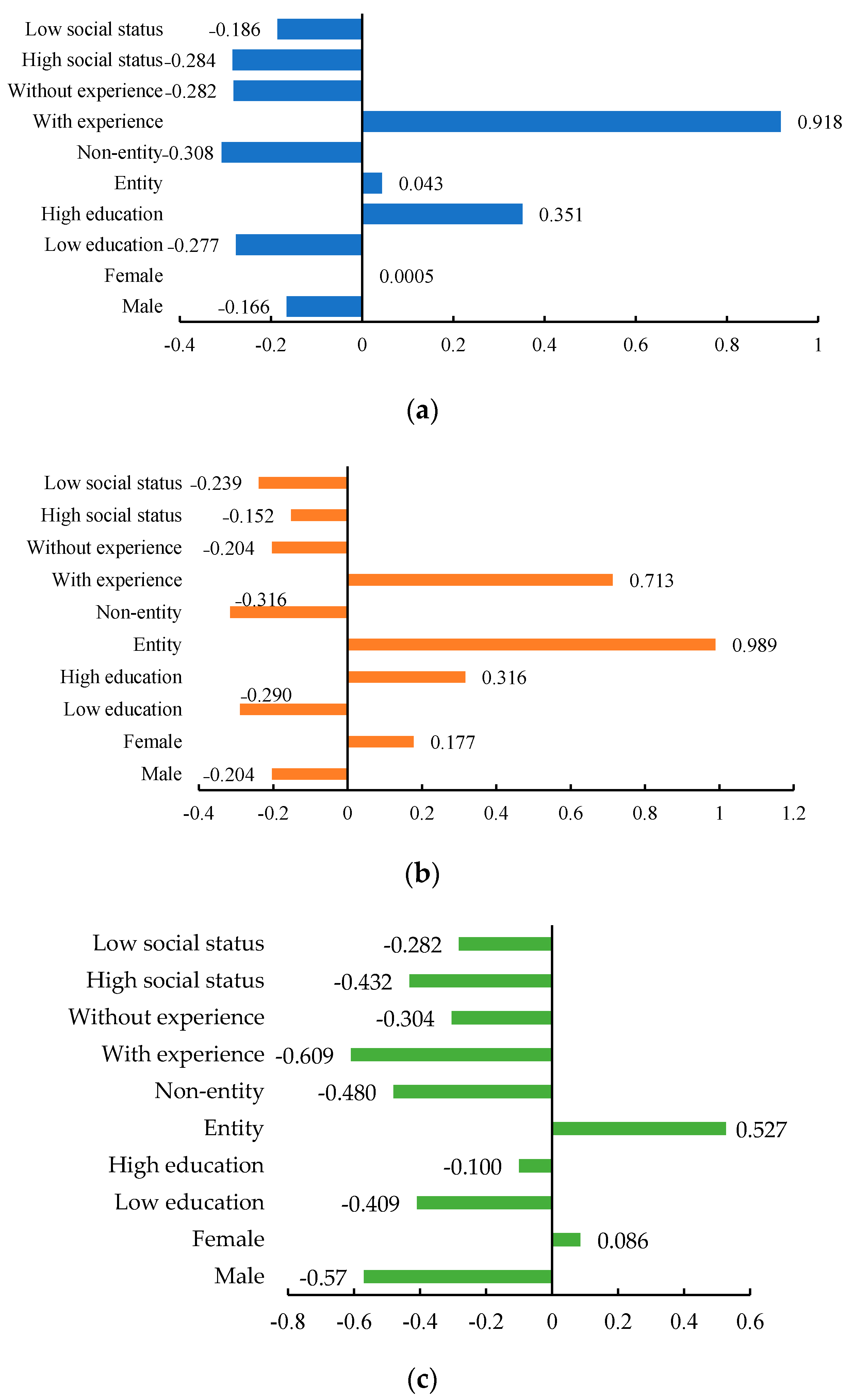

Figure 3a–c reports the estimated results of the mean WTP of different attributes across gender, education, agribusiness entity, loan experience, and social status, as well as 95% confidence intervals derived from the estimated RPL. The heterogeneities in farmers’ preferences for selecting FMRM attributes are apparently across their characteristics, especially for gender, agribusiness entity, and loan experience. First, it is indicated that the female farmers with high education levels, entity identities, and loan experiences were more willing to pay off their loans at once. In precisely, they were willing to pay a 0.0005%, 0.351%, 0.043%, and 0.918% higher interest rate for a one-payment loan than for monthly-payment loans, respectively. Similarly, they were also willing to pay a 0.177%, 0.316%, 0.989%, and 0.713% higher interest rate for loans with insurance requirements, respectively. In addition, only the female farmers with entity identities were more willing to pay a 0.086% and 0.527% higher interest rate for loans with guarantee requirements, respectively. Second, the characteristics of gender, agribusiness entity, and loan experience are sensitive to the demand of FMRM. A possible explanation could be that gender determines financial decision-making rights; different identities and loan experiences are important factors that affect loan demands and financing behaviors [12,21,31].

4.3. Limitations and Future Study

Since the mainstream supply of FMRM products are designed in the short-term in the prevailing market, we did not include the term of the loan attribute in the FMRM product, i.e., a short-term product (less than 1 year) vs. medium- (over 1–3 years,) or long-term products (over 3 years), individuals’ preferences may vary largely when selecting them. In future research, if the FMRM product is to be scaled, this attribute can be included when the medium- or long-term FMRM products are launched. Another consideration is the inclusion of the FMRM supplier in the attribute. Different suppliers (e.g., financial institutions) would provide distinct products and services that affect individuals’ decision-making.

5. Conclusions and Policy Implications

Farmland Management Right Mortgages (FMRMs) is an important and emerging land financing tool used to alleviate credit constraints; it has drawn much attention from farmers, financial institutions, and policymakers in China. The impropriate-designed FMRM products and their mismatched attributes may discourage farmers’ initiatives to apply for them. This study examined the demand for FMRMs to better understand farmers’ heterogeneous preferences in selecting FMRM attributes and their WTPs for these attributes, using an in-the-field choice experiment based on data collected from 1815 farm households in 2019 and 2020, in China.

One of the main findings of this study is that farmers are interest-rate sensitive with rigid demands for FMRMs. Moreover, farmers have the highest WTP in using farmland management rights as sole collateral and they prefer to paying off in amortization but without insurance or guarantee. Thus, policies designed to increase the supply of FMRMs may consider establishing a comprehensive risk system to help financial institutions to release risk so that farmers could be approved for more FMRMs with fewer requirements. As noted, initiatives to increase the credit supply will be more effective if the aggregated credit demand is huge [37].

Another important finding is that farmers have the highest WTP for products that include amortization (without guarantee requirements). After considering the class differentiation, the “guarantee averters” are more willing to pay off loans with amortization and insurance requirements, while “guarantee takers” are more willing to adopt loans with lump-sum payments and guarantee requirements. These results suggest that lenders may consider offering a portfolio of FRMR products with different attributes to maximize the potential pool of borrowers. For example, in terms of repayment, our results indicate that farmers value flexibility and may prefer a series of smaller loan repayments rather than a single lump-sum transfer [38]. Meanwhile, policies that aim to increase the supply of FMRMs are suggested to establish and improve local government guarantee systems to help farmers obtain access to loans by “Direct Mortgage” modes.

One last important finding is that gender, agribusiness entity, and loan experience largely affect farmers’ preferences for selecting FMRM attributes. Thus, household characteristics are nonnegligible in designing land financing products, such as FMRMs, given that they play an essential role in determining a rural household’s nominal demands and financing behaviors. In addition, policies that seek to increase the supply of FMRMs are suggested to prioritize farmers’ credit demands in the context of an emerging class of commercial farmers.

This study’s exploration of farmland financing implementation in China provides an example for other developing countries where farmland financing policies are expected to alleviate credit constraints. Notably, the design of FMRM attributes may have important implications in countries, e.g., Ethiopia, where only usufruct rights are given to landholders [39]. Lastly, a better understanding of farmers’ preferences and designing appropriate products that satisfy farmers’ needs could make credit more accessible and thus reduce the risk of moral hazards.

Author Contributions

Conceptualization, Y.P. and Y.J.; methodology, Y.H.; software, Y.H.; validation, Y.P., Y.J. and Y.H.; formal analysis, Y.H.; investigation, Y.P. and Y.J.; resources, Y.P.; data curation, Y.H.; writing—original draft preparation, Y.P.; writing—review and editing, Y.J. and Y.H.; visualization, Y.H.; supervision, Y.H.; project administration, Y.P.; funding acquisition, Y.P. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the National Nature Science Foundation of China, grant number 7190314, the National Social Science Fund of China, grant number 20AJY011, the China Postdoctoral Science Foundation, grant number 2019M653834XB, and the Agricultural Science and Technology Innovation Program, grant number 10-IAED-04-2022.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the first authors upon reasonable request.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Note 1: Since 2013, rural land tenure in China has been divided into three rights: ownership, contract, and management rights. Ownership rights are possessed by the state and collective. Contract rights refer to the rights to contract from the state and collective, which is the most effective guarantee for households without ownership. Furthermore, these rights are possessed by the villagers affiliated with the same collectives and cannot be transacted directly in the market. Management rights refer to the operation rights to use and manage farmland, and they belong to the operator. Only management rights for contracted farmland can be used as collateral to access loans from the formal institution

Note 2: http://www.moa.gov.cn/govpublic/zcggs/201908/t20190812_6322482.htm (accessed on 5 November 2021)

Note 3: The benchmark interest rate is determined by the Central People’s Bank of China, whereas the floating rate is determined by local banks.

Note 4: In the sample, 838 respondents had primary school experience, 562 had middle school experience, 285 had high school experience, and only 127 had college or university experience.

Note 5: 74 respondents reported low social status, 279 reported relatively low social status, 930 reported middle social status, 408 respondents reported relatively high social status, and 109 reported high social status.

References

- Ma, X.; Heerink, N.; Feng, S.; Shi, X. Farmland tenure in China: Comparing legal, actual and perceived security. Land Use Policy 2015, 42, 293–306. [Google Scholar] [CrossRef]

- Gu, X.; Zhang, Y.; Qian, X. The suspension of borrowing: An implicit penalty for loan default under imperfect information. Appl. Econ. 2016, 48, 5882–5896. [Google Scholar] [CrossRef]

- Johnson, J. Rural economic development in the United States: An evaluation of the US department of agriculture’s business and industry guaranteed loan program. Econ. Dev. Q. 2009, 2, 229–241. [Google Scholar] [CrossRef]

- Aditya, R.K.; Omobolaji, O. Rural finance, capital constrained small farms, and financial performance: Findings from a primary survey. J. Agric. Appl. Econ. 2020, 52, 288–307. [Google Scholar]

- Feder, G.; Onchan, T.; Raparla, T. Collateral, guaranties and rural credit in developing countries: Evidence from Asia. Agric. Econ. 1988, 2, 231–245. [Google Scholar] [CrossRef] [Green Version]

- Li, C.; Lin, L.; Gan, C.E.C. China credit constraints and rural households’ consumption expenditure. Financ. Res. Lett. 2016, 19, 158–164. [Google Scholar] [CrossRef]

- Peng, Y.; Ren, Y.; Li, H. Do credit constraints affect household’s economic vulnerability? Empirical evidence from rural China. J. Int. Agric. 2021, 20, 2552–2568. [Google Scholar] [CrossRef]

- Besley, T.; Ghatak, M. Creating Collateral: The de Soto Effect and the Political Economy of Legal Reform; Working Paper; London School of Economics: London, UK, 2008. [Google Scholar]

- Luo, X.; Ma, J. Comparison of montage effect of the right to use farmland under different kind of land transfer modes. Issues Agric. Econ. 2017, 2, 22–32. [Google Scholar]

- Zhang, H.; Luo, J.; Cheng, M.; Duan, P. How does rural household differentiation affect the availability of farmland management right mortgages in China? Emerg. Mark. Financ. Trade 2019, 56, 2509–2528. [Google Scholar] [CrossRef]

- Gu, Q.; Lin, L. Can farmland management rights mortgages relieve the credit rationing of farmers? Econ. Rev. 2019, 5, 63–76. [Google Scholar]

- Tang, S.; Guo, S. Formal and informal credit markets and rural credit demand in China. In Proceedings of the 2017 4th International Conference on Industrial Economics System and Industrial Security Engineering, Kyoto, Japan, 24–27 July 2017. [Google Scholar]

- Lin, J.Y. The household responsibility system in China’s agricultural reform: A theoretical and empirical study. Econ. Dev. Cult. Chang. 1988, 36, S199–S224. [Google Scholar] [CrossRef]

- Peng, Y.; Kong, R. An analysis of China’s reforms on mortgaging and transacting rural land use rights and entrepreneurial activity. Agric. Financ. Rev. 2020, 80, 377–400. [Google Scholar] [CrossRef]

- Shee, A.; Turvey, C.G. Collateral-free lending with risk-contingent credit for agricultural development: Indemnifying loans against pulse crop price risk in India. Agric. Econ. 2012, 43, 561–574. [Google Scholar] [CrossRef]

- Yang, X.; Luo, J.; Yan, W. Heterogeneous effects of rural land property mortgage loan program on income: Evidence from the western China. China Agric. Econ. Rev. 2018, 10, 695–711. [Google Scholar] [CrossRef]

- Lancaster, K.J. A new approach to consumer theory. J. Polit. Econ. 1966, 74, 132–157. [Google Scholar] [CrossRef]

- McFadden, D. Conditional Logit Analysis of Qualitative Choice Behavior in P. Zarembka; New York Academic Press: New York, NY, USA, 1974; pp. 123–128. [Google Scholar] [CrossRef]

- Hanemann, W.M. Discrete/continuous models of consumer demand. Econom. J. Econom. Soc. 1984, 52, 541–561. [Google Scholar] [CrossRef]

- Ortega, D.; Wang, H.H.; Wu, L.; Olynk, N.J. Modeling heterogeneity in consumer preference for select food safety attributes in China. Food Policy 2011, 36, 318–324. [Google Scholar] [CrossRef] [Green Version]

- Kanninen, B.J. Valuing Environmental Amenities Using Stated Choice Studies: A Common Sense Approach to Theory and Practice; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2007; Volume 8, Available online: https://link.springer.com/book/10.1007/1-4020-5313-4?noAccess=true (accessed on 1 July 2020).

- Shee, A.; Turvey, C.G.; Marr, A. Heterogeneous demand and supply for an insurance-linked credit product in Kenya: A stated choice experiment approach. J. Agric. Econ. 2020, 72, 244–267. [Google Scholar] [CrossRef]

- Lusk, J.L.; Schroeder, T.C. Are choice experiments incentive compatible? A test with quality differentiated beef steaks. Am. J. Agric. Econ. 2004, 86, 467–482. [Google Scholar] [CrossRef] [Green Version]

- Davis, K.J.; Burton, M.; Kragt, M.E. Scale heterogeneity and its implications for discrete choice analysis. Land Econ. 2019, 95, 353–368. [Google Scholar] [CrossRef]

- McFadden, D.; Train, K. Mixed MNL models for discrete response. J. Appl. Econ. 2000, 15, 447–470. [Google Scholar] [CrossRef]

- Teichert, T.; Shehu, E.; Wartbugr, I.V. Customer segmentation revisited: The case of the airline industry. Transport. Res. A Pol. 2008, 42, 227–242. [Google Scholar] [CrossRef] [Green Version]

- Train, K.E. Discrete Choice Methods with Simulation; Cambridge Books; Cambridge University Press: Cambridge, UK, 2003; pp. 109–112. [Google Scholar]

- Boxall, P.C.; Adomowicz, W.L. Understanding heterogeneous preference in random utility models: A latent class approach. Environ. Res. Econ. 2002, 23, 421–446. [Google Scholar] [CrossRef]

- Lusk, J.L.; Roosen, J.; Fox, J.A. Demand for beef from cattle administered growth hormones or fed genetically modified corn: A comparison of consumers in France, Germany, the United Kingdom, and the United States. Am. J. Agric. Econ. 2003, 85, 16–29. [Google Scholar] [CrossRef] [Green Version]

- Ward, P.S.; Ortega, D.; Spielman, D.J.; Singh, V. Heterogeneous demand for drought-tolerant rice: Evidence from Bihar, India. World Dev. 2014, 64, 125–139. [Google Scholar] [CrossRef]

- Kong, R.; Peng, Y.; Meng, N.; Fu, H.; Zhou, L.; Zhang, Y.; Turvey, C. Heterogeneous choice in the demand for agriculture credit in China: Results from an in-the-field choice experiment. China Agric. Econ. Rev. 2021, 13, 456–474. [Google Scholar] [CrossRef]

- Asare, E.L.; Whitehead, C. Formal mortgage markets in Ghana: Nature and implications. RICS Res. Pap. Ser. 2006, 6, 1–30. [Google Scholar]

- Geltner, D.; Miller, N.G.; Clayton, J.; Eichholtz, P. Commercial Real Estate Analysis and Investments; South-Western: Cincinnati, OH, USA, 2001; p. 642. [Google Scholar]

- Liu, Y.; Zhong, F. Risk management VS income support: A research about the policy target selection of police agricultural insurance in China. Issues Agric. Econ. 2019, 4, 131–139. [Google Scholar]

- Zheng, H.; Zhang, Z. Analyzing characteristics and implications of the mortgage default of agricultural land management rights in recent China based on 724 court decisions. Land 2021, 10, 729. [Google Scholar] [CrossRef]

- Mishra, K.; Gallenstein, R.A.; Miranda, M.J.; Sam, A.G.; Toledo, P.; Mulangu, F. Insured loans and credit access: Evidence from a randomized field experiment in Northern Ghana. Am. J. Agric. Econ. 2020, 103, 923–943. [Google Scholar] [CrossRef]

- Ma, W.; Xu, X. Identification of credit suppression and policy implications: Evidence from thousand village survey. Financ. Res. 2018, 3, 19–36. [Google Scholar]

- Jia, X.; Heidhues, F.; Zeller, M. Credit rationing of rural households in China. Agric. Financ. Rev. 2010, 70, 37–54. [Google Scholar] [CrossRef]

- Crewett, W.; Korf, B. Ethiopia: Reforming Land Tenure. Rev. Afr. Policy Econ. 2008, 35, 203–220. [Google Scholar] [CrossRef]

Figure 1.

Sample choice set.

Figure 2.

Farmers’ willingness-to-pay, mean [95% confidence interval].

Figure 3.

(a) The WTP of repayment across gender, education, agribusiness entity, loan experience, social status, and mean [95% confidence interval]. (b) The WTP of insurance across gender, education, agribusiness entity, loan experience, social status, and mean [95% confidence interval]. (c) The WTP of guarantee across gender, education, agribusiness entity, loan experience, social status, and mean [95% confidence interval].

Figure 3.

(a) The WTP of repayment across gender, education, agribusiness entity, loan experience, social status, and mean [95% confidence interval]. (b) The WTP of insurance across gender, education, agribusiness entity, loan experience, social status, and mean [95% confidence interval]. (c) The WTP of guarantee across gender, education, agribusiness entity, loan experience, social status, and mean [95% confidence interval].

{kind=link}

{kind=link}

{kind=link}

Table 1.

Attributes and levels used in the direct choice experiment.

| Attributes | Levels and Description |

|---|---|

| Interest rate | 5% and 8% |

| Repayment | 1 = Lump sum, 0 = Amortization |

| Insurance | 1 = Agricultural insurance required, 0 = No agricultural insurance required |

| Guarantee | 1 = Guarantee required, 0 = No guarantee required |

Table 2.

Sociodemographic statistics.

| Variables | Definition | Mean | S.D. |

|---|---|---|---|

| Age | The respondent’s age (year) | 54.5 | 13.0 |

| Gender | Gender of the respondent: 1 = male, 0 = female | 0.607 | 0.489 |

| Education | 1 = primary school, 2 = middle school, 3 = high school, 4 = college or university | 1.84 | 0.962 |

| Social status | Self-evaluation of the respondent’s class identification: 1 = low, 2 = relatively low, 3 = middle, 4 = relatively high, 5 = high | 3.11 | 0.881 |

| Agribusiness entity | 1 = yes, 0 = no | 0.207 | 0.405 |

| Loan experience a | FMRM experience: 1 = approved, 0 = other | 0.119 | 0.323 |

| Number of respondents | 1815 | ||

| Number of observations | 32,670 | ||

a The demand for FMRMs was approved either partly or entirely in the last three years.

Table 3.

The estimations of the RPL and LCM.

| Variables | RPL | LCM | |

|---|---|---|---|

| Class 1 (Guarantee Averters) | Class 2 (Guarantee Takers) | ||

| (1) | (2) | (3) | |

| Interest rate | −0.658 *** (0.02) | −0.581 *** (0.02) | −0.471 *** (0.08) |

| Repayment | −0.111 (0.12) | −0.097 (0.10) | 0.042 (0.63) |

| Insurance | −0.088 (0.12) | 0.207 ** (0.10) | 0.510 (0.63) |

| Guarantee | −0.221 ** (0.11) | −0.235 *** (0.09) | 1.032 * (0.62) |

| Repayment Insurance | −0.246 ** (0.12) | 0.154 (0.11) | 0.506 (0.62) |

| Repayment Guarantee | −0.889 *** (0.11) | −0.259 *** (0.10) | −0.657 (0.61) |

| Insurance Guarantee | −0.835 *** (0.12) | −0.157 (0.10) | −0.357 (0.52) |

| STDEV (Repayment) | 2.689 *** (0.09) | ||

| STDEV (Insurance) | 2.406 *** (0.09) | ||

| STDEV (Guarantee) | 2.053 *** (0.08) | ||

| Opt-out | −4.187 *** (0.18) | −5.523 *** (0.18) | 1.969 ** (0.79) |

| Class Prob. | N. A | 0.669 | 0.331 |

| AIC | 18,337.990 | 14,815.893 | |

| BIC | 18,430.321 | 14,958.585 | |

| Chi2 | 3672.196 | ||

Standard errors in parentheses; *** p < 0.01, ** p < 0.05, * p < 0.1.

Table 4.

Estimated RPL results across gender, education, agribusiness entity, loan experience, and social status.

Table 4.

Estimated RPL results across gender, education, agribusiness entity, loan experience, and social status.

| Variables | Gender | Education | Agribusiness Entity | Loan Experience | Social Status | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Male | Female | Low Education | High Education | Entity | Non-Entity | With Experience | Without Experience | High Social Status | Low Social Status | |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | |

| Interest rate | −0.637 *** (0.02) | −0.694 *** (0.03) | −0.654 *** (0.02) | −0.669 *** (0.04) | −0.507 *** (0.05) | −0.702 *** (0.02) | −0.604 *** (0.05) | −0.667 *** (0.02) | −0.646 *** (0.02) | −0.714 *** (0.04) |

| Repayment | −0.106 (0.15) | 0.000 (0.22) | −0.181 (0.15) | 0.235 (0.20) | 0.022 (0.23) | −0.216 (0.15) | 0.554 ** (0.28) | −0.188 (0.13) | −0.184 (0.14) | −0.133 (0.26) |

| Insurance | −0.130 (0.14) | 0.123 (0.21) | −0.190 (0.14) | 0.211 (0.20) | 0.501 ** (0.23) | −0.222 (0.14) | 0.430 (0.27) | −0.136 (0.13) | −0.098 (0.13) | −0.171 (0.25) |

| Guarantee | −0.363 *** (0.13) | 0.060 (0.19) | −0.268 ** (0.13) | −0.067 (0.18) | 0.267 (0.19) | −0.337 ** (0.13) | −0.368 (0.23) | −0.203 * (0.12) | −0.279 ** (0.12) | −0.201 (0.23) |

| Repayment × Insurance | 0.035 (0.14) | −0.785 *** (0.20) | −0.418 *** (0.14) | 0.132 (0.21) | 0.660 ** (0.27) | −0.427 *** (0.14) | 0.362 (0.29) | −0.378 *** (0.13) | 0.016 (0.13) | −0.960 *** (0.24) |

| Repayment × Guarantee | −0.858 *** (0.14) | −1.071 *** (0.20) | −0.869 *** (0.14) | −0.993 *** (0.20) | −1.564 *** (0.24) | −0.786 *** (0.14) | −0.528 ** (0.27) | −0.965 *** (0.13) | −0.752 *** (0.13) | −1.163 *** (0.24) |

| Insurance × Guarantee | −0.604 *** (0.15) | −1.207 *** (0.22) | −1.000 *** (0.15) | −0.193 (0.21) | −0.889 *** (0.26) | −0.658 *** (0.15) | −0.536 * (0.28) | −0.848 *** (0.13) | −0.702 *** (0.14) | −1.207 *** (0.26) |

| STDEV (Repayment) | 2.581 *** (0.11) | 2.881 *** (0.16) | 2.917 *** (0.12) | 1.824 *** (0.14) | 1.988 *** (0.19) | 2.885 *** (0.11) | 1.805 *** (0.19) | 2.733 *** (0.10) | 2.540 *** (0.10) | 3.158 *** (0.21) |

| STDEV (Insurance) | 2.322 *** (0.11) | 2.517 *** (0.17) | 2.505 *** (0.11) | 1.681 *** (0.14) | 2.545 *** (0.20) | 2.281 *** (0.11) | 1.405 *** (0.18) | 2.446 *** (0.10) | 2.169*** (0.10) | 3.115 *** (0.23) |

| STDEV (Guarantee) | 1.875 *** (0.10) | 2.260 *** (0.14) | 2.194 *** (0.10) | 1.484 *** (0.13) | 1.918 *** (0.17) | 2.130 *** (0.09) | 1.065 *** (0.17) | 2.188 *** (0.09) | 1.883 *** (0.09) | 2.548 *** (0.19) |

| Opt-out | −4.231 *** (0.22) | −4.027 *** (0.30) | −3.941 *** (0.21) | −4.976 *** (0.34) | −3.223 *** (0.38) | −4.439 *** (0.21) | −4.971 *** (0.46) | −4.090 *** (0.19) | −4.435 *** (0.20) | −3.843 *** (0.37) |

| AIC | 11,239.467 | 7058.133 | 13,815.745 | 4307.504 | 3962.400 | 14,251.805 | 2121.399 | 16,003.270 | 13,196.852 | 5000.918 |

| BIC | 11,326.294 | 7140.192 | 13,905.218 | 4383.609 | 4037.420 | 14,341.581 | 2190.270 | 16,094.212 | 13,285.373 | 5079.735 |

| Chi2 | 2104.434 | 1547.860 | 3083.179 | 439.877 | 587.127 | 3112.247 | 169.650 | 3321.575 | 2354.054 | 1290.104 |

Standard errors in parentheses, *** p < 0.01, ** p < 0.05, * p < 0.1.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Peng, Y.; Jiang, Y.; Hong, Y. Heterogeneous Preferences for Selecting Attributes of Farmland Management Right Mortgages in Western China: A Demand Perspective. Land 2022, 11, 1157. https://doi.org/10.3390/land11081157

AMA Style

Peng Y, Jiang Y, Hong Y. Heterogeneous Preferences for Selecting Attributes of Farmland Management Right Mortgages in Western China: A Demand Perspective. Land. 2022; 11(8):1157. https://doi.org/10.3390/land11081157

Chicago/Turabian StylePeng, Yanling, Yuansheng Jiang, and Yu Hong. 2022. "Heterogeneous Preferences for Selecting Attributes of Farmland Management Right Mortgages in Western China: A Demand Perspective" Land 11, no. 8: 1157. https://doi.org/10.3390/land11081157

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.