1. Introduction

Historically, Pakistan’s financial sector has undergone significant changes, from nationalization in the 1970s to liberalization in the 1990s and globalization in the 21st century. These changes have increased competition and pressured financial institutions to improve their efficiency and performance. Research suggests that CEO turnover, R&D investments, and pay-performance sensitivities can significantly impact organizational efficiency. For instance, studies have found that CEO turnover can lead to organizational strategy and culture changes, which may positively or negatively impact firm performance [

1,

2]. Similarly, R&D investments have been linked to increased innovation, which can lead to competitive advantages for firms [

3,

4]. Finally, pay-performance sensitivities have been found to impact employee motivation, affecting productivity and performance [

5,

6]. In Pakistan, the government has undertaken several programs to boost R&D, including the Pakistan Council of Science and Technology (PCST) [

7,

8]. Pay-performance sensitivities also play a significant role in the effectiveness of a business. According to research, connecting CEO compensation with performance may increase financial success and organizational efficacy. However, high CEO compensation may negatively impact organizational effectiveness. The Securities and Exchange Commission of Pakistan (SECP) has introduced many policies to encourage openness and accountability concerning pay-performance sensitivity [

9,

10].

The banking sector plays a crucial role in the economy of Pakistan, serving as the backbone of the financial system. The sector comprises a range of financial institutions, including commercial banks, Islamic banks, microfinance banks, and development finance institutions. It contributes significantly to the country’s economic growth by facilitating financial intermediation, mobilizing savings, and providing credit to individuals and businesses [

11,

12,

13]. As of 2021, the banking sector in Pakistan consists of 43 commercial banks, 6 Islamic banks, and 16 microfinance banks, with 17,954 branches across the country [

14]. According to the State Bank of Pakistan, the banking sector’s total assets amounted to PKR 22.8 trillion (

$143 billion) as of June 2021. The importance of the banking sector in Pakistan can be gauged from the fact that it accounts for approximately 70% of the country’s total financial sector assets and employs over 100,000 people [

14]. The sector has played a critical role in the country’s economic development, contributing to the growth of agriculture, manufacturing, and services [

15]. The banking sector has also played a crucial role in financial inclusion by expanding access to financial services and ensuring sustainability in different sectors [

16,

17,

18,

19]. In conclusion, the banking sector is of the utmost importance to Pakistan’s economy, contributing significantly to its growth and development. With continued efforts to expand access to financial services and promote financial inclusion, the banking sector is poised to play an even more critical role in the country’s economic development in the coming years.

Pakistan’s financial industry has witnessed considerable changes and growth throughout the years. In recent years, this industry has placed a greater emphasis on enhancing organizational efficiency. Organizational efficiency refers to the ability of an organization to utilize its resources effectively and efficiently to achieve its goals and objectives. It is a measure of how well an organization optimizes its processes, resources, and capabilities to produce desired outcomes with minimal waste or inefficiencies. Efficiency in an organizational context involves maximizing output or results while minimizing the inputs or resources required. This includes factors such as time, money, materials, energy, and human effort. Organizational efficiency entails utilizing these resources in a way that maximizes productivity, minimizes costs, reduces errors, and improves overall sustainable performance [

20,

21]. One element of this phenomenon is the association between CEO turnover, R&D, and pay-performance sensitivity.

Moreover, research demonstrates that investment in R&D may result in greater organizational efficiency and financial success. According to a study, worldwide investment in research and development has increased to make the world more sustainable [

22]. Given the importance of these factors in determining organizational efficiency, understanding their relationships and how they can be leveraged to improve performance is crucial for financial institutions in Pakistan.

This research significantly contributes to the understanding of organizational efficiency within the financial sector of Pakistan, particularly in the context of CEO turnover, pay-performance sensitivities, and R&D investment. It delivers empirical evidence that underscores the correlation between pay-performance sensitivity, firm age, R&D investment, and organizational efficiency, while identifying areas like high expense ratios that are negatively associated with efficiency. The relatively lesser impact of CEO turnover, duality, and board size on efficiency presented in this study also brings new perspectives to the table. Through the lens of the banking industry in Pakistan, this study enriches the existing literature on corporate governance and organizational efficiency. It equips managers and policymakers in the banking sector with valuable insights that enable them to prioritize their efforts to enhance efficiency, cut down costs, and augment financial performance. This study thus serves as a strategic roadmap for banking leaders, facilitating data-driven decision-making and strategy development. Additionally, this research transcends its geographic focus, having broader implications for global banking and financial organizations grappling with similar challenges pertaining to senior management turnover, wage structures, and efficiency optimization. By proposing a comprehensive framework that can be adapted to various contexts, this study paves the way for improvements not only in Pakistan’s banking industry but also for financial institutions worldwide. Overall, this study represents a significant stride in the exploration of organizational efficiency, CEO turnover, R&D, and pay-performance sensitivities within the banking industry. It offers a robust framework to guide strategic decisions, thereby assisting organizations in their pursuit of heightened operational efficiency and financial success. This study aims to achieve the following objectives:

To investigate the relationship between CEO turnover and organizational efficiency in the financial sector of Pakistan.

To examine the impact of R&D investment on the relationship between CEO turnover and organizational efficiency in the financial sector of Pakistan.

To assess the effect of pay-performance sensitivities on the relationship between CEO turnover and organizational efficiency in the financial sector of Pakistan.

To identify the implications of the findings for policymakers, practitioners, and researchers interested in enhancing Pakistan’s financial sector’s efficiency and competitiveness.

To contribute to the literature on corporate governance, CEO turnover, R&D investment, pay-performance sensitivities, and organizational efficiency in emerging markets, particularly in the financial sector of Pakistan.

The following research questions are formulated:

What is the relationship between CEO turnover and organizational efficiency in the financial sector of Pakistan?

How does R&D investment impact the relationship between CEO turnover and organizational efficiency in the financial sector of Pakistan?

How do pay-performance sensitivities affect the relationship between CEO turnover and organizational efficiency in the financial sector of Pakistan?

What implications do the findings of this study have for policymakers, practitioners, and researchers who aim to enhance the efficiency and competitiveness of Pakistan’s financial sector?

How does this study contribute to the existing literature on corporate governance, CEO turnover, R&D investment, pay-performance sensitivities, and organizational efficiency in emerging markets, specifically in the financial sector of Pakistan?

The present article unfolds through a sequential structure. It begins with a comprehensive review of the existing literature on the topic, offering insights into the historical and current perspectives that frame the context of this study. This overview of prior research sets the stage for the study’s primary focus and emphasizes the significance of the investigation at hand. Following the literature review, the methodology is clearly outlined. This study employs time-series data-based methods, a choice influenced by their suitability for the research questions at hand. The adopted methodological approach is meticulously detailed, offering readers a transparent view of the research process and reinforcing the credibility and reliability of the findings. Subsequently, the results and discussion sections are presented. These crucial segments illuminate the outcomes of the investigation and explore their implications in depth. Every finding is thoroughly examined and contextualized within the broader literature and theoretical framework, fostering a robust understanding of the study’s contributions. Finally, the article concludes with a succinct and thoughtful summary of the research. This final section synthesizes the findings, discusses their implications, and points out potential directions for future research. In doing so, it provides readers with a holistic view of the study, its significance, and its potential influence on the field.

2. Literature Review

The literature on the impact of CEO turnover on organizational performance has proliferated in recent years, and yet, the precise nature of these relationships remains inconclusive and vastly generalized. Studies often group results by the positive and negative effects of CEO turnover without accounting for the specific characteristics and nuances of different types of companies and the countries in which they operate. CEO turnover could have varying impacts on organizational performance, depending on the circumstances of the transition [

23,

24]. Similarly, another study highlighted the potential substantial influence of CEO turnover on a company’s value and profitability [

25]. Parallel research threads have explored the role of R&D investment and pay-performance sensitivities as critical drivers of organizational efficiency. R&D investment could enhance financial institutions’ performance through innovation and the introduction of new products and services [

26,

27]. Meanwhile, pay-performance sensitivity could shape top management behavior, particularly that of the CEO, thereby significantly influencing organizational sustainable performance [

28,

29]. Despite these studies, the literature review reveals a gap. There is a noticeable lack of empirical evidence investigating the relationships between CEO turnover, R&D, and pay-performance sensitivities, specifically in the context of emerging economies like Pakistan. The dynamics of the banking sector, with its inherent characteristics and specificities, necessitate a focused investigation. The aim of this literature review is not merely to summarize existing findings but to critically examine them considering the unique context of Pakistan’s financial sector. By doing so, it hopes to contribute to a richer, more nuanced understanding of the interplay between CEO turnover, R&D, and pay-performance sensitivities, and their collective impact on organizational efficiency in the financial sector of emerging markets like Pakistan.

2.1. CEO Turnover and Organizational Efficiency

CEO turnover and its effects on organizational efficiency is a commonly discussed topic in management research. Previous studies exploring this relationship have yielded mixed results. In this literature review, we aim to consolidate the research surrounding CEO turnover and organizational efficiency to gain a more nuanced understanding of their interplay. Notably, the available literature demonstrates differing outcomes based on various factors. Certain studies posit that CEO turnover negatively influences organizational efficiency due to associated uncertainty and disruption leading to the loss of institutional knowledge and deterioration in decision-making quality [

23,

30,

31]. Conversely, other research advocates that CEO turnover can facilitate organizational change and boost efficiency, given that new CEOs often bring innovative perspectives and strategies [

24,

32,

33]. Further complexities arise when considering the nature and context of the turnover. Planned turnovers, such as retirements, typically have a lesser negative impact on efficiency compared to sudden, unplanned turnovers [

34]. Similarly, CEO-specific factors can significantly influence the impact [

35]. These studies discovered that efficiency impacts were more substantial in cases where the outgoing CEO had a high compensation package, potentially due to greater conflicts during the transition.

However, the reviewed literature largely fails to account for company-specific and country-specific influences, presenting a generalized overview of results without a deeper understanding of the intricacies of specific sectors or emerging markets. It is necessary to understand the hypothesized relationships described below in the theoretical framework in context of the banking sector of emerging countries like Pakistan, given their unique characteristics and specificities. For instance, the dynamics of CEO turnover and its impact on organizational efficiency could be vastly different in this context due to the nature of the banking sector, different corporate governance norms, cultural factors, and the regulatory environment. The literature also showcases geographic diversity in its studies, with ample research conducted in Asian countries. Studies in countries such as Malaysia, France, and China reveal varying impacts of CEO turnover on organizational efficiency [

36,

37,

38]. These results again highlight the need for a more contextual analysis of the phenomenon.

In conclusion, while the literature offers significant insight into the relationship between CEO turnover and organizational efficiency, there is still a need for additional research, particularly within the banking sector of Pakistan. This present study aims to address this gap, by investigating the influence of CEO turnover on performance metrics like return on assets, equity, and net income, and the correlation between CEO tenure and organizational efficiency. These findings can inform strategies to improve efficiency in the banking sector, benefiting scholars, managers, and policymakers. It also contributes to the literature on corporate governance, CEO turnover, R&D investment, pay-performance sensitivities, and organizational efficiency in emerging markets, specifically Pakistan’s financial sector.

2.2. R&D Investments and Organizational Efficiency

Research and development (R&D) investments are essential for businesses seeking to preserve and enhance their competitive edge in today’s quickly evolving business climate. This literature study investigates the connection between R&D expenditures and organizational effectiveness. Research has shown that R&D expenditures enhance company effectiveness. For instance, R&D expenditures have a beneficial effect on productivity and revenue growth in the technology sector [

39]. Similarly, a study showed that pharmaceutical companies’ R&D spending led to higher efficiency and profitability [

40]. In addition, it has been shown that R&D expenditures favor innovation [

41,

42,

43], which may increase organizational efficiency. Another study discovered that R&D spending substantially impacted the innovation performance of Chinese high-tech enterprises [

44].

Furthermore, research has demonstrated that R&D spending benefits the innovation capabilities of developing market enterprises [

45,

46]. However, the link between R&D expenditures and organizational effectiveness is complex. Many studies have demonstrated that business size, industry type, and technological complexity influence the association between R&D spending and organizational efficiency. For instance, R&D spending on organizational efficiency is more significant in more prominent organizations than in smaller ones [

47,

48]. Ineffective management of R&D expenditures may also have a detrimental influence on organizational effectiveness.

In conclusion, R&D expenditures have a favorable impact on organizational efficiency and innovation, although several variables mitigate their connection. Companies should manage their R&D investments carefully to ensure they are aligned with their strategic goals and objectives to optimize their beneficial influence on organizational efficiency. Considering the importance of the financial industry in Pakistan’s economy, it is crucial to explore the correlation between R&D spending and organizational effectiveness in this sector. However, more studies on this issue must be conducted, particularly in Pakistan. Thus, it is necessary to perform research investigating the link between R&D spending and organizational effectiveness in Pakistan’s banking industry. This research will shed light on the difficulties and potential of R&D investments in Pakistan’s financial industry and assist in identifying the best practices that may improve the sector’s efficiency and competitiveness. In addition, this research will contribute to the literature on corporate governance, CEO turnover, pay-performance sensitivity, and organizational efficiency in developing economies, specifically Pakistan’s banking industry. Policymakers, practitioners, and scholars interested in boosting the efficiency and competitiveness of Pakistan’s financial system would find these ideas helpful.

2.3. Pay Performance Sensitivity and Organization Efficiency

Payment performance sensitivity is an organization’s capacity to respond promptly and adequately to payment performance changes, which may substantially influence organizational efficiency. A company must effectively manage payment performance to limit the risk of late or missed payments, save on expenditures, and preserve cash flow. This literature study investigates the connection between payment performance sensitivity and organizational efficiency. According to the literature, payment performance sensitivity impacts supply chain performance [

49,

50]. Research has indicated that a greater sensitivity to payment performance results in improved supply chain performance. This is because firms with a high sensitivity to payment performance tend to communicate better with their suppliers, resulting in enhanced confidence and cooperation and higher supply chain performance.

Similarly, study have shown that payment performance sensitivity is positively related to overall company success [

51,

52]. This research indicates that firms with a high sensitivity to payment performance tend to have higher financial performance and a greater likelihood of pleasing customers and suppliers. The authors suggest that this is because such firms can better control risks connected with payment performance, resulting in more trust and confidence in the enterprise. The articles provide valuable insights into the relationship between corporate social responsibility (CSR) and financial performance [

53,

54]. CSR positively affects financial performance, both directly and indirectly by mitigating the impact of financial instability [

54]. Rjiba et al. revealed that CSR helps offset the negative effects of economic policy uncertainty on firm financial performance. Lahouel et al. addressed endogeneity concerns by studying the CSP–CFP relationship and highlighted the importance of considering external factors. These studies contribute to an understanding of the impact of CSR on corporate financial outcomes.

Another study demonstrated that payment performance substantially affects a company’s profitability and liquidity [

55]. In addition, another study evaluated the effect of payment delays on organizational effectiveness and found that payment delays might harm organizational efficiency and impede the expansion of organizations [

56]. A separate study showed that a correlation exists between payment performance sensitivity and supply chain efficiency [

56,

57]. This suggests that companies attentive to payment performance are more likely to have good supply networks. In addition, payment performance positively influences innovation, as organizations with a substantial payment performance culture are more inclined to invest in innovation and new product development [

57,

58]. Payment delays may harm an organization’s efficiency, while a strong payment performance culture can result in improved financial performance, supply chain efficiency, and innovation. However, there are possible downsides to being too sensitive to payment performance, such as increasing transaction costs and diminished supplier allure. Thus, firms must compromise between sensitivity to payment performance and organizational efficiency.

2.4. Theoretical Framework

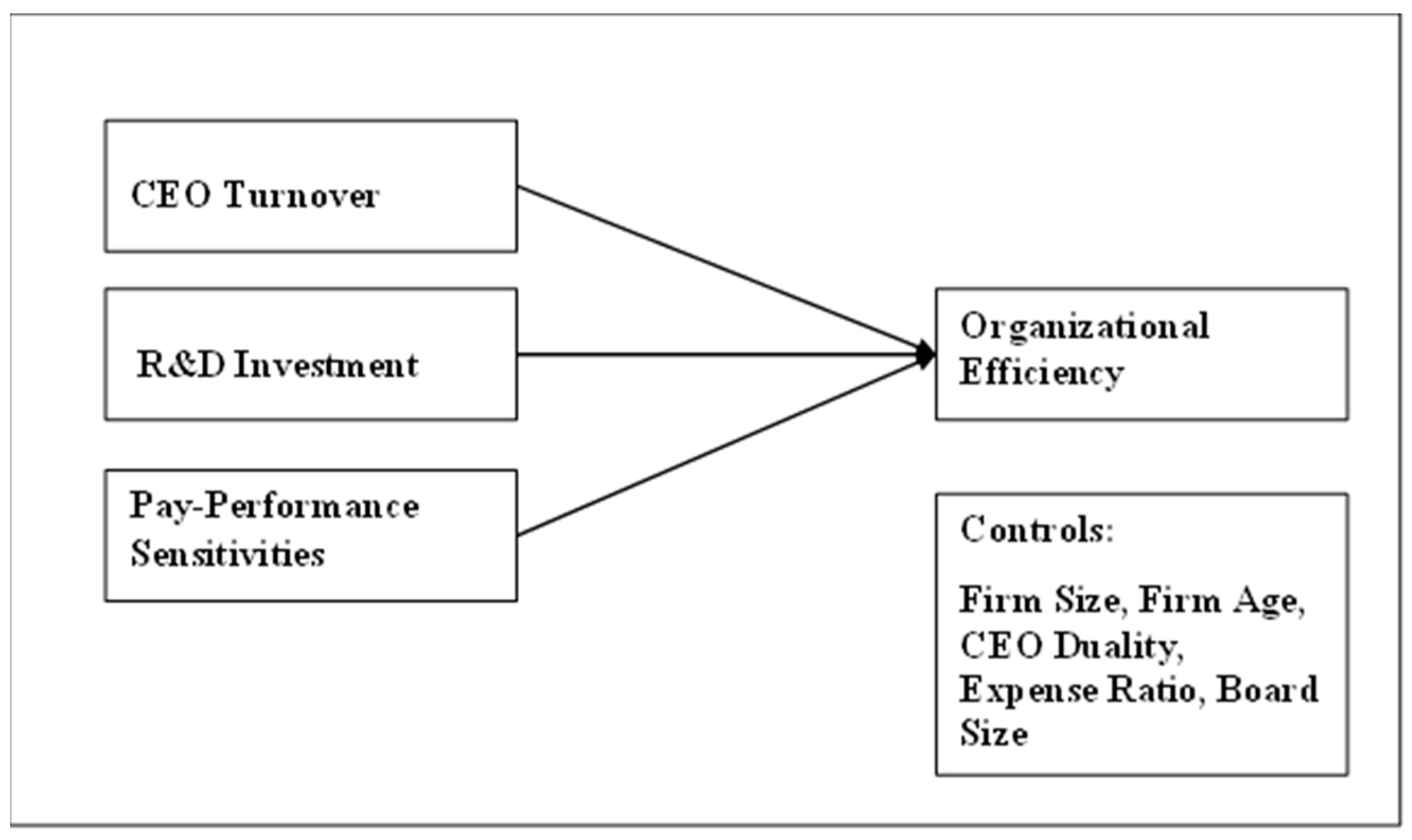

In this section, we establish the theoretical framework shown in

Figure 1 below, aiming to provide an understanding of the conceptual structures that underpin our research. This framework will serve as a roadmap, guiding our investigation and analysis. It is through this lens that we seek to interpret our findings and contribute new insights to existing scholarship.

This study’s theoretical framework on organizational efficiency in the Pakistani banking sector sustainable performance is underpinned by several financial theories. CEO turnover, one of the independent variables, is informed by agency theory, which suggests that CEO turnover may be a way for shareholders to ensure that the CEO acts in their best interest [

59]. R&D investment, another independent variable, is supported by a resource-based view of the firm, which proposes that a firm’s resources and capabilities, such as investments in R&D, can lead to sustainable competitive advantages [

60]. The principal-agent theory informs the pay-performance sensitivities variable, which posits that aligning the interests of managers and shareholders through pay-performance sensitivities can enhance organizational performance [

6]. The dependent variable, organizational efficiency, is informed by efficiency theory, which argues that firms should maximize output given a particular input level [

61]. The control variables, firm size and firm age, are informed by the effects of size and age in finance, which suggest that more extensive and more established firms may have advantages regarding access to resources and reputation [

62,

63]. CEO duality, another control variable, is supported by agency theory, which suggests that separating the roles of CEO and chairman may enhance board independence and lead to better corporate governance [

64]. The expense ratio variable is supported by cost theory, which proposes that higher expenses may reduce a firm’s profitability and efficiency [

65]. Finally, the board size, the last control variable, is informed by agency theory, which suggests that larger boards may provide management with better monitoring and advisory services.

Overall, the study’s theoretical framework draws from various financial theories to comprehensively understand the factors that affect organizational efficiency in the Pakistani banking sector. The following hypotheses were proposed for the study based on the above framework:

H1: CEO turnover harms organizational efficiency in the Pakistani banking sector.

H2: R&D investment has a positive effect on organizational efficiency in the Pakistani banking sector.

H3: Pay-performance sensitivities positively affect organizational efficiency in the Pakistani banking sector.

By considering multiple independent and control variables, this study aims to identify the critical drivers of organizational efficiency and provide insights for policymakers and bank managers to improve performance and competitiveness.

3. Methods

A study of causes in the relationship between CEO turnover sensitivity, compensation performance, and organizational effectiveness from 2005 to 2019 was conducted using the following standard procedures: A proxy for organizational effectiveness were selected as dependent variable—return on assets (ROA) [

66]. Three independent variables were used to determine the impact on organizational effectiveness—CEO turnover, research and development (R&D) expenses, and CEO remuneration. We included leverage, CEO duality, company age, board size, and expense ratio as control factors. CEO turnover was defined as a dummy variable, indicating a value of one if there was a change in the CEO’s identity from year t − 1 to year t, and zero otherwise. R&D expenses were assessed by costs directly associated with the research and development of products or services by companies, and CEO remuneration was measured using the natural logarithm. The sample included 25 banks within the population of the whole banking sector of Pakistan. Regarding the selection process, we utilized a random sampling methodology to ensure the results would not be skewed toward a particular set of banks. This method was chosen to guarantee a fair representation of the banking industry. Regarding the characterization of the banks, due to confidentiality reasons, detailed information about each bank in the sample cannot be provided. Nonetheless, the sample was designed to be diverse, including banks of various sizes, geographical locations, and types (e.g., commercial, investment, etc.), ensuring the findings are representative of the wider banking sector. The published annual reports from 2005 to 2019 of 25 public and private banking institutions were mined for yearly secondary data. The data were collected from the annual reports available on the websites of the relevant banks and the Pakistan stock exchange. The study was conducted in Pakistan.

The data were analyzed using the following econometric model:

where i represents a single bank and t represents the year. Organizational efficiency (ORGEF) of bank i in year t is equal to the constant term (α) plus the coefficient of the sensitivity of salary performance (β_2) multiplied by the natural logarithm of the salary expenses (LNEXC) of bank i in year t, plus the coefficient of the sensitivity of R&D investment (β_3) multiplied by the R&D investment (R&D INV) of bank i in year t, plus the coefficient of the CEO turnover (β_4) multiplied by the CEO turnover (CEOT) of bank i in year t, plus the coefficient of all the control variables (β_5) multiplied by the control variables.

The model also includes a set of control variables (CONTROL) of bank i in year t, as well as the error term (ε_it). The chosen control variables in the model, including CEO turnover, CEO duality, and board size, serve to account for additional factors that could potentially influence organizational efficiency. CEO turnover addresses the impact of leadership changes, CEO duality considers the influence of the combined CEO and chair roles, and board size reflects the composition and coordination dynamics of the board of directors. These control variables are included to ensure that the effects of pay-performance sensitivity, R&D investment, and other independent variables on organizational efficiency are accurately assessed, while accounting for the potential influence of these control factors.

The impact of CEO turnover, R&D expenses, and CEO remuneration on organizational efficiency was determined using multiple regression analysis using STATA 12 software. ROA was chosen for its wide applicability across various industries and the simplicity it brings to performance evaluation. ROA is a measure of how efficiently a company uses its assets to generate profits, providing a valuable perspective on operational efficiency. While this metric may not capture all the nuances of banking activity, it provides a consistent base for comparing performance across different sectors and companies. it allows for a quick and effective comparative analysis, especially for a diversified audience not exclusively acquainted with banking-specific metrics. The study’s results were interpreted by analyzing the coefficients of determination and the significance of the regression model. This study used the statistical approach of multiple regression analysis to examine the connection between a dependent variable and multiple independent factors. Several studies have employed multiple regression analysis to investigate the characteristics of variables and their mutual relationships in panel data [

67,

68,

69]. A multiple regression analysis on the secondary data was performed using STATA software. The findings are presented in the tables below.

4. Results and Discussion

The results and discussion section presents our research findings on the relationship between several variables and their impact on the dependent variable. To examine the validity of our research model, we conducted various statistical tests such as VIF values for multicollinearity, unit root tests, correlation between variables, OLS regression analysis, and robust testing. The OLS regression analysis was then performed to estimate the relationship between the dependent and independent variables. Overall, the results of our analysis provide valuable insights into the relationships between the variables and their impact on the dependent variable. The findings can be generalized to inform decision-making in the banking industry of Pakistan and other developing countries.

The multicollinearity among the variables in the study was assessed using variance inflation factor (VIF) values, as shown in

Table 1. VIF is a statistical measure used to identify the degree of correlation between the predictor variables in a multiple regression analysis [

70]. The VIF values for the variables in the study ranged from 1.04 to 2.18. Generally, a VIF value of 1 indicates no multicollinearity, while values greater than 1 indicate moderate to high multicollinearity. Therefore, based on the results in

Table 1, the multicollinearity among the variables in the study was not a significant concern. It is essential to report the VIF values in a study to provide information about the potential for multicollinearity. Reporting VIF values allows other researchers to assess the reliability and validity of the results and determine if multicollinearity is a potential issue. Using VIF to assess multicollinearity is a well-established statistical practice in regression analysis [

71]. The interpretation of VIF values in multicollinearity is consistent with established reporting standards in statistics and econometrics.

The data in

Table 2 show the results of unit root tests for various variables, including CEO, ROA, LNEXC, R&D INV, CEOT, CEO duality, board size, firm age, and expense ratio. The

p-values for all variables were 0.00, indicating that they were stationary and did not exhibit a trend over time. Stationarity is an important assumption in time series analysis, as it allows for the use of statistical models that rely on constant means and variances. A unit root test is commonly used to determine whether a variable is stationary. It evaluates whether the value has a unit root or a root close to unity in its autoregressive process. In conclusion, the data in

Table 2 provide evidence that the variables analyzed were stationary, which is an important assumption for further analysis and modeling of these variables.

The descriptive statistics in

Table 3 provide an overview of the characteristics of the firms in the dataset. The “CEO Duality” column, a binary variable, reveals that the CEO held a dual role as the chairman in only approximately 1.8% of the observations. This was further underscored by a low standard deviation of 0.132. Regarding “Board Size”, companies on average have approximately nine board members, as reflected in the mean value of 8.557, but with moderate variability, indicated by the standard deviation of 1.598. The “Firm Size” likely measured a company’s total assets or revenues and demonstrated a large mean and a substantial standard deviation, showing that the size of firms in this sample varied widely. The “CEO Turnover” statistics indicated that CEO changes occurred in approximately 17% of the companies, with a standard deviation of 0.375, suggesting that CEO changes are relatively less common. The “Return on Assets (ROA)” metric, indicating a company’s profitability, showed an average return of 0.6% on the assets of the firms in this sample, with a small standard deviation revealing that the profitability of most companies was close to the mean. Lastly, the “Age” column revealed a significant dispersion in the ages of the firms. Despite the average age being approximately 22.5 years, the large standard deviation of 20.283 shows that the sample included a wide age range of companies, from young startups to long-established firms.

Table 4 displays the correlation coefficients between the following variables: ROA, LNEXC, R&D INV, CEOT, CEOD, BS, FIRM AGE, and EXPL. The values in the table represent the strength and direction of the relationship between these variables. The strongest positive correlation was observed between R&D INV and FIRM AGE (r = 0.651,

p < 0.01), followed by the positive correlation between FIRM AGE and LNEXC (r = 0.533,

p < 0.01) and R&D INV and LNEXC (r = 0.881,

p < 0.01). Additionally, there was a positive correlation between BS and R&D INV (r = 0.214,

p < 0.01), BS and ROA (r = 0.197,

p < 0.01) and FIRM AGE and ROA (r = 0.388,

p < 0.01). On the other hand, a negative correlation was observed between EXPL and FIRM AGE (r = −0.204,

p < 0.01), EXPL and BS (r = −0.235,

p < 0.01), and EXPL and ROA (r = −0.386,

p < 0.01). However, there was no significant correlation between ROA and the other variables, except for the weak positive correlation between ROA and BS (r = 0.197,

p < 0.01). Moreover, there was a weak positive correlation between CEOT and LNEXC (r = 0.159,

p < 0.01) and a weak negative correlation between CEOD and BS (r = −0.133,

p < 0.05). The results suggest that R&D investment, board size, firm age, and pay-performance sensitivity are positively associated with firm efficiency and performance. In contrast, CEO turnover, CEO duality, and expense ratio were negatively associated with these variables.

Table 5 presents an OLS regression analysis examining the relationship between several independent variables and the dependent variable, organization efficiency (ROA). The analysis included six independent variables, including LNEXC (pay-performance sensitivity), R&D INV (R&D investment), CEOT (CEO turnover), CEOD (CEO duality), BS (board size), and EXPL (expense ratio), as well as firm age. The results showed that LNEXC, R&D INV, and firm age were all significant predictors of ROA, with coefficients of 0.002, 0.003, and 0.000, respectively, and t-values of 3.28, 4.13, and 4.85, respectively. The negative coefficient for EXPL indicates that higher expense ratios were associated with lower organization efficiency, with a coefficient value of −0.035 and a t-value of −6.98. The other independent variables, including CEOT, CEOD, and BS, did not appear to have a significant relationship with ROA, as their coefficient values were not statistically significant at the 5% level. Overall, the model had an R-square value of 0.415, indicating that the independent variables explained 41.5% of the variance in organizational efficiency. The F-test was also statistically significant for all models, indicating that the overall model fit well.

In conclusion, this analysis provided evidence for the positive impact of pay-performance sensitivity, R&D investment, and firm age on organization efficiency, while higher expense ratios were associated with a lower efficiency. However, CEO turnover, duality, and board size could be much higher on organizational efficiency. The results are consistent with prior research. The agency theory supports the positive relationship between pay-performance sensitivity and firm performance [

6]. At the same time, the positive relationship between R&D investment and firm performance is consistent with prior studies [

39,

42], and the positive relationship between firm age and firm performance is consistent with the resource-based theory [

72].

Table 6 presents the results of robust testing on various variables using the DEER model. The results of both the DEER model and OLS model were similar, proving the robustness of the model. The coefficient values and corresponding Z-values are shown for each variable. LNEXC had a significant positive coefficient value of 0.070 (significant at 1% level), indicating that pay performance sensitivity positively affected firm performance. R&D INV had a significant positive coefficient value of 0.052 (significant at a 5% level), indicating that R&D investment positively affected firm performance. CEOT had a nonsignificant negative coefficient value of −0.044, indicating that CEO turnover did not significantly affect firm performance. CEOD had non-significant coefficient values, indicating that CEO duality did not significantly affect firm performance. BS had non-significant negative coefficient values, indicating that board size did not significantly affect firm performance. Firm Age had a significant positive coefficient value of 0.000 (significant at 1% level), indicating that older firms performed better. EXPL had a significant negative coefficient value of −0.312 (significant at a 5% level), indicating that the expense ratio negatively affected firm performance.

5. Conclusions and Recommendations

The conclusions drawn from this study hold substantial implications for Pakistan’s financial sector. Pay-performance sensitivity, R&D investment, and firm age were discovered to have a notable positive impact on organizational efficiency. This suggests that aligning pay with performance, focusing on research and development, and leveraging experience gained over time can significantly enhance a firm’s operational efficiency. Conversely, this investigation revealed that CEO turnover, CEO duality, and board size do not significantly affect organizational efficiency. This finding suggests that these corporate governance aspects, while crucial, might not directly influence operational efficiency in Pakistan’s financial sector.

The findings of this study align with the literature and offer valuable insights into the factors impacting organizational efficiency. To enhance competitiveness and sustainability, financial institutions should focus on bolstering pay-performance sensitivity, investing more significantly in R&D, and effectively managing expenses. Newly established firms should seek to learn from the experiences of older, more established firms to increase their operational efficiency. In the same vein, the banking sector, particularly in developing nations like Pakistan, could benefit from improved management practices and incentive systems that link pay to performance. Research and development should be prioritized to foster innovation and the development of new products and services, thereby attracting more clients and enhancing profitability.

This study’s findings highlight crucial elements for enhancing organizational efficiency in the banking sector, providing valuable insights that can guide banks in Pakistan and other emerging markets to optimize operations, maximize resources, and increase their global competitiveness. Nevertheless, this study did not account for the impact of the financial crisis of 2008 on these variables, a factor that could potentially influence the conclusions drawn. Future research could explore this aspect to gain a comprehensive understanding of the factors influencing organizational efficiency in the financial sector.

The findings indicate a positive correlation between pay-performance sensitivity and banking R&D expenditure. This not only promotes environmental sustainability by fostering potential innovation in eco-friendly practices, but also contributes to economic sustainability by reducing costs and enhancing financial performance. Enhanced financial inclusion and job security are just two of the social benefits highlighted in this study. In addition to informing governance and policy, the results can assist decision-makers in prioritizing R&D expenditures and compensation plans to optimize productivity. By focusing on these areas, Pakistan’s banking sector can enhance its long-term viability, productivity, and profitability.

These are some prospective areas for future banking industry research based on the results of this analysis. With the rising use of technology in banking, it would be interesting to examine how digitalization affects the efficiency of banking institutions in Pakistan and other emerging nations. This may include online banking, mobile banking, and chatbots powered by artificial intelligence. The relationship between corporate social responsibility (CSR) and organizational effectiveness in the banking industry can also be investigated. This can aid comprehension of how CSR initiatives affect the performance of banks. The current analysis revealed the beneficial effect of pay-performance sensitivity on efficiency, demonstrating that employee engagement may be vital to organizational efficiency. Future research can investigate the connection between employee engagement and organizational effectiveness in the banking sector. Pakistan and other developing nations frequently endure political and economic volatility, which can affect the performance of banks. Future research might investigate how political and economic volatility affects the efficacy of banking institutions and provide mitigation techniques.

{kind=link}