Empirical Detection and Quantification of Price Transmission in Endogenously Unstable Markets: The Case of the Global–Domestic Coffee Supply Chain in Papua New Guinea

Abstract

:1. Introduction

1.1. Past Work

1.2. Contribution

2. Materials and Methods

2.1. PNG Coffee Industry and Price Data

2.2. A Framework for Empirically Detecting and Quantifying Price Transmission

2.3. Code Availability

3. Results and Discussion

3.1. Stage 1: Signal Processing

“Throughout the nineteenth century we can trace the history of anarchic cycles of overproduction and underproduction of coffee. Delight in a year when prices have been high is translated into an undue extension of planting, which, four years later, leads to the recurrence of rock-bottom prices. Then there is a panic. In the seventh year, the pendulum swings back once more toward the side of extended planting.”

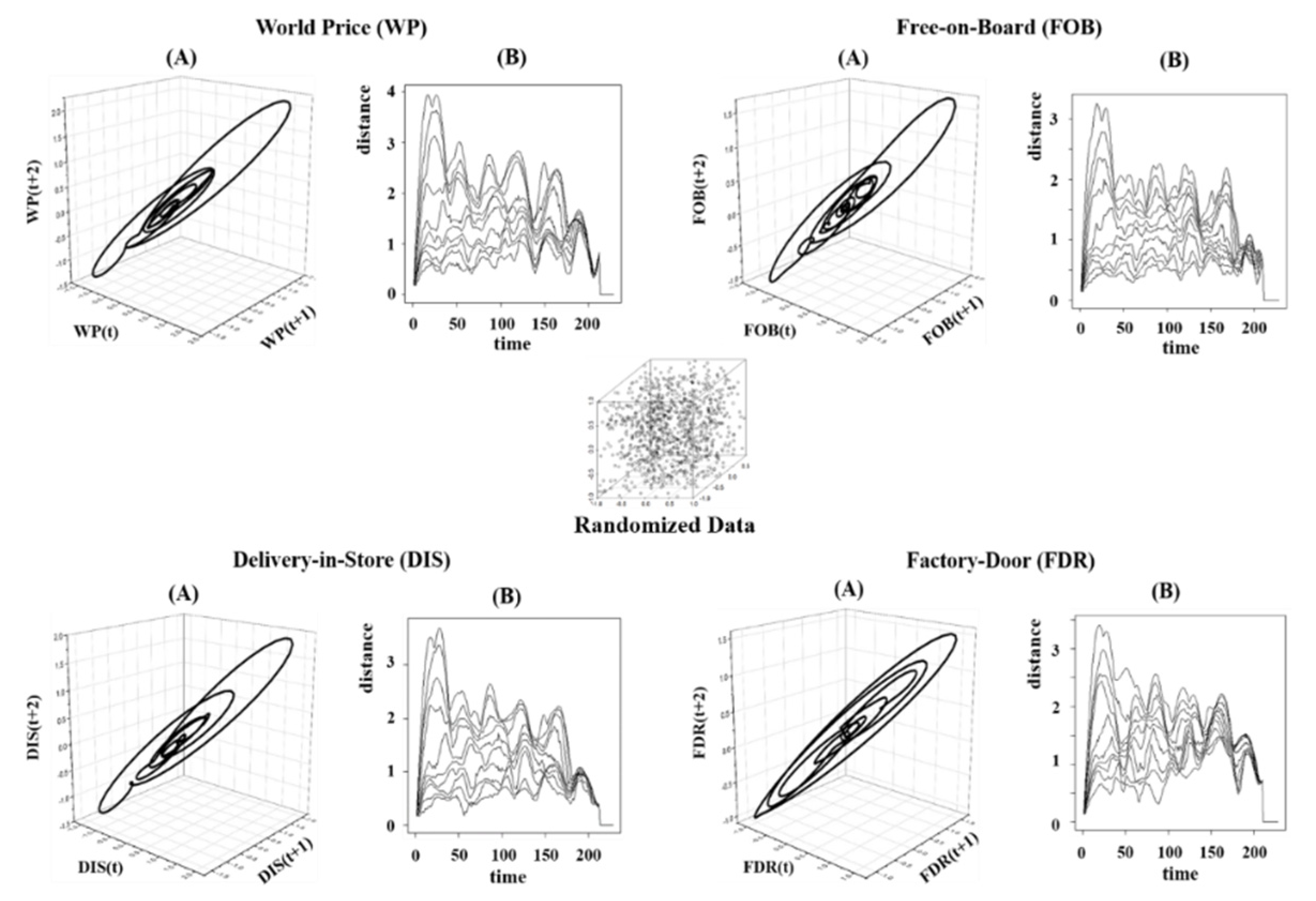

3.2. Stage 2: Reconstruct Market Dynamics from Price Signals

3.3. Stage 3: Test for Market Dynamics with Surrogate Price Data

3.4. Stage 4: Test for Price Transmission

3.5. Quantification of Price Transmission

3.6. Implications for PNG Global–Domestic Supply Chain

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Rapsomanikis, G.; Hallam, D.; Conforti, P. Market Integration and Price Transmission in Selected Food and Cash Crop Markets of Developing Countries: Review and Applications. Available online: www.fao.org/3/YR117E/y5117e06.htm (accessed on 8 December 2020).

- Brundtland Commission. Our Common Future; World Commission on Environment and Development: Oxford, UK, 1987. [Google Scholar]

- Arrow, K.; Dasgupta, P.; Goulder, L.; Daily, G.; Ehrlich, P.; Heal, G.; Levin, S.; Maler, K.; Starrett, D.; Walker, B. Are we consuming too much. J. off Econ. Perspect. 2004, 18, 147–172. [Google Scholar] [CrossRef] [Green Version]

- Fackler, P.; Goodwin, B. Spatial price analysis. In Handbook of Agricultural Economics; Gardner, B., Rausser, G., Eds.; Elsevier Science: Amsterdam, The Netherlands, 2002. [Google Scholar]

- Engle, R.; Granger, C. Cointegration and error correction: Respresentation, estimation and testing. Econometrica 1998, 55, 40–47. [Google Scholar]

- Sexton, R.; Kling, C.; Carman, H. Market integration, efficiency of arbitrage and imperfect competition: Methodology and application to US celery. Amer. J. Agr. Econ. 1991, 73, 568–580. [Google Scholar] [CrossRef] [Green Version]

- Goodwin, B.; Piggot, N. Spatial market integration in the presence of threshold effects. Amer. J. Agr. Econ. 2001, 83, 302–317. [Google Scholar] [CrossRef] [Green Version]

- Balcombe, K.; Rapsomanikis, G. Baysian estimation and selection of nonlinear vector error correction models: The case of the sugar-ethanol-oil nexus in Brazil. Amer. J. Agric. Econ. 2008, 90, 658–668. [Google Scholar] [CrossRef]

- Ghosray, A.; Mohan, S. Coffee price dynamics: An analysis of the retail-international price margin. Eur. Rev. Agric. Econ. 2021, 1–24. [Google Scholar] [CrossRef]

- Glendinning, P. Stability, Instability and Chaos: An Introduction to the Theory of Nonlinear Differential Equations; Cambridge University Press: Cambridge, UK, 1994. [Google Scholar]

- Chavas, J.; Holt, M. On nonlinear dynamics: The case of the pork cycle. Am. J. Agric. Econ. 1991, 73, 819–828. [Google Scholar] [CrossRef]

- Chavas, J.; Holt, M. Market instability and nonlinear dynamics. Am. J. Agric. Econ. 1993, 75, 113–120. [Google Scholar] [CrossRef]

- Jensen, R.; Urban, R. Chaotic price behavior in a non-linear cobweb model. Econ. Lett. 1984, 15, 235–240. [Google Scholar] [CrossRef]

- Berg, E.; Huffaker, R. Economic dynamics of the German hog-price cycle. Int. J. Food Syst. Dyn. 2015, 6, 64–80. [Google Scholar]

- If economists reformed themselves. The Economist, 16 May 2016.

- Kantz, H.; Schreiber, T. Nonlinear Time Series Anaysis; Cambridge University Press: Cambridge, UK, 1997. [Google Scholar]

- Huffaker, R.; Bittelli, M.; Rosa, R. Nonlinear Time Series Analysis with R; Oxford University Press: Oxford, UK, 2017. [Google Scholar]

- Huffaker, R.; Canavari, M.; Munoz-Carpena, R. Distinguishing between endogenous and exogenous price volatility in food security assessment: An empirical nonlinear dynamics approach. Agric. Syst. 2018, 160, 98–109. [Google Scholar] [CrossRef]

- Huffaker, R.; Fearne, A. Reconstructing systematic persistent impacts of promotional marketing with empirical nonlinear dynamics. PLoS ONE 2019, 14, e0221167. [Google Scholar] [CrossRef]

- Huffaker, R.; Hartmann, M. Reconstructing dynamics of foodborne disease outbreaks in the US cattle market from monitoring data. PLoS ONE 2021, 16, e0245867. [Google Scholar] [CrossRef] [PubMed]

- McCullough, M.; Huffaker, R.; Marsh, T. Endogenously determined cycles: Empirical evidence from livestock industries. Nonlinear Dyn. Psychol. Life Sci. 2012, 16, 205–231. [Google Scholar]

- Oreskes, N.; Shrader-Frechette, K.; Belitz, K. Verification, validation, and confirmation of numerical models in the earth sciences. Science 1994, 263, 641–646. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Dambui, C.; Griffith, G.; Mounter, S. Short run coffee processor and expoerter marketing margin behavior in Papua New Guinea. In Proceedings of the International European Forum on System Dynamics and Innovation in Food Networks, Igls, Australia, 15 February 2015. [Google Scholar]

- C.I.C. I.C. Statistical Database; G. CIC Ltd.: Toronto, ON, Canada, 1999–2017. [Google Scholar]

- Papua New Guinea. Available online: https://www.bankpng.gov.pg/historical-exchange-rates/ (accessed on 11 August 2021).

- Golyandina, N.; Nekrutkin, V.; Zhigljavsky, A. Analysis of Time Series Structure; Chapman & Hall/CRC: New York, NY, USA, 2001. [Google Scholar]

- Schreiber, T. Detecting and analyzing nonstationarity in a time series with nonlinear cross predictions. Phys. Rev. Lett. 1997, 78, 843–846. [Google Scholar] [CrossRef] [Green Version]

- Sprott, J. Chaos and Time Series Analysis; Oxford University Press: Oxford, UK, 2003. [Google Scholar]

- Takens, F. Detecting strange attractors in turbulence. In Dynamical Systems and Turbulence; Rand, D., Young, L., Eds.; Springer: New York, NY, USA, 1980; pp. 366–381. [Google Scholar]

- Deyle, E.; Sugihara, G. Generalized theorems for nonlinear state space reconstruction. PLoS ONE 2011, 6, 1–8. [Google Scholar] [CrossRef]

- Provenzale, A.; Smith, L.; Vio, R.; Murante, G. Distinguishing between low-dimensional dynamics and randomness in measured time series. Phys. D 1992, 58, 31. [Google Scholar] [CrossRef]

- Theiler, J.; Eubank, S.; Longtin, A.; Galdrikian, B.; Farmer, J. Testing for nonlinearity in time series: The method of surrogate data. Phys. D 1992, 58, 77–94. [Google Scholar] [CrossRef] [Green Version]

- Small, M.; Tse, C. Applying the method of surrogate data to cyclic time series. Phys. D 2002, 164, 187–201. [Google Scholar] [CrossRef]

- Brandt, C.; Pompe, B. Permutation entropy: A natural complexity measure for time series. Phys. Rev. Lett. 2012, 88, 174102. [Google Scholar] [CrossRef]

- Schreiber, T.; Schmitz, A. Surrogate time series. Phys. D 2000, 142, 346–382. [Google Scholar] [CrossRef] [Green Version]

- Sugihara, G.; May, R.; Hao, Y.; Chih-hao, H.; Deyle, E.; Fogarty, M.; Munch, S. Detecting causality in complex ecosystems. Science 2012, 338, 496–500. [Google Scholar] [CrossRef]

- Muir, J. My First Summer in the Sierra; Houghton Mifflin: Boston, MA, USA, 1911. [Google Scholar]

- Deyle, E.; May, R.; Munch, S.; Sugihara, G. Tracking and forecasting ecosystem interactions in real time. Proc. R. Soc. B 2018, 283, 201522358. [Google Scholar] [CrossRef]

- Version, Origin. Version 2019. Available online: https://www.originlab.com/ (accessed on 10 August 2021).

- Gelb, A. A spectral analysis of coffee market oscillations. Int. Econ. Rev. 1979, 20, 495–514. [Google Scholar] [CrossRef]

- Jacob, H. The Saga of Coffee: The Biography of an Economic Product; Allen and Unwin: London, UK, 1935. [Google Scholar]

- Terazono, E. Brazilians smooth out arabica output cycle. Financial Times, 30 January 2013. [Google Scholar]

- Delfim-Netto, A.; Pinto, C. Brazilian coffee: 20 years of substitution in the international market. ANPES Study 1965, 3. [Google Scholar]

- Geer, T. An Oligopoly: The World Coffee Economy and Stabililization Schemes; Dunellen: New York, NY, USA, 1974. [Google Scholar]

- Vavra, P.; Goodwin, B. Analysis of price transmission along the food chain. In OECD Food, Agriculrual and Fisheries Working Papers; OECD Publishing: Paris, France, 2005. [Google Scholar]

- Bettendorf, L.; Verboven, F. Incomplete transmission of cofee bean prices in the Netherlands. Eur. Rev. Agric. Econ. 2000, 27, 1–16. [Google Scholar] [CrossRef]

- OECD Competition Committee. Competition Issues in the Food Chain Industry; Competition Law & Policy OECD: Paris, France, 2013. [Google Scholar]

- Kim, H.; Ward, R. Price transmission across the U.S. food distribution system. Food Policy 2013, 41, 226–236. [Google Scholar] [CrossRef]

- Ghil, M.; Allen, M.; Dettinger, M.; Ide, K.; Kondrashov, D.; Mann, M.; Robertson, A.; Saunders, A.; Tian, Y.; Varadi, F.; et al. Advanced spectral methods for climatic time series. Rev. Geophys. 2002, 40, 1–41. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| SSA-1 b | SSA-2 d Cycle Length (Months) Signal Strength e | Noise Strength f | ||||||

|---|---|---|---|---|---|---|---|---|

| Trend | 19 | 23 | 28 | 38 | 57 | |||

| WP a | 53% c | 2% | 3% | 37% | 42% | 5% | ||

| FOB | 74% | 1% | 3% | 7% | 10% | 21% | 5% | |

| DIS | 62% | 2% | 7% | 11% | 13% | 33% | 5% | |

| FDR | 55% | 4% | 11% | 20% | 35% | 10% | ||

| World Price | Signal b | Surrogate (low) c | H0 d |

|---|---|---|---|

| Permutation entropy | 0.523 | 0.956 | Reject |

| Free-on-Board | |||

| Permutation entropy | 0.631 | 0.957 | Reject |

| Delivery-in-Store | |||

| Permutation entropy | 0.578 | 0.957 | Reject |

| Factory Door | |||

| Permutation entropy | 0.518 | 0.957 | Reject |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Huffaker, R.; Griffith, G.; Dambui, C.; Canavari, M. Empirical Detection and Quantification of Price Transmission in Endogenously Unstable Markets: The Case of the Global–Domestic Coffee Supply Chain in Papua New Guinea. Sustainability 2021, 13, 9172. https://doi.org/10.3390/su13169172

Huffaker R, Griffith G, Dambui C, Canavari M. Empirical Detection and Quantification of Price Transmission in Endogenously Unstable Markets: The Case of the Global–Domestic Coffee Supply Chain in Papua New Guinea. Sustainability. 2021; 13(16):9172. https://doi.org/10.3390/su13169172

Chicago/Turabian StyleHuffaker, Ray, Garry Griffith, Charles Dambui, and Maurizio Canavari. 2021. "Empirical Detection and Quantification of Price Transmission in Endogenously Unstable Markets: The Case of the Global–Domestic Coffee Supply Chain in Papua New Guinea" Sustainability 13, no. 16: 9172. https://doi.org/10.3390/su13169172